3

More Annotations

6

4

Favourite Annotations

3

4

Text

NEWFOUND RESEARCHABOUT USINVESTPODCASTRESEARCHCONTACT USLIQUIDITY

CASCADES

Newfound Research LLC is a quantitative investment and research firm. The firm was founded in August 2008. We currently serve financial advisors via open-end mutual funds, ETFs, and separately managed accounts through most major model manager platforms / TAMPs. For qualified firms, we offer model delivery and customized mandatesolutions.

RESEARCH LIBRARY

We explore the application of tactical signals to a rolling put strategy, seeking to minimize long-term costs while still providing meaningful protection. Read more. Flirting with Models, Season 3. We've begun releasing episodes of Season 3 of Flirting wiith Models and will continue to release throughout July 2020.LIQUIDITY CASCADES

LIQUIDITY CASCADES. A central property of a complex system is the possible occurrence of coherent large-scale collective behaviors with a very rich structure, resulting from the repeated non-linear interactions among its constituents: the whole turns out to be much more than the sum of its parts. PODCAST | FLIRTING WITH MODELS Flirting with Models is the show that aims to pull back the curtain and meet the investors who research, design, develop, and manage quantitative investment strategies. Join Corey Hoffstein, Chief Investment Officer of Newfound Research, on a journey to explore systematic investment strategies, ranging from value to momentum and merger arbitrage to managed futures. If S4E2 - DARRIN JOHNSON S4E2 – Darrin Johnson. Darrin Johnson is the first independent trader I’ve interviewed for this show and with that distinction he brings an entirely new perspective. After learning about how Darrin began his career as an independent trader, we get into the bulk of the conversation that circles around his process of shorting volatility in UNDERSTANDING DYNAMIC, VOLATILITY- ADJUSTED MOMENTUM UNDERSTANDING THE DYNAMIC WINDOW 5 Price Series Trend Noise = + Consider decomposing a price series into trend and noise: The variable m determines how strongly the price series trends; the variable a determines how volatile the price series is. Momentum systems seek to A SHOCK TO THE COVARIANCE SYSTEM UNDERSTANDING OPTIMIZATION: ERRORS IN OPTIMIZATION Understanding Optimization: Errors in Optimization. By Corey Hoffstein. On January 14, 2013. In the last post of the series, Understanding Optimization: Intuition, we provided an overview of what optimization is and provided an intuition for how it works for non-practitioners. We left off with an image of the Rastriginfunction, a complex

NEWFOUND RESEARCHABOUT USINVESTPODCASTRESEARCHCONTACT USLIQUIDITYCASCADES

Newfound Research LLC is a quantitative investment and research firm. The firm was founded in August 2008. We currently serve financial advisors via open-end mutual funds, ETFs, and separately managed accounts through most major model manager platforms / TAMPs. For qualified firms, we offer model delivery and customized mandatesolutions.

RESEARCH LIBRARY

We explore the application of tactical signals to a rolling put strategy, seeking to minimize long-term costs while still providing meaningful protection. Read more. Flirting with Models, Season 3. We've begun releasing episodes of Season 3 of Flirting wiith Models and will continue to release throughout July 2020.LIQUIDITY CASCADES

LIQUIDITY CASCADES. A central property of a complex system is the possible occurrence of coherent large-scale collective behaviors with a very rich structure, resulting from the repeated non-linear interactions among its constituents: the whole turns out to be much more than the sum of its parts. PODCAST | FLIRTING WITH MODELS Flirting with Models is the show that aims to pull back the curtain and meet the investors who research, design, develop, and manage quantitative investment strategies. Join Corey Hoffstein, Chief Investment Officer of Newfound Research, on a journey to explore systematic investment strategies, ranging from value to momentum and merger arbitrage to managed futures. If S4E2 - DARRIN JOHNSON S4E2 – Darrin Johnson. Darrin Johnson is the first independent trader I’ve interviewed for this show and with that distinction he brings an entirely new perspective. After learning about how Darrin began his career as an independent trader, we get into the bulk of the conversation that circles around his process of shorting volatility in UNDERSTANDING DYNAMIC, VOLATILITY- ADJUSTED MOMENTUM UNDERSTANDING THE DYNAMIC WINDOW 5 Price Series Trend Noise = + Consider decomposing a price series into trend and noise: The variable m determines how strongly the price series trends; the variable a determines how volatile the price series is. Momentum systems seek to OPTION-BASED TREND FOLLOWING The strategy is rebalanced monthly on the options expiration dates. For the option-based trend strategy, on each rebalance date, we will purchase a 1-month call if the trend signal is positive or a put if the trend signal is negative. We will purchase all options at-the-money (ATM) and hold them toTAIL HEDGING

30% OTM Strategy: Buy a 3-month 30% OTM put on February 21 st and sell a 2-month 1.4% ITM put on March 20 th. When bought, the option had an implied volatility of 35.0% and a price of $5.42; when sold it had an implied volatility of 53.8% and a price of $425.85 for a 7757% return.LIQUIDITY CASCADES

LIQUIDITY CASCADES. A central property of a complex system is the possible occurrence of coherent large-scale collective behaviors with a very rich structure, resulting from the repeated non-linear interactions among its constituents: the whole turns out to be much more than the sum of its parts. DIVERSIFICATION WITH PORTABLE BETA Conclusion. In this research note, we explored diversification in a long/flat tactical equity strategy with a portable beta bond overlay. By decomposing the strategy into its passive holdings (50/50 stock/bond portfolio and U.S. Treasury futures) and active long/short overlays (trend equity, bond carry, bond momentum, and bond value), wefound

ENSEMBLES AND REBALANCING While seemingly random, there is nothing particularly magical about these signals. The holding period was selected to align with approximately 1/12 th of the evaluation period, to match the usual 1-year lookback with 1-month holding period.; Dubikovsky, Vladislav and Susinno, Gabriele, Demystifying Rebalancing Premium and Extending Portfolio Theory in the Process (May 20, 2015). PUT-WRITE ETFS AS ALTERNATIVE INCOME OPTIONS Put-Write ETFs. or more appropriately, ETF. Currently, the only ETF available for put-write strategies is the U.S. Equity High Volatility Put Write Index Fund ETF (HVPW). It has $52 million in AUM and an expense ratio of 95 bps. Every two months, it sells 15% OTM cash-secured puts on 20 of the largest stocks with the highest impliedvolatility.

S4E4 - TINA LINDSTROM S4E4 – Tina Lindstrom. Tina Lindstrom is a Partner at First NY, where she manages an oil volatility portfolio. She began her career at Susquehanna and eventually worked her way up to managing both the high cap equity index group and the commodity volatility group. This gives her the unique perspective to be able to compare and contrast how PROTECT & PARTICIPATE: MANAGING DRAWDOWNS WITH TREND Returns are gross of all fees, including management fees, transaction costs, and taxes. A few important takeaways: Trend following is not a risk panacea. Even with trend following applied, drawdowns in excess of 15% occurred in each of these cases. This is the cost of market participation, which will address a bit later. DYNAMIC SPENDING IN RETIREMENT MONTE CARLO Dynamic Spending Rules. If the goal is ultimately not to run out of funds in retirement, the first spending adjustment case can substantially improve those chances (aside from a large negative return in the final periods prior to the last withdrawals). Each month, we will compare the portfolio value to the 90% success value. RISK IGNITION WITH TREND FOLLOWING Consider, for example, the optimal mixture that targets the same risk profile of the 30/70 stock/bond blend. The portfolio holds 9.7% in stocks, 48.4% in bonds and 41.9% in the trend strategy. This means that in years where stocks are exhibiting a positive trend, theportfolio is

NEWFOUND RESEARCHABOUT USINVESTPODCASTRESEARCHCONTACT USLIQUIDITYCASCADES

Newfound Research LLC is a quantitative investment and research firm. The firm was founded in August 2008. We currently serve financial advisors via open-end mutual funds, ETFs, and separately managed accounts through most major model manager platforms / TAMPs. For qualified firms, we offer model delivery and customized mandatesolutions.

RESEARCH LIBRARY

We explore the application of tactical signals to a rolling put strategy, seeking to minimize long-term costs while still providing meaningful protection. Read more. Flirting with Models, Season 3. We've begun releasing episodes of Season 3 of Flirting wiith Models and will continue to release throughout July 2020. PODCAST | NEWFOUND RESEARCH Podcast. Flirting with Models is the show that aims to pull back the curtain and meet the investors who research, design, develop, and manage quantitative investment strategies. Join Corey Hoffstein, Chief Investment Officer of Newfound Research, on a journey to explore systematic investment strategies, ranging from value to momentum andmerger

TREND EQUITY

A Little, But Frequently. Our journal-published research suggests that the simple choice of when a strategy rebalances can have a significant impact on realized strategy results. In an effort to avoid this risk, the Newfound/ReSolve Robust Equity Momentum Index adopts a PODCAST | FLIRTING WITH MODELS Flirting with Models is the show that aims to pull back the curtain and meet the investors who research, design, develop, and manage quantitative investment strategies. Join Corey Hoffstein, Chief Investment Officer of Newfound Research, on a journey to explore systematic investment strategies, ranging from value to momentum and merger arbitrage to managed futures. If S4E2 - DARRIN JOHNSON S4E2 – Darrin Johnson. Darrin Johnson is the first independent trader I’ve interviewed for this show and with that distinction he brings an entirely new perspective. After learning about how Darrin began his career as an independent trader, we get into the bulk of the conversation that circles around his process of shorting volatility in S5E5 - ANGUS CAMERON Angus Cameron is the Founder and CIO of Liminal Capital, a machine-learning focused investment manager. But Angus does not come to markets with a computer science PhD. Rather, his career arc took him through the prop desks and buyside of Asia, trading global fixed income, FX, equity markets, and arbitrage strategies on a discretionary basis. DIVERSIFICATION WITH PORTABLE BETA S4E4 - TINA LINDSTROM S4E4 – Tina Lindstrom. Tina Lindstrom is a Partner at First NY, where she manages an oil volatility portfolio. She began her career at Susquehanna and eventually worked her way up to managing both the high cap equity index group and the commodity volatility group. This gives her the unique perspective to be able to compare and contrast how PUT-WRITE ETFS AS ALTERNATIVE INCOME OPTIONS Put-Write ETFs. or more appropriately, ETF. Currently, the only ETF available for put-write strategies is the U.S. Equity High Volatility Put Write Index Fund ETF (HVPW). It has $52 million in AUM and an expense ratio of 95 bps. Every two months, it sells 15% OTM cash-secured puts on 20 of the largest stocks with the highest impliedvolatility.

NEWFOUND RESEARCHABOUT USINVESTPODCASTRESEARCHCONTACT USLIQUIDITYCASCADES

Newfound Research LLC is a quantitative investment and research firm. The firm was founded in August 2008. We currently serve financial advisors via open-end mutual funds, ETFs, and separately managed accounts through most major model manager platforms / TAMPs. For qualified firms, we offer model delivery and customized mandatesolutions.

RESEARCH LIBRARY

We explore the application of tactical signals to a rolling put strategy, seeking to minimize long-term costs while still providing meaningful protection. Read more. Flirting with Models, Season 3. We've begun releasing episodes of Season 3 of Flirting wiith Models and will continue to release throughout July 2020. PODCAST | NEWFOUND RESEARCH Podcast. Flirting with Models is the show that aims to pull back the curtain and meet the investors who research, design, develop, and manage quantitative investment strategies. Join Corey Hoffstein, Chief Investment Officer of Newfound Research, on a journey to explore systematic investment strategies, ranging from value to momentum andmerger

TREND EQUITY

A Little, But Frequently. Our journal-published research suggests that the simple choice of when a strategy rebalances can have a significant impact on realized strategy results. In an effort to avoid this risk, the Newfound/ReSolve Robust Equity Momentum Index adopts a PODCAST | FLIRTING WITH MODELS Flirting with Models is the show that aims to pull back the curtain and meet the investors who research, design, develop, and manage quantitative investment strategies. Join Corey Hoffstein, Chief Investment Officer of Newfound Research, on a journey to explore systematic investment strategies, ranging from value to momentum and merger arbitrage to managed futures. If S4E2 - DARRIN JOHNSON S4E2 – Darrin Johnson. Darrin Johnson is the first independent trader I’ve interviewed for this show and with that distinction he brings an entirely new perspective. After learning about how Darrin began his career as an independent trader, we get into the bulk of the conversation that circles around his process of shorting volatility in S5E5 - ANGUS CAMERON Angus Cameron is the Founder and CIO of Liminal Capital, a machine-learning focused investment manager. But Angus does not come to markets with a computer science PhD. Rather, his career arc took him through the prop desks and buyside of Asia, trading global fixed income, FX, equity markets, and arbitrage strategies on a discretionary basis. DIVERSIFICATION WITH PORTABLE BETA S4E4 - TINA LINDSTROM S4E4 – Tina Lindstrom. Tina Lindstrom is a Partner at First NY, where she manages an oil volatility portfolio. She began her career at Susquehanna and eventually worked her way up to managing both the high cap equity index group and the commodity volatility group. This gives her the unique perspective to be able to compare and contrast how PUT-WRITE ETFS AS ALTERNATIVE INCOME OPTIONS Put-Write ETFs. or more appropriately, ETF. Currently, the only ETF available for put-write strategies is the U.S. Equity High Volatility Put Write Index Fund ETF (HVPW). It has $52 million in AUM and an expense ratio of 95 bps. Every two months, it sells 15% OTM cash-secured puts on 20 of the largest stocks with the highest impliedvolatility.

PODCAST | NEWFOUND RESEARCH Podcast. Flirting with Models is the show that aims to pull back the curtain and meet the investors who research, design, develop, and manage quantitative investment strategies. Join Corey Hoffstein, Chief Investment Officer of Newfound Research, on a journey to explore systematic investment strategies, ranging from value to momentum andmerger

DIVERSIFICATION WITH PORTABLE BETA Conclusion. In this research note, we explored diversification in a long/flat tactical equity strategy with a portable beta bond overlay. By decomposing the strategy into its passive holdings (50/50 stock/bond portfolio and U.S. Treasury futures) and active long/short overlays (trend equity, bond carry, bond momentum, and bond value), wefound

LIQUIDITY CASCADES

LIQUIDITY CASCADES. A central property of a complex system is the possible occurrence of coherent large-scale collective behaviors with a very rich structure, resulting from the repeated non-linear interactions among its constituents: the whole turns out to be much more than the sum of its parts.TAIL HEDGING

30% OTM Strategy: Buy a 3-month 30% OTM put on February 21 st and sell a 2-month 1.4% ITM put on March 20 th. When bought, the option had an implied volatility of 35.0% and a price of $5.42; when sold it had an implied volatility of 53.8% and a price of $425.85 for a 7757% return. ENSEMBLES AND REBALANCING While seemingly random, there is nothing particularly magical about these signals. The holding period was selected to align with approximately 1/12 th of the evaluation period, to match the usual 1-year lookback with 1-month holding period.; Dubikovsky, Vladislav and Susinno, Gabriele, Demystifying Rebalancing Premium and Extending Portfolio Theory in the Process (May 20, 2015). UNDERSTANDING DYNAMIC, VOLATILITY- ADJUSTED MOMENTUM UNDERSTANDING THE DYNAMIC WINDOW 5 Price Series Trend Noise = + Consider decomposing a price series into trend and noise: The variable m determines how strongly the price series trends; the variable a determines how volatile the price series is. Momentum systems seek to THINKING IN LONG/SHORT PORTFOLIOS Portfolio = Benchmark + b x Long/Short. Here, the legs of the Long/Short portfolio are assumed to have 100% notional exposure. Using the example above, this would mean that the long/short is 100% long Stock B, 100% short Stock A, and b is equal to 25%. This step is important because it allows us to disentangle quantity from quality. UNDERSTANDING OPTIMIZATION: ERRORS IN OPTIMIZATION Understanding Optimization: Errors in Optimization. By Corey Hoffstein. On January 14, 2013. In the last post of the series, Understanding Optimization: Intuition, we provided an overview of what optimization is and provided an intuition for how it works for non-practitioners. We left off with an image of the Rastriginfunction, a complex

RISK BUDGETING (WITH SPREADSHEET) The asset weights that achieved a specified risk profile can be calculated using Solver, which is preset and accessed by clicking on the “Solve” button. The sheet is preloaded with data from SPY, TLT and EEM and a risk profile of 30%, 40% and 30%, respectively. Solving this yields allocations of 37% SPY, 44.6% TLT and 18.4% EEM. RISK ATTRIBUTION IN A PORTFOLIO Risk Attribution in a Portfolio. Diversification is touted as the only free lunch (see our old post Is Diversification Really a Free Lunch) in investing and is a primary way to reduce portfolio volatility without sacrificing a proportional amount of return. Return characteristics aside, a well-diversified portfolio can be less riskythan any of

NEWFOUND RESEARCHABOUT USINVESTPODCASTRESEARCHCONTACT USLIQUIDITYCASCADES

Newfound Research LLC is a quantitative investment and research firm. The firm was founded in August 2008. We currently serve financial advisors via open-end mutual funds, ETFs, and separately managed accounts through most major model manager platforms / TAMPs. For qualified firms, we offer model delivery and customized mandatesolutions.

RESEARCH LIBRARY

We explore the application of tactical signals to a rolling put strategy, seeking to minimize long-term costs while still providing meaningful protection. Read more. Flirting with Models, Season 3. We've begun releasing episodes of Season 3 of Flirting wiith Models and will continue to release throughout July 2020.LIQUIDITY CASCADES

LIQUIDITY CASCADES. A central property of a complex system is the possible occurrence of coherent large-scale collective behaviors with a very rich structure, resulting from the repeated non-linear interactions among its constituents: the whole turns out to be much more than the sum of its parts. S4E2 - DARRIN JOHNSON S4E2 – Darrin Johnson. Darrin Johnson is the first independent trader I’ve interviewed for this show and with that distinction he brings an entirely new perspective. After learning about how Darrin began his career as an independent trader, we get into the bulk of the conversation that circles around his process of shorting volatility in PODCAST | FLIRTING WITH MODELS Flirting with Models is the show that aims to pull back the curtain and meet the investors who research, design, develop, and manage quantitative investment strategies. Join Corey Hoffstein, Chief Investment Officer of Newfound Research, on a journey to explore systematic investment strategies, ranging from value to momentum and merger arbitrage to managed futures. If DIVERSIFICATION WITH PORTABLE BETA UNDERSTANDING DYNAMIC, VOLATILITY- ADJUSTED MOMENTUM UNDERSTANDING THE DYNAMIC WINDOW 5 Price Series Trend Noise = + Consider decomposing a price series into trend and noise: The variable m determines how strongly the price series trends; the variable a determines how volatile the price series is. Momentum systems seek to UNDERSTANDING OPTIMIZATION: ERRORS IN OPTIMIZATION Understanding Optimization: Errors in Optimization. By Corey Hoffstein. On January 14, 2013. In the last post of the series, Understanding Optimization: Intuition, we provided an overview of what optimization is and provided an intuition for how it works for non-practitioners. We left off with an image of the Rastriginfunction, a complex

2 WAYS TO LOWER PORTFOLIO DRAWDOWN As a simple example, say that an equity portfolio is 100% allocated to the S&P 500 ETF SPY. Over the last ten years, SPY has returned 7.7% with volatility of 21.0%*. The largest peak to trough loss – otherwise known as the max drawdown – over the period was 55.2%. Now consider a made-up tactical strategy: the Benjamin Button Strategy PUT-WRITE ETFS AS ALTERNATIVE INCOME OPTIONS Put-Write ETFs. or more appropriately, ETF. Currently, the only ETF available for put-write strategies is the U.S. Equity High Volatility Put Write Index Fund ETF (HVPW). It has $52 million in AUM and an expense ratio of 95 bps. Every two months, it sells 15% OTM cash-secured puts on 20 of the largest stocks with the highest impliedvolatility.

NEWFOUND RESEARCHABOUT USINVESTPODCASTRESEARCHCONTACT USLIQUIDITYCASCADES

Newfound Research LLC is a quantitative investment and research firm. The firm was founded in August 2008. We currently serve financial advisors via open-end mutual funds, ETFs, and separately managed accounts through most major model manager platforms / TAMPs. For qualified firms, we offer model delivery and customized mandatesolutions.

RESEARCH LIBRARY

We explore the application of tactical signals to a rolling put strategy, seeking to minimize long-term costs while still providing meaningful protection. Read more. Flirting with Models, Season 3. We've begun releasing episodes of Season 3 of Flirting wiith Models and will continue to release throughout July 2020.LIQUIDITY CASCADES

LIQUIDITY CASCADES. A central property of a complex system is the possible occurrence of coherent large-scale collective behaviors with a very rich structure, resulting from the repeated non-linear interactions among its constituents: the whole turns out to be much more than the sum of its parts. S4E2 - DARRIN JOHNSON S4E2 – Darrin Johnson. Darrin Johnson is the first independent trader I’ve interviewed for this show and with that distinction he brings an entirely new perspective. After learning about how Darrin began his career as an independent trader, we get into the bulk of the conversation that circles around his process of shorting volatility in PODCAST | FLIRTING WITH MODELS Flirting with Models is the show that aims to pull back the curtain and meet the investors who research, design, develop, and manage quantitative investment strategies. Join Corey Hoffstein, Chief Investment Officer of Newfound Research, on a journey to explore systematic investment strategies, ranging from value to momentum and merger arbitrage to managed futures. If DIVERSIFICATION WITH PORTABLE BETA UNDERSTANDING DYNAMIC, VOLATILITY- ADJUSTED MOMENTUM UNDERSTANDING THE DYNAMIC WINDOW 5 Price Series Trend Noise = + Consider decomposing a price series into trend and noise: The variable m determines how strongly the price series trends; the variable a determines how volatile the price series is. Momentum systems seek to UNDERSTANDING OPTIMIZATION: ERRORS IN OPTIMIZATION Understanding Optimization: Errors in Optimization. By Corey Hoffstein. On January 14, 2013. In the last post of the series, Understanding Optimization: Intuition, we provided an overview of what optimization is and provided an intuition for how it works for non-practitioners. We left off with an image of the Rastriginfunction, a complex

TREND EQUITY

A Little, But Frequently. Our journal-published research suggests that the simple choice of when a strategy rebalances can have a significant impact on realized strategy results. In an effort to avoid this risk, the Newfound/ReSolve Robust Equity Momentum IndexTAIL HEDGING

30% OTM Strategy: Buy a 3-month 30% OTM put on February 21 st and sell a 2-month 1.4% ITM put on March 20 th. When bought, the option had an implied volatility of 35.0% and a price of $5.42; when sold it had an implied volatility of 53.8% and a price of $425.85 for a 7757% return. OPTION-BASED TREND FOLLOWING The strategy is rebalanced monthly on the options expiration dates. For the option-based trend strategy, on each rebalance date, we will purchase a 1-month call if the trend signal is positive or a put if the trend signal is negative. We will purchase all options at-the-money (ATM) and hold them to S4E5 - GUILLERMO RODITI DOMINGUEZ In this episode I speak with Guillermo Roditi Dominguez, managing director at New River Investments. This was one of the more unique and wide-ranging conversations I have had on the podcast to date. We begin by discussing Guillermo’s approach to portfolio construction, which is heavily focused on the idea of under-writing risk. How he goes TIMING TREND MODEL SPECIFICATION WITH MOMENTUM After constructing the 1023 different strategies, we will then apply a momentum model that ranks the models based upon prior returns and equally-weights our portfolio across the top 10%. These choices are made daily and implemented with 21 overlapping portfolios to reduce the impact of rebalance timing luck. UNDERSTANDING OPTIMIZATION: ERRORS IN OPTIMIZATION Understanding Optimization: Errors in Optimization. By Corey Hoffstein. On January 14, 2013. In the last post of the series, Understanding Optimization: Intuition, we provided an overview of what optimization is and provided an intuition for how it works for non-practitioners. We left off with an image of the Rastriginfunction, a complex

PUT-WRITE ETFS AS ALTERNATIVE INCOME OPTIONS Put-Write ETFs. or more appropriately, ETF. Currently, the only ETF available for put-write strategies is the U.S. Equity High Volatility Put Write Index Fund ETF (HVPW). It has $52 million in AUM and an expense ratio of 95 bps. Every two months, it sells 15% OTM cash-secured puts on 20 of the largest stocks with the highest impliedvolatility.

PROTECT & PARTICIPATE: MANAGING DRAWDOWNS WITH TREND Returns are gross of all fees, including management fees, transaction costs, and taxes. A few important takeaways: Trend following is not a risk panacea. Even with trend following applied, drawdowns in excess of 15% occurred in each of these cases. This is the cost of market participation, which will address a bit later. S4E4 - TINA LINDSTROM S4E4 – Tina Lindstrom. Tina Lindstrom is a Partner at First NY, where she manages an oil volatility portfolio. She began her career at Susquehanna and eventually worked her way up to managing both the high cap equity index group and the commodity volatility group. This gives her the unique perspective to be able to compare and contrast how A SHOCK TO THE COVARIANCE SYSTEM Corey is co-founder and Chief Investment Officer of Newfound Research, a quantitative asset manager offering a suite of separately managed accounts and mutual funds.At Newfound, Corey is responsible for portfolio management, investment research, strategy development, and communication of the firm's views to clients. NEWFOUND RESEARCHABOUT USINVESTPODCASTRESEARCHCONTACT USLIQUIDITYCASCADES

Newfound Research LLC is a quantitative investment and research firm. The firm was founded in August 2008. We currently serve financial advisors via open-end mutual funds, ETFs, and separately managed accounts through most major model manager platforms / TAMPs. For qualified firms, we offer model delivery and customized mandatesolutions.

RESEARCH LIBRARY

Explore Newfound Research's weekly quantitative research notes on tactical allocation, style premia, risk management, and craftsmanship. S4E2 - DARRIN JOHNSON Darrin Johnson is the first independent trader I’ve interviewed for this show and with that distinction he brings an entirely new perspective. After learning about how Darrin began his career as an independent trader, we get into the bulk of the conversation that circles around his process of shorting volatility in the S&P 500complex,

LIQUIDITY CASCADES

A central property of a complex system is the possible occurrence of coherent large-scale collective behaviors with a very rich structure, resulting from the repeated non-linear interactions among its constituents: the whole turns out to be much more than the sum of itsparts.

DIVERSIFICATION WITH PORTABLE BETA PODCAST | FLIRTING WITH MODELS Flirting with Models is the show that aims to pull back the curtain and meet the investors who research, design, develop, and manage quantitative investment strategies. Join Corey Hoffstein, Chief Investment Officer of Newfound Research, on a journey to explore systematic investment strategies, ranging from value to momentum and merger arbitrage to managed futures. If UNDERSTANDING DYNAMIC, VOLATILITY- ADJUSTED MOMENTUM UNDERSTANDING THE DYNAMIC WINDOW 5 Price Series Trend Noise = + Consider decomposing a price series into trend and noise: The variable m determines how strongly the price series trends; the variable a determines how volatile the price series is. Momentum systems seek to 2 WAYS TO LOWER PORTFOLIO DRAWDOWN From 2012-2019, Justin Sibears served as Managing Director and Portfolio Manager at Newfound Research. At Newfound, Justin was responsible for portfolio management, investment research, strategy development, and communication of the firm's views to clients. UNDERSTANDING OPTIMIZATION: ERRORS IN OPTIMIZATION In the last post of the series, Understanding Optimization: Intuition, we provided an overview of what optimization is and provided an intuition for how it works for non-practitioners. We left off with an image of the Rastrigin function, a complex terrain of hills and valleys that would stump our naive optimization methods. PUT-WRITE ETFS AS ALTERNATIVE INCOME OPTIONS In a previous post, we covered buy-write strategies and related ETFs, which are currently offering very attractive yield levels. Today, we’ll look a bit further into the buy-write’s cousin, the put-write. What is a Put-Write Strategy? Like buy-writes, put-writes also earn income by writing options to collect premiums with the hope that the options will expire worthless. NEWFOUND RESEARCHABOUT USINVESTPODCASTRESEARCHCONTACT USLIQUIDITYCASCADES

Newfound Research LLC is a quantitative investment and research firm. The firm was founded in August 2008. We currently serve financial advisors via open-end mutual funds, ETFs, and separately managed accounts through most major model manager platforms / TAMPs. For qualified firms, we offer model delivery and customized mandatesolutions.

RESEARCH LIBRARY

Explore Newfound Research's weekly quantitative research notes on tactical allocation, style premia, risk management, and craftsmanship. S4E2 - DARRIN JOHNSON Darrin Johnson is the first independent trader I’ve interviewed for this show and with that distinction he brings an entirely new perspective. After learning about how Darrin began his career as an independent trader, we get into the bulk of the conversation that circles around his process of shorting volatility in the S&P 500complex,

LIQUIDITY CASCADES

A central property of a complex system is the possible occurrence of coherent large-scale collective behaviors with a very rich structure, resulting from the repeated non-linear interactions among its constituents: the whole turns out to be much more than the sum of itsparts.

DIVERSIFICATION WITH PORTABLE BETA PODCAST | FLIRTING WITH MODELS Flirting with Models is the show that aims to pull back the curtain and meet the investors who research, design, develop, and manage quantitative investment strategies. Join Corey Hoffstein, Chief Investment Officer of Newfound Research, on a journey to explore systematic investment strategies, ranging from value to momentum and merger arbitrage to managed futures. If UNDERSTANDING DYNAMIC, VOLATILITY- ADJUSTED MOMENTUM UNDERSTANDING THE DYNAMIC WINDOW 5 Price Series Trend Noise = + Consider decomposing a price series into trend and noise: The variable m determines how strongly the price series trends; the variable a determines how volatile the price series is. Momentum systems seek to 2 WAYS TO LOWER PORTFOLIO DRAWDOWN From 2012-2019, Justin Sibears served as Managing Director and Portfolio Manager at Newfound Research. At Newfound, Justin was responsible for portfolio management, investment research, strategy development, and communication of the firm's views to clients. UNDERSTANDING OPTIMIZATION: ERRORS IN OPTIMIZATION In the last post of the series, Understanding Optimization: Intuition, we provided an overview of what optimization is and provided an intuition for how it works for non-practitioners. We left off with an image of the Rastrigin function, a complex terrain of hills and valleys that would stump our naive optimization methods. PUT-WRITE ETFS AS ALTERNATIVE INCOME OPTIONS In a previous post, we covered buy-write strategies and related ETFs, which are currently offering very attractive yield levels. Today, we’ll look a bit further into the buy-write’s cousin, the put-write. What is a Put-Write Strategy? Like buy-writes, put-writes also earn income by writing options to collect premiums with the hope that the options will expire worthless.TREND EQUITY

A Little, But Frequently. Our journal-published research suggests that the simple choice of when a strategy rebalances can have a significant impact on realized strategy results. In an effort to avoid this risk, the Newfound/ReSolve Robust Equity Momentum Index adopts a OPTION-BASED TREND FOLLOWING Nathan is a Portfolio Manager at Newfound Research, a quantitative asset manager offering a suite of separately managed accounts and mutual funds.At Newfound, Nathan is responsible for investment research, strategy development, and supporting the portfoliomanagement team.

TAIL HEDGING

Corey is co-founder and Chief Investment Officer of Newfound Research, a quantitative asset manager offering a suite of separately managed accounts and mutual funds.At Newfound, Corey is responsible for portfolio management, investment research, strategy development, and communication of the firm's views to clients. S4E5 - GUILLERMO RODITI DOMINGUEZ In this episode I speak with Guillermo Roditi Dominguez, managing director at New River Investments. This was one of the more unique and wide-ranging conversations I have had on the podcast to date. We begin by discussing Guillermo’s approach to portfolio construction, which is heavily focused on the idea of under-writing risk. How he goes TIMING TREND MODEL SPECIFICATION WITH MOMENTUM Corey is co-founder and Chief Investment Officer of Newfound Research, a quantitative asset manager offering a suite of separately managed accounts and mutual funds.At Newfound, Corey is responsible for portfolio management, investment research, strategy development, and communication of the firm's views to clients. S4E4 - TINA LINDSTROM Tina Lindstrom is a Partner at First NY, where she manages an oil volatility portfolio. She began her career at Susquehanna and eventually worked her way up to managing both the high cap equity index group and the commodity volatility group. This gives her the unique perspective to be able to compare and contrast how UNDERSTANDING OPTIMIZATION: ERRORS IN OPTIMIZATION In the last post of the series, Understanding Optimization: Intuition, we provided an overview of what optimization is and provided an intuition for how it works for non-practitioners. We left off with an image of the Rastrigin function, a complex terrain of hills and valleys that would stump our naive optimization methods. PROTECT & PARTICIPATE: MANAGING DRAWDOWNS WITH TREND Corey is co-founder and Chief Investment Officer of Newfound Research, a quantitative asset manager offering a suite of separately managed accounts and mutual funds.At Newfound, Corey is responsible for portfolio management, investment research, strategy development, and communication of the firm's views to clients. PUT-WRITE ETFS AS ALTERNATIVE INCOME OPTIONS In a previous post, we covered buy-write strategies and related ETFs, which are currently offering very attractive yield levels. Today, we’ll look a bit further into the buy-write’s cousin, the put-write. What is a Put-Write Strategy? Like buy-writes, put-writes also earn income by writing options to collect premiums with the hope that the options will expire worthless. A SHOCK TO THE COVARIANCE SYSTEM Corey is co-founder and Chief Investment Officer of Newfound Research, a quantitative asset manager offering a suite of separately managed accounts and mutual funds.At Newfound, Corey is responsible for portfolio management, investment research, strategy development, and communication of the firm's views to clients. NEWFOUND RESEARCHABOUT USINVESTPODCASTRESEARCHCONTACT USLIQUIDITYCASCADES

Newfound Research LLC is a quantitative investment and research firm. The firm was founded in August 2008. We currently serve financial advisors via open-end mutual funds, ETFs, and separately managed accounts through most major model manager platforms / TAMPs. For qualified firms, we offer model delivery and customized mandatesolutions.

RESEARCH LIBRARY

Explore Newfound Research's weekly quantitative research notes on tactical allocation, style premia, risk management, and craftsmanship. S4E2 - DARRIN JOHNSON Darrin Johnson is the first independent trader I’ve interviewed for this show and with that distinction he brings an entirely new perspective. After learning about how Darrin began his career as an independent trader, we get into the bulk of the conversation that circles around his process of shorting volatility in the S&P 500complex,

LIQUIDITY CASCADES

A central property of a complex system is the possible occurrence of coherent large-scale collective behaviors with a very rich structure, resulting from the repeated non-linear interactions among its constituents: the whole turns out to be much more than the sum of itsparts.

DIVERSIFICATION WITH PORTABLE BETA PODCAST | FLIRTING WITH MODELS Flirting with Models is the show that aims to pull back the curtain and meet the investors who research, design, develop, and manage quantitative investment strategies. Join Corey Hoffstein, Chief Investment Officer of Newfound Research, on a journey to explore systematic investment strategies, ranging from value to momentum and merger arbitrage to managed futures. If UNDERSTANDING DYNAMIC, VOLATILITY- ADJUSTED MOMENTUM UNDERSTANDING THE DYNAMIC WINDOW 5 Price Series Trend Noise = + Consider decomposing a price series into trend and noise: The variable m determines how strongly the price series trends; the variable a determines how volatile the price series is. Momentum systems seek to 2 WAYS TO LOWER PORTFOLIO DRAWDOWN From 2012-2019, Justin Sibears served as Managing Director and Portfolio Manager at Newfound Research. At Newfound, Justin was responsible for portfolio management, investment research, strategy development, and communication of the firm's views to clients. UNDERSTANDING OPTIMIZATION: ERRORS IN OPTIMIZATION In the last post of the series, Understanding Optimization: Intuition, we provided an overview of what optimization is and provided an intuition for how it works for non-practitioners. We left off with an image of the Rastrigin function, a complex terrain of hills and valleys that would stump our naive optimization methods. PUT-WRITE ETFS AS ALTERNATIVE INCOME OPTIONS In a previous post, we covered buy-write strategies and related ETFs, which are currently offering very attractive yield levels. Today, we’ll look a bit further into the buy-write’s cousin, the put-write. What is a Put-Write Strategy? Like buy-writes, put-writes also earn income by writing options to collect premiums with the hope that the options will expire worthless. NEWFOUND RESEARCHABOUT USINVESTPODCASTRESEARCHCONTACT USLIQUIDITYCASCADES

Newfound Research LLC is a quantitative investment and research firm. The firm was founded in August 2008. We currently serve financial advisors via open-end mutual funds, ETFs, and separately managed accounts through most major model manager platforms / TAMPs. For qualified firms, we offer model delivery and customized mandatesolutions.

RESEARCH LIBRARY

Explore Newfound Research's weekly quantitative research notes on tactical allocation, style premia, risk management, and craftsmanship. S4E2 - DARRIN JOHNSON Darrin Johnson is the first independent trader I’ve interviewed for this show and with that distinction he brings an entirely new perspective. After learning about how Darrin began his career as an independent trader, we get into the bulk of the conversation that circles around his process of shorting volatility in the S&P 500complex,

LIQUIDITY CASCADES

A central property of a complex system is the possible occurrence of coherent large-scale collective behaviors with a very rich structure, resulting from the repeated non-linear interactions among its constituents: the whole turns out to be much more than the sum of itsparts.

DIVERSIFICATION WITH PORTABLE BETA PODCAST | FLIRTING WITH MODELS Flirting with Models is the show that aims to pull back the curtain and meet the investors who research, design, develop, and manage quantitative investment strategies. Join Corey Hoffstein, Chief Investment Officer of Newfound Research, on a journey to explore systematic investment strategies, ranging from value to momentum and merger arbitrage to managed futures. If UNDERSTANDING DYNAMIC, VOLATILITY- ADJUSTED MOMENTUM UNDERSTANDING THE DYNAMIC WINDOW 5 Price Series Trend Noise = + Consider decomposing a price series into trend and noise: The variable m determines how strongly the price series trends; the variable a determines how volatile the price series is. Momentum systems seek to 2 WAYS TO LOWER PORTFOLIO DRAWDOWN From 2012-2019, Justin Sibears served as Managing Director and Portfolio Manager at Newfound Research. At Newfound, Justin was responsible for portfolio management, investment research, strategy development, and communication of the firm's views to clients. UNDERSTANDING OPTIMIZATION: ERRORS IN OPTIMIZATION In the last post of the series, Understanding Optimization: Intuition, we provided an overview of what optimization is and provided an intuition for how it works for non-practitioners. We left off with an image of the Rastrigin function, a complex terrain of hills and valleys that would stump our naive optimization methods. PUT-WRITE ETFS AS ALTERNATIVE INCOME OPTIONS In a previous post, we covered buy-write strategies and related ETFs, which are currently offering very attractive yield levels. Today, we’ll look a bit further into the buy-write’s cousin, the put-write. What is a Put-Write Strategy? Like buy-writes, put-writes also earn income by writing options to collect premiums with the hope that the options will expire worthless.TREND EQUITY

A Little, But Frequently. Our journal-published research suggests that the simple choice of when a strategy rebalances can have a significant impact on realized strategy results. In an effort to avoid this risk, the Newfound/ReSolve Robust Equity Momentum Index adopts a OPTION-BASED TREND FOLLOWING Nathan is a Portfolio Manager at Newfound Research, a quantitative asset manager offering a suite of separately managed accounts and mutual funds.At Newfound, Nathan is responsible for investment research, strategy development, and supporting the portfoliomanagement team.

TAIL HEDGING

Corey is co-founder and Chief Investment Officer of Newfound Research, a quantitative asset manager offering a suite of separately managed accounts and mutual funds.At Newfound, Corey is responsible for portfolio management, investment research, strategy development, and communication of the firm's views to clients. S4E5 - GUILLERMO RODITI DOMINGUEZ In this episode I speak with Guillermo Roditi Dominguez, managing director at New River Investments. This was one of the more unique and wide-ranging conversations I have had on the podcast to date. We begin by discussing Guillermo’s approach to portfolio construction, which is heavily focused on the idea of under-writing risk. How he goes TIMING TREND MODEL SPECIFICATION WITH MOMENTUM Corey is co-founder and Chief Investment Officer of Newfound Research, a quantitative asset manager offering a suite of separately managed accounts and mutual funds.At Newfound, Corey is responsible for portfolio management, investment research, strategy development, and communication of the firm's views to clients. S4E4 - TINA LINDSTROM Tina Lindstrom is a Partner at First NY, where she manages an oil volatility portfolio. She began her career at Susquehanna and eventually worked her way up to managing both the high cap equity index group and the commodity volatility group. This gives her the unique perspective to be able to compare and contrast how UNDERSTANDING OPTIMIZATION: ERRORS IN OPTIMIZATION In the last post of the series, Understanding Optimization: Intuition, we provided an overview of what optimization is and provided an intuition for how it works for non-practitioners. We left off with an image of the Rastrigin function, a complex terrain of hills and valleys that would stump our naive optimization methods. PROTECT & PARTICIPATE: MANAGING DRAWDOWNS WITH TREND Corey is co-founder and Chief Investment Officer of Newfound Research, a quantitative asset manager offering a suite of separately managed accounts and mutual funds.At Newfound, Corey is responsible for portfolio management, investment research, strategy development, and communication of the firm's views to clients. PUT-WRITE ETFS AS ALTERNATIVE INCOME OPTIONS In a previous post, we covered buy-write strategies and related ETFs, which are currently offering very attractive yield levels. Today, we’ll look a bit further into the buy-write’s cousin, the put-write. What is a Put-Write Strategy? Like buy-writes, put-writes also earn income by writing options to collect premiums with the hope that the options will expire worthless. A SHOCK TO THE COVARIANCE SYSTEM Corey is co-founder and Chief Investment Officer of Newfound Research, a quantitative asset manager offering a suite of separately managed accounts and mutual funds.At Newfound, Corey is responsible for portfolio management, investment research, strategy development, and communication of the firm's views to clients. NEWFOUND RESEARCHABOUT USINVESTPODCASTRESEARCHCONTACT USLIQUIDITYCASCADES

Newfound Research LLC is a quantitative investment and research firm. The firm was founded in August 2008. We currently serve financial advisors via open-end mutual funds, ETFs, and separately managed accounts through most major model manager platforms / TAMPs. For qualified firms, we offer model delivery and customized mandatesolutions.

RESEARCH LIBRARY

We explore the application of tactical signals to a rolling put strategy, seeking to minimize long-term costs while still providing meaningful protection. Read more. Flirting with Models, Season 3. We've begun releasing episodes of Season 3 of Flirting wiith Models and will continue to release throughout July 2020. S4E2 - DARRIN JOHNSON S4E2 – Darrin Johnson. Darrin Johnson is the first independent trader I’ve interviewed for this show and with that distinction he brings an entirely new perspective. After learning about how Darrin began his career as an independent trader, we get into the bulk of the conversation that circles around his process of shorting volatility in OPTION-BASED TREND FOLLOWINGTAIL HEDGING

ENSEMBLES AND REBALANCING While seemingly random, there is nothing particularly magical about these signals. The holding period was selected to align with approximately 1/12 th of the evaluation period, to match the usual 1-year lookback with 1-month holding period.; Dubikovsky, Vladislav and Susinno, Gabriele, Demystifying Rebalancing Premium and Extending Portfolio Theory in the Process (May 20, 2015). PODCAST | FLIRTING WITH MODELS Flirting with Models is the show that aims to pull back the curtain and meet the investors who research, design, develop, and manage quantitative investment strategies. Join Corey Hoffstein, Chief Investment Officer of Newfound Research, on a journey to explore systematic investment strategies, ranging from value to momentum and merger arbitrage to managed futures. If S4E4 - TINA LINDSTROM Tina Lindstrom is a Partner at First NY, where she manages an oil volatility portfolio. She began her career at Susquehanna and eventually worked her way up to managing both the high cap equity index group and the commodity volatility group. This gives her the unique perspective to be able to compare and contrast how PUT-WRITE ETFS AS ALTERNATIVE INCOME OPTIONS Put-Write ETFs. or more appropriately, ETF. Currently, the only ETF available for put-write strategies is the U.S. Equity High Volatility Put Write Index Fund ETF (HVPW). It has $52 million in AUM and an expense ratio of 95 bps. Every two months, it sells 15% OTM cash-secured puts on 20 of the largest stocks with the highest impliedvolatility.

2 WAYS TO LOWER PORTFOLIO DRAWDOWN As a simple example, say that an equity portfolio is 100% allocated to the S&P 500 ETF SPY. Over the last ten years, SPY has returned 7.7% with volatility of 21.0%*. The largest peak to trough loss – otherwise known as the max drawdown – over the period was 55.2%. Now consider a made-up tactical strategy: the Benjamin Button Strategy NEWFOUND RESEARCHABOUT USINVESTPODCASTRESEARCHCONTACT USLIQUIDITYCASCADES

Newfound Research LLC is a quantitative investment and research firm. The firm was founded in August 2008. We currently serve financial advisors via open-end mutual funds, ETFs, and separately managed accounts through most major model manager platforms / TAMPs. For qualified firms, we offer model delivery and customized mandatesolutions.

RESEARCH LIBRARY

We explore the application of tactical signals to a rolling put strategy, seeking to minimize long-term costs while still providing meaningful protection. Read more. Flirting with Models, Season 3. We've begun releasing episodes of Season 3 of Flirting wiith Models and will continue to release throughout July 2020. S4E2 - DARRIN JOHNSON S4E2 – Darrin Johnson. Darrin Johnson is the first independent trader I’ve interviewed for this show and with that distinction he brings an entirely new perspective. After learning about how Darrin began his career as an independent trader, we get into the bulk of the conversation that circles around his process of shorting volatility in OPTION-BASED TREND FOLLOWINGTAIL HEDGING

ENSEMBLES AND REBALANCING While seemingly random, there is nothing particularly magical about these signals. The holding period was selected to align with approximately 1/12 th of the evaluation period, to match the usual 1-year lookback with 1-month holding period.; Dubikovsky, Vladislav and Susinno, Gabriele, Demystifying Rebalancing Premium and Extending Portfolio Theory in the Process (May 20, 2015). PODCAST | FLIRTING WITH MODELS Flirting with Models is the show that aims to pull back the curtain and meet the investors who research, design, develop, and manage quantitative investment strategies. Join Corey Hoffstein, Chief Investment Officer of Newfound Research, on a journey to explore systematic investment strategies, ranging from value to momentum and merger arbitrage to managed futures. If S4E4 - TINA LINDSTROM Tina Lindstrom is a Partner at First NY, where she manages an oil volatility portfolio. She began her career at Susquehanna and eventually worked her way up to managing both the high cap equity index group and the commodity volatility group. This gives her the unique perspective to be able to compare and contrast how PUT-WRITE ETFS AS ALTERNATIVE INCOME OPTIONS Put-Write ETFs. or more appropriately, ETF. Currently, the only ETF available for put-write strategies is the U.S. Equity High Volatility Put Write Index Fund ETF (HVPW). It has $52 million in AUM and an expense ratio of 95 bps. Every two months, it sells 15% OTM cash-secured puts on 20 of the largest stocks with the highest impliedvolatility.

2 WAYS TO LOWER PORTFOLIO DRAWDOWN As a simple example, say that an equity portfolio is 100% allocated to the S&P 500 ETF SPY. Over the last ten years, SPY has returned 7.7% with volatility of 21.0%*. The largest peak to trough loss – otherwise known as the max drawdown – over the period was 55.2%. Now consider a made-up tactical strategy: the Benjamin Button Strategy PAPERS | NEWFOUND RESEARCH Prior research and empirical investment results have shown that portfolio construction choices related to rebalance schedules may have non-trivial impacts on realized performance. We construct long-only indices that provide exposures to popular U.S. equity factors (value, size, momentum, quality, and low volatility) and vary their rebalanceTAIL HEDGING

30% OTM Strategy: Buy a 3-month 30% OTM put on February 21 st and sell a 2-month 1.4% ITM put on March 20 th. When bought, the option had an implied volatility of 35.0% and a price of $5.42; when sold it had an implied volatility of 53.8% and a price of $425.85 for a 7757% return. A MODERN, BEHAVIOR-AWARE APPROACH TO ASSET ALLOCATION AND Newfound Research LLC | 425 Boylston Street, 3rd Floor | Boston, MA 02116 | p: 617-531-9773 | w: thinknewfound.com Case #5239056 A Modern, Behavior-Aware Approach to Asset Allocation and Portfolio Construction December 2016 Corey M. Hoffstein DIVERSIFICATION WITH PORTABLE BETA Conclusion. In this research note, we explored diversification in a long/flat tactical equity strategy with a portable beta bond overlay. By decomposing the strategy into its passive holdings (50/50 stock/bond portfolio and U.S. Treasury futures) and active long/short overlays (trend equity, bond carry, bond momentum, and bond value), wefound

FLIRTING WITH MODELS™ Explore Newfound Research's weekly quantitative research notes on tactical allocation, style premia, risk management, and craftsmanship. S5E5 - ANGUS CAMERON Angus Cameron is the Founder and CIO of Liminal Capital, a machine-learning focused investment manager. But Angus does not come to markets with a computer science PhD. Rather, his career arc took him through the prop desks and buyside of Asia, trading global fixed income, FX, equity markets, and arbitrage strategies on a discretionary basis. PODCAST | FLIRTING WITH MODELS Flirting with Models is the show that aims to pull back the curtain and meet the investors who research, design, develop, and manage quantitative investment strategies. Join Corey Hoffstein, Chief Investment Officer of Newfound Research, on a journey to explore systematic investment strategies, ranging from value to momentum and merger arbitrage to managed futures. If S4E5 - GUILLERMO RODITI DOMINGUEZ In this episode I speak with Guillermo Roditi Dominguez, managing director at New River Investments. This was one of the more unique and wide-ranging conversations I have had on the podcast to date. We begin by discussing Guillermo’s approach to portfolio construction, which is heavily focused on the idea of under-writing risk. How he goes LEVERED ETFS FOR THE LONG RUN? When L=1, we have a standard long-only investment. When L=2, we have our 2X daily levered ETFs. What we see is that when L=1, our drag is simply –X% 2.. When L=2, however, our drag is 4X% 2.. When L=3, the drag skyrockets to 9X% 2.. Of course, the so-called drag turns into a benefit in trending markets (whether positive or negative). BUILDING BETTER BACKTESTS Summary. Backtests should be, and frequently are, evaluated with scrutiny and skepticism. While hypothetical results – backtested or live – are reported as a single, precise number, investors will have different performance based on. In most hypothetical results, this execution factor is often ignored. To more accurately reporthypothetical

Loading...

__

* Strategies

* How to Invest__

* Separately Managed Accounts* Mutual Funds

* ETFs

* Insights__

* Research

* Equity Style Dashboard * Quantitative Signals* Papers

* Podcast

* About Us__

* Contact

* MyNFR__

* Login

* Register

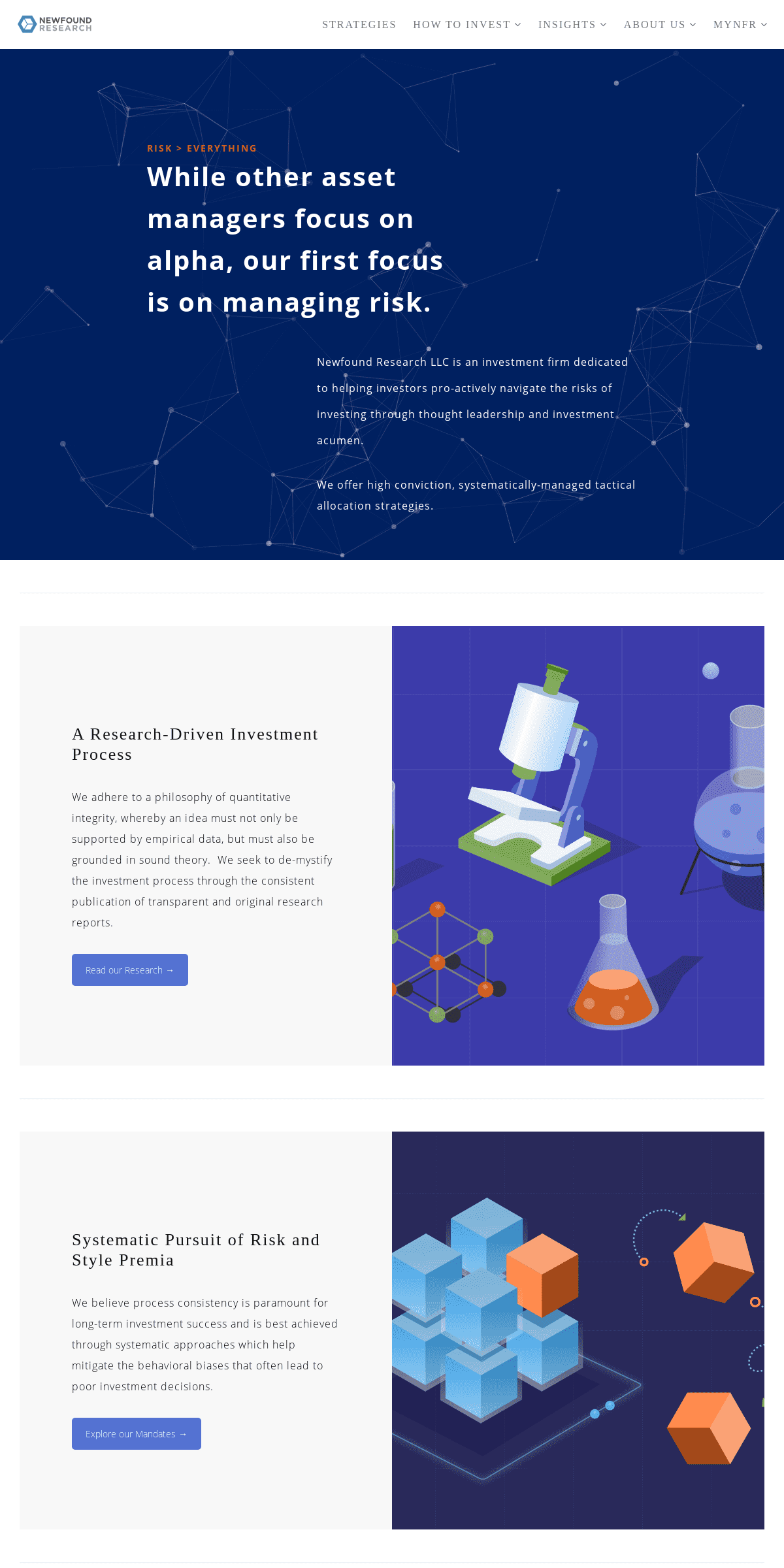

Risk > Everything

While other asset managers focus on alpha, our first focus is onmanaging risk.

Newfound Research LLC is an investment firm dedicated to helping investors pro-actively navigate the risks of investing through thought leadership and investment acumen. We offer high conviction, systematically-managed tactical allocationstrategies.

------------------------- A RESEARCH-DRIVEN INVESTMENT PROCESS We adhere to a philosophy of quantitative integrity, whereby an idea must not only be supported by empirical data, but must also be grounded in sound theory. We seek to de-mystify the investment process through the consistent publication of transparent and originalresearch reports.

Read our Research → ------------------------- SYSTEMATIC PURSUIT OF RISK AND STYLE PREMIA We believe process consistency is paramount for long-term investment success and is best achieved through systematic approaches which help mitigate the behavioral biases that often lead to poor investmentdecisions.

Explore our Mandates → ------------------------- BALANCING SIMPLICITY AND COMPLEXITY WITH THOUGHTFUL DESIGN Our portfolios are built around a holistic view of diversification which considers not only what a strategy invests in, but also how and when those decisions are made. Access our Strategies → -------------------------FEATURED RESEARCH

NO PAIN, NO PREMIUM

DID DECLINING RATES ACTUALLY MATTER? REBALANCE TIMING LUCK: THE DIFFERENCE BETWEEN HIRED & FIRED TWO CENTURIES OF MOMENTUM FRAGILITY CASE STUDY: DUAL MOMENTUM GEM WHEN SIMPLICITY MET FRAGILITY Start asking questions. In investing, the journey is just as important as the destination. Learn more about our philosophy and process. We want to hear fromyou.

Talk to the Team →ADDITIONAL LINKS

* About Us

* Investment Strategies* How to Invest

* Mutual Funds

* Bespoke Solutions

* Research Commentary* Contact

* Form ADV

FROM THE BLOG

* 2020 Q1 Investor Letter * A L-U-V-Wy Recovery * One Hedge to Rule Them All* What the Trend

* How I Invest

RESEARCH COMMENTARY

SUBSCRIPTIONS

* Weekly Commentary

* Video Digest

* Monthly Performance UpdateSubscribe

Browse Archive

------------------------- � Newfound Research 2020.__

__

You are about to leave the Newfound Research LLC website. The following link may contain information concerning investments, products or other information. Newfound Research LLC is not responsible for the accuracy or completeness of information on non-affiliated websites and does not make any representation regarding the advisability of investing in any investment fund or other investment product or vehicle. Importantly, Newfound Research LLC is not compensated for linking you to any non-affiliated website and instead is only compensated with an asset-based fee in the limited capacities as either a licensor of intellectual property or a sub-adviser to an investment adviser. The material available on non-affiliated websites has been produced by entities that are not affiliated with Newfound Research LLC. Descriptions of, references to, or links to products or publications within any non-affiliated linked website does not imply endorsement or recommendation of that product or publication by Newfound Research LLC. Any opinions or recommendations from non-affiliated websites are solely those of the independent providers and are not the opinions or recommendations of Newfound Research LLC, which is not responsible for any inaccuracies or errors. THIS INFORMATION IS NOT AN OFFER TO BUY OR A SOLICITATION TO SELL ANY SECURITY OR INVESTMENT PRODUCT. SUCH AN OFFER OR SOLICITATION IS MADE ONLY BY THE SECURITIES’ OR INVESTMENT PRODUCTS’ ISSUER OR SPONSOR THROUGH A PROSPECTUS OR OTHER OFFERINGDOCUMENTATION.

Confirmation Required Close You are about to leave the Newfound Research LLC website and are being re-directed to the Newfound Research Mutual Funds website. Please note that Newfound Research Mutual Funds site may be subject to rules and regulations that may differ significantly from those to which the Newfound Research website is subject and may not be appropriate for use by residents in all jurisdictions.Details

5