2

More Annotations

3

4

Favourite Annotations

3

3

Text

PENSIONERS « WHO CAN CLAIM UNIVERSAL CREDIT « GUIDANCE Currently, pension claimants are expected to claim help towards their housing costs through housing benefit. Capital. In pension credit, for each £500 of capital over £10,000, £1 is added to the person's income when calculating their entitlement. In UC, for each £250 of capital over £6,000, £4.35 a month is added to the person's income CH2 NOTES - CHILD BENEFIT CLAIM FORM - GETTING IT RIGHT CH2 Notes Child Benefit claim form - Getting it right Use these notes to help you www.hmrc.gov.uk Our helpline number: 0845 302 1444 Our

textphone number:

MANAGED MIGRATION « EXISTING TAX CREDIT CLAIMANTS Universal credit: Managed migration - Move to UC . This page explains the managed migration exercise - this is where DWP/HMRC move claimants from tax credits (and other legacy benefits) across to Universal Credit (UC) under a formal exercise, which is sometimes referred to as ‘Move to UC’ by DWP. PENSION INCOME « WHAT IS INCOME « HOW DO TAX CREDITS WORK Pension income for tax credits mirrors the tax treatment. It includes the following taxable pension payments and annuities: income from UK social security pensions, ie the state retirement pension, graduated retirement benefit, industrial death benefit, widowed mother’s allowance, widowed parent’s allowance, and widow’s pension (ITEPA THE ANNUAL CYCLE « HOW DO TAX CREDITS WORK? « GUIDANCE Tax credits, unlike other benefits, follow an annual cycle based on the tax year (6 April – 5 April). We have created a pdf timeline that explains the basic annual tax credits cycle. Use the links below to find out more information about: Claims starting: This section explains what happens when HMRC receive a tax credits claim, whatcounts as

BEREAVEMENT « CHANGES OF CIRCUMSTANCES « HOW DO TAX Tax Credits: Bereavement. When a tax credit claimant dies, or a child who is included in a tax credit claim dies, this is a change of circumstances which must be notified to HMRC within 1 month. This has been temporarily extended to 3 months from 23rd May 2020 for critical workers due to the coronavirus pandemic. SURPLUS EARNINGS AND LOSSES « SELF-EMPLOYMENT Self-employment: Surplus earnings and losses . The surplus earnings and loss rules apply from April 2018. These are very complex rules and we have written this guidance to help advisers understand the rules.TC603RD NOTES

TC603RD Notes – for use from 6 April 2012 Renewing your tax credits – Getting it right Use these notes to help you Renew now– don’t risk leaving it until 31 July INTERMEDIARIES REGISTERED WITH HMRC CAN SEND TC689S 3 December 2012 . Intermediaries registered with HMRC can send TC689s electronically HMRC have advised that from 3 December, registered Intermediaries (those with an office ID number (OIN)) can send urgent TC689s electronically instead of using the existing fax route .. The electronic TC689 (known as KANA 689) has been tested and can be found here.. It is intended that this will RECONFIRMATION PROCESS « MAKING A CLAIM « HOW DOES TAX Welcome to our new Tax-Free Childcare guidance pages . We are currently building this section of the website. New material will be added gradually and there may be changes to links, pages and navigation as we add more material. PENSIONERS « WHO CAN CLAIM UNIVERSAL CREDIT « GUIDANCE Currently, pension claimants are expected to claim help towards their housing costs through housing benefit. Capital. In pension credit, for each £500 of capital over £10,000, £1 is added to the person's income when calculating their entitlement. In UC, for each £250 of capital over £6,000, £4.35 a month is added to the person's income CH2 NOTES - CHILD BENEFIT CLAIM FORM - GETTING IT RIGHT CH2 Notes Child Benefit claim form - Getting it right Use these notes to help you www.hmrc.gov.uk Our helpline number: 0845 302 1444 Ourtextphone number:

MANAGED MIGRATION « EXISTING TAX CREDIT CLAIMANTS Universal credit: Managed migration - Move to UC . This page explains the managed migration exercise - this is where DWP/HMRC move claimants from tax credits (and other legacy benefits) across to Universal Credit (UC) under a formal exercise, which is sometimes referred to as ‘Move to UC’ by DWP. PENSION INCOME « WHAT IS INCOME « HOW DO TAX CREDITS WORK Pension income for tax credits mirrors the tax treatment. It includes the following taxable pension payments and annuities: income from UK social security pensions, ie the state retirement pension, graduated retirement benefit, industrial death benefit, widowed mother’s allowance, widowed parent’s allowance, and widow’s pension (ITEPA THE ANNUAL CYCLE « HOW DO TAX CREDITS WORK? « GUIDANCE Tax credits, unlike other benefits, follow an annual cycle based on the tax year (6 April – 5 April). We have created a pdf timeline that explains the basic annual tax credits cycle. Use the links below to find out more information about: Claims starting: This section explains what happens when HMRC receive a tax credits claim, whatcounts as

BEREAVEMENT « CHANGES OF CIRCUMSTANCES « HOW DO TAX Tax Credits: Bereavement. When a tax credit claimant dies, or a child who is included in a tax credit claim dies, this is a change of circumstances which must be notified to HMRC within 1 month. This has been temporarily extended to 3 months from 23rd May 2020 for critical workers due to the coronavirus pandemic. SURPLUS EARNINGS AND LOSSES « SELF-EMPLOYMENT Self-employment: Surplus earnings and losses . The surplus earnings and loss rules apply from April 2018. These are very complex rules and we have written this guidance to help advisers understand the rules.TC603RD NOTES

TC603RD Notes – for use from 6 April 2012 Renewing your tax credits – Getting it right Use these notes to help you Renew now– don’t risk leaving it until 31 July INTERMEDIARIES REGISTERED WITH HMRC CAN SEND TC689S 3 December 2012 . Intermediaries registered with HMRC can send TC689s electronically HMRC have advised that from 3 December, registered Intermediaries (those with an office ID number (OIN)) can send urgent TC689s electronically instead of using the existing fax route .. The electronic TC689 (known as KANA 689) has been tested and can be found here.. It is intended that this will RECONFIRMATION PROCESS « MAKING A CLAIM « HOW DOES TAX Welcome to our new Tax-Free Childcare guidance pages . We are currently building this section of the website. New material will be added gradually and there may be changes to links, pages and navigation as we add more material.REVENUE BENEFITS

April 2021: We're currently updating revenuebenefits and adding new content to take account of the start of the 2021/2022 tax year. Keep checking back for the latest information. New regulations (27 May 2021): Child Benefit (General) (Coronavirus) (Amendment) Regulations 2021 (SI.No.630/2021) - New regulations amend child benefit‘terminal

TAX CREDIT RENEWALS

9 September 2020 How are the NHS test and trace self-isolation payments treated for tax credits and universal credit? CHILD TRUST FUND (CTF) 27 March 2020 Coronavirus outbreak (Covid-19) – Tax credit and Universal Credit policy announcements POLICY « UNIVERSAL CREDIT Universal Credit Policy . This section of the website covers Universal Credit policy issues. Policy changes: This section contains information about changes to Universal Credit policy that have been announced.Where changes are planned but not yet in place or the legislation is not yet published, the finer details of those policy changes may not be available. OVERPAYMENTS AND UNDERPAYMENTS « HOW DO TAX CREDITS WORK Tax Credits: Overpayments and underpayments . Overpayments and underpayments are a normal part of the tax credits system. This is because when a tax credits award is made it is not final until a final entitlement decision is made which is usually after the end of the tax year for which it has been given or shortly after a claim is ended during a tax year (where a person claims Universal Credit UNDERSTANDING SELF-EMPLOYMENT « HOW DO TAX CREDITS WORK Tax Credits: Understanding self-employment. This section covers some aspects of the tax credits system that are of particular importance for the self-employed. To be entitled to tax credits you must be in ‘qualifying remunerative work’. For claims prior to April 2015, there was no restriction on claiming WTC for people who were self CAPITAL RULES « ENTITLEMENT TO UNIVERSAL CREDIT « GUIDANCE The maximum capital limit for claiming Universal Credit is £16,000 for either a single person or a couple where that capital is held jointly. If capital is above this amount there is no entitlement to UC. Capital or joint capital over £6,000 is treated as providing income, known as “tariff income”, of £4.35 per month for eachadditional

SURPLUS EARNINGS AND LOSSES « SELF-EMPLOYMENT Self-employment: Surplus earnings and losses . The surplus earnings and loss rules apply from April 2018. These are very complex rules and we have written this guidance to help advisers understand the rules. HIGH INCOME CHILD BENEFIT CHARGE 11 June 2018 Universal Credit – extending transitional protection and delayed roll-out completion to March 2023 FOSTER CARERS « SPECIAL CIRCUMSTANCES « HOW DO TAX CREDITS Foster carers who foster children under entirely private foster arrangements where no public funds are involved may be able to claim CTC for the children they foster, providing they meet the normal qualifying rules for CTC. Income from caring and tax credits. The amount of tax credits will be based on the level of household income. ELIGIBILITY CONDITIONS « WHO CAN CLAIM? « GUIDANCE « TAX Eligibility condition 1 - Age. The claimant must be aged at least 16 at the date of declaration. Eligibility condition 2 - Responsible for the child. The claimant must, at the date of declaration, be responsible for the relevant child. The relevant child means the child who the claimant is trying to open a childcare account for or, if theyare

PENSIONERS « WHO CAN CLAIM UNIVERSAL CREDIT « GUIDANCE Currently, pension claimants are expected to claim help towards their housing costs through housing benefit. Capital. In pension credit, for each £500 of capital over £10,000, £1 is added to the person's income when calculating their entitlement. In UC, for each £250 of capital over £6,000, £4.35 a month is added to the person's income WHERE IT ALL STARTED « POLICY « CHILD BENEFIT Child Poverty Action Group (CPAG) was instrumental in ‘changing their minds’ and in 1975 the child benefit bill was enacted. The bill replaced family allowance with a benefit for each child, which was paid to the mothers. The act was not implemented MANAGED MIGRATION « EXISTING TAX CREDIT CLAIMANTS Universal credit: Managed migration - Move to UC . This page explains the managed migration exercise - this is where DWP/HMRC move claimants from tax credits (and other legacy benefits) across to Universal Credit (UC) under a formal exercise, which is sometimes referred to as ‘Move to UC’ by DWP. CH2 NOTES - CHILD BENEFIT CLAIM FORM - GETTING IT RIGHT CH2 Notes Child Benefit claim form - Getting it right Use these notes to help you www.hmrc.gov.uk Our helpline number: 0845 302 1444 Ourtextphone number:

BENEFIT CAP « ENTITLEMENT TO UNIVERSAL CREDIT « GUIDANCE The benefit cap is relevant to the final stage of calculating entitlement to UC. Firstly, the amount of excess must be calculated. This is the amount that the UC entitlement (plus any of the other benefits listed above) exceeds the benefit cap minus any amount included in the award for childcare costs. This ensures that childcarecosts are

PENSION INCOME « WHAT IS INCOME « HOW DO TAX CREDITS WORK Pension income for tax credits mirrors the tax treatment. It includes the following taxable pension payments and annuities: income from UK social security pensions, ie the state retirement pension, graduated retirement benefit, industrial death benefit, widowed mother’s allowance, widowed parent’s allowance, and widow’s pension (ITEPA SURPLUS EARNINGS AND LOSSES « SELF-EMPLOYMENT Self-employment: Surplus earnings and losses . The surplus earnings and loss rules apply from April 2018. These are very complex rules and we have written this guidance to help advisers understand the rules. CAPITAL RULES « ENTITLEMENT TO UNIVERSAL CREDIT « GUIDANCE The maximum capital limit for claiming Universal Credit is £16,000 for either a single person or a couple where that capital is held jointly. If capital is above this amount there is no entitlement to UC. Capital or joint capital over £6,000 is treated as providing income, known as “tariff income”, of £4.35 per month for eachadditional

TC603RD NOTES

TC603RD Notes – for use from 6 April 2012 Renewing your tax credits – Getting it right Use these notes to help you Renew now– don’t risk leaving it until 31 July ELIGIBILITY CONDITIONS « WHO CAN CLAIM? « GUIDANCE « TAX Eligibility condition 1 - Age. The claimant must be aged at least 16 at the date of declaration. Eligibility condition 2 - Responsible for the child. The claimant must, at the date of declaration, be responsible for the relevant child. The relevant child means the child who the claimant is trying to open a childcare account for or, if theyare

PENSIONERS « WHO CAN CLAIM UNIVERSAL CREDIT « GUIDANCE Currently, pension claimants are expected to claim help towards their housing costs through housing benefit. Capital. In pension credit, for each £500 of capital over £10,000, £1 is added to the person's income when calculating their entitlement. In UC, for each £250 of capital over £6,000, £4.35 a month is added to the person's income WHERE IT ALL STARTED « POLICY « CHILD BENEFIT Child Poverty Action Group (CPAG) was instrumental in ‘changing their minds’ and in 1975 the child benefit bill was enacted. The bill replaced family allowance with a benefit for each child, which was paid to the mothers. The act was not implemented MANAGED MIGRATION « EXISTING TAX CREDIT CLAIMANTS Universal credit: Managed migration - Move to UC . This page explains the managed migration exercise - this is where DWP/HMRC move claimants from tax credits (and other legacy benefits) across to Universal Credit (UC) under a formal exercise, which is sometimes referred to as ‘Move to UC’ by DWP. CH2 NOTES - CHILD BENEFIT CLAIM FORM - GETTING IT RIGHT CH2 Notes Child Benefit claim form - Getting it right Use these notes to help you www.hmrc.gov.uk Our helpline number: 0845 302 1444 Ourtextphone number:

BENEFIT CAP « ENTITLEMENT TO UNIVERSAL CREDIT « GUIDANCE The benefit cap is relevant to the final stage of calculating entitlement to UC. Firstly, the amount of excess must be calculated. This is the amount that the UC entitlement (plus any of the other benefits listed above) exceeds the benefit cap minus any amount included in the award for childcare costs. This ensures that childcarecosts are

PENSION INCOME « WHAT IS INCOME « HOW DO TAX CREDITS WORK Pension income for tax credits mirrors the tax treatment. It includes the following taxable pension payments and annuities: income from UK social security pensions, ie the state retirement pension, graduated retirement benefit, industrial death benefit, widowed mother’s allowance, widowed parent’s allowance, and widow’s pension (ITEPA SURPLUS EARNINGS AND LOSSES « SELF-EMPLOYMENT Self-employment: Surplus earnings and losses . The surplus earnings and loss rules apply from April 2018. These are very complex rules and we have written this guidance to help advisers understand the rules. CAPITAL RULES « ENTITLEMENT TO UNIVERSAL CREDIT « GUIDANCE The maximum capital limit for claiming Universal Credit is £16,000 for either a single person or a couple where that capital is held jointly. If capital is above this amount there is no entitlement to UC. Capital or joint capital over £6,000 is treated as providing income, known as “tariff income”, of £4.35 per month for eachadditional

TC603RD NOTES

TC603RD Notes – for use from 6 April 2012 Renewing your tax credits – Getting it right Use these notes to help you Renew now– don’t risk leaving it until 31 JulyTAX CREDIT RENEWALS

9 September 2020 How are the NHS test and trace self-isolation payments treated for tax credits and universal credit? WHERE IT ALL STARTED « POLICY « CHILD BENEFIT Child Poverty Action Group (CPAG) was instrumental in ‘changing their minds’ and in 1975 the child benefit bill was enacted. The bill replaced family allowance with a benefit for each child, which was paid to the mothers. The act was not implemented PENSION INCOME « WHAT IS INCOME « HOW DO TAX CREDITS WORK Pension income for tax credits mirrors the tax treatment. It includes the following taxable pension payments and annuities: income from UK social security pensions, ie the state retirement pension, graduated retirement benefit, industrial death benefit, widowed mother’s allowance, widowed parent’s allowance, and widow’s pension (ITEPA BENEFIT CAP « ENTITLEMENT TO UNIVERSAL CREDIT « GUIDANCE The benefit cap is relevant to the final stage of calculating entitlement to UC. Firstly, the amount of excess must be calculated. This is the amount that the UC entitlement (plus any of the other benefits listed above) exceeds the benefit cap minus any amount included in the award for childcare costs. This ensures that childcarecosts are

BEREAVEMENT « CHANGES OF CIRCUMSTANCES « HOW DO TAX Tax Credits: Bereavement. When a tax credit claimant dies, or a child who is included in a tax credit claim dies, this is a change of circumstances which must be notified to HMRC within 1 month. This has been temporarily extended to 3 months from 23rd May 2020 for critical workers due to the coronavirus pandemic. CAPITAL RULES « ENTITLEMENT TO UNIVERSAL CREDIT « GUIDANCE The maximum capital limit for claiming Universal Credit is £16,000 for either a single person or a couple where that capital is held jointly. If capital is above this amount there is no entitlement to UC. Capital or joint capital over £6,000 is treated as providing income, known as “tariff income”, of £4.35 per month for eachadditional

SURPLUS EARNINGS AND LOSSES « SELF-EMPLOYMENT Self-employment: Surplus earnings and losses . The surplus earnings and loss rules apply from April 2018. These are very complex rules and we have written this guidance to help advisers understand the rules. RTI AND UNIVERSAL CREDIT « ENTITLEMENT TO UNIVERSAL CREDIT In the past, HMRC required employers to send payments of tax and NI to them frequently and then report those figures after the end of each tax year on a series of forms. On 6 April 2013, HMRC introduced a new system of real time reporting for employers. It is often called the RTI (Real Time Information) system. CLAIMANT COMMITMENT « ENTITLEMENT TO UNIVERSAL CREDIT The claimant commitment is a record of the claimant’s responsibilities in relation to their award of UC. Where a couple claim, both members must accept a claimant commitment. Only in limited circumstances will this requirement not be imposed. It will be updated and reviewed periodically and each time it is changed the claimantmust accept the

CHANGES OF CIRCUMSTANCES « EXISTING TAX CREDIT CLAIMANTS Universal credit: Changes of circumstances . Eventually, all tax credit claimants will be asked to move to Universal Credit (UC) or pension credit (depending on age) under a managed migration exercise, known as ‘Move to UC’. Until that exercise, existing tax credit claimants are not affected by Universal Credit (UC) unless they choose to make a UC claim, need to claim another benefit that ELIGIBILITY CONDITIONS « WHO CAN CLAIM? « GUIDANCE « TAX Eligibility condition 1 - Age. The claimant must be aged at least 16 at the date of declaration. Eligibility condition 2 - Responsible for the child. The claimant must, at the date of declaration, be responsible for the relevant child. The relevant child means the child who the claimant is trying to open a childcare account for or, if theyare

WHERE IT ALL STARTED « POLICY « CHILD BENEFIT Child Poverty Action Group (CPAG) was instrumental in ‘changing their minds’ and in 1975 the child benefit bill was enacted. The bill replaced family allowance with a benefit for each child, which was paid to the mothers. The act was not implemented PENSIONERS « WHO CAN CLAIM UNIVERSAL CREDIT « GUIDANCE Currently, pension claimants are expected to claim help towards their housing costs through housing benefit. Capital. In pension credit, for each £500 of capital over £10,000, £1 is added to the person's income when calculating their entitlement. In UC, for each £250 of capital over £6,000, £4.35 a month is added to the person's income MANAGED MIGRATION « EXISTING TAX CREDIT CLAIMANTS Universal credit: Managed migration - Move to UC . This page explains the managed migration exercise - this is where DWP/HMRC move claimants from tax credits (and other legacy benefits) across to Universal Credit (UC) under a formal exercise, which is sometimes referred to as ‘Move to UC’ by DWP. BENEFIT CAP « ENTITLEMENT TO UNIVERSAL CREDIT « GUIDANCE The benefit cap is relevant to the final stage of calculating entitlement to UC. Firstly, the amount of excess must be calculated. This is the amount that the UC entitlement (plus any of the other benefits listed above) exceeds the benefit cap minus any amount included in the award for childcare costs. This ensures that childcarecosts are

CH2 NOTES - CHILD BENEFIT CLAIM FORM - GETTING IT RIGHT CH2 Notes Child Benefit claim form - Getting it right Use these notes to help you www.hmrc.gov.uk Our helpline number: 0845 302 1444 Ourtextphone number:

BEREAVEMENT « CHANGES OF CIRCUMSTANCES « HOW DO TAX Tax Credits: Bereavement. When a tax credit claimant dies, or a child who is included in a tax credit claim dies, this is a change of circumstances which must be notified to HMRC within 1 month. This has been temporarily extended to 3 months from 23rd May 2020 for critical workers due to the coronavirus pandemic. OVERPAYMENTS AND UNDERPAYMENTS « HOW DO TAX CREDITS WORK Tax Credits: Overpayments and underpayments . Overpayments and underpayments are a normal part of the tax credits system. This is because when a tax credits award is made it is not final until a final entitlement decision is made which is usually after the end of the tax year for which it has been given or shortly after a claim is ended during a tax year (where a person claims Universal Credit CAPITAL RULES « ENTITLEMENT TO UNIVERSAL CREDIT « GUIDANCE The maximum capital limit for claiming Universal Credit is £16,000 for either a single person or a couple where that capital is held jointly. If capital is above this amount there is no entitlement to UC. Capital or joint capital over £6,000 is treated as providing income, known as “tariff income”, of £4.35 per month for eachadditional

TC603RD NOTES

TC603RD Notes – for use from 6 April 2012 Renewing your tax credits – Getting it right Use these notes to help you Renew now– don’t risk leaving it until 31 July ELIGIBILITY CONDITIONS « WHO CAN CLAIM? « GUIDANCE « TAX Eligibility condition 1 - Age. The claimant must be aged at least 16 at the date of declaration. Eligibility condition 2 - Responsible for the child. The claimant must, at the date of declaration, be responsible for the relevant child. The relevant child means the child who the claimant is trying to open a childcare account for or, if theyare

WHERE IT ALL STARTED « POLICY « CHILD BENEFIT Child Poverty Action Group (CPAG) was instrumental in ‘changing their minds’ and in 1975 the child benefit bill was enacted. The bill replaced family allowance with a benefit for each child, which was paid to the mothers. The act was not implemented PENSIONERS « WHO CAN CLAIM UNIVERSAL CREDIT « GUIDANCE Currently, pension claimants are expected to claim help towards their housing costs through housing benefit. Capital. In pension credit, for each £500 of capital over £10,000, £1 is added to the person's income when calculating their entitlement. In UC, for each £250 of capital over £6,000, £4.35 a month is added to the person's income MANAGED MIGRATION « EXISTING TAX CREDIT CLAIMANTS Universal credit: Managed migration - Move to UC . This page explains the managed migration exercise - this is where DWP/HMRC move claimants from tax credits (and other legacy benefits) across to Universal Credit (UC) under a formal exercise, which is sometimes referred to as ‘Move to UC’ by DWP. BENEFIT CAP « ENTITLEMENT TO UNIVERSAL CREDIT « GUIDANCE The benefit cap is relevant to the final stage of calculating entitlement to UC. Firstly, the amount of excess must be calculated. This is the amount that the UC entitlement (plus any of the other benefits listed above) exceeds the benefit cap minus any amount included in the award for childcare costs. This ensures that childcarecosts are

CH2 NOTES - CHILD BENEFIT CLAIM FORM - GETTING IT RIGHT CH2 Notes Child Benefit claim form - Getting it right Use these notes to help you www.hmrc.gov.uk Our helpline number: 0845 302 1444 Ourtextphone number:

BEREAVEMENT « CHANGES OF CIRCUMSTANCES « HOW DO TAX Tax Credits: Bereavement. When a tax credit claimant dies, or a child who is included in a tax credit claim dies, this is a change of circumstances which must be notified to HMRC within 1 month. This has been temporarily extended to 3 months from 23rd May 2020 for critical workers due to the coronavirus pandemic. OVERPAYMENTS AND UNDERPAYMENTS « HOW DO TAX CREDITS WORK Tax Credits: Overpayments and underpayments . Overpayments and underpayments are a normal part of the tax credits system. This is because when a tax credits award is made it is not final until a final entitlement decision is made which is usually after the end of the tax year for which it has been given or shortly after a claim is ended during a tax year (where a person claims Universal Credit CAPITAL RULES « ENTITLEMENT TO UNIVERSAL CREDIT « GUIDANCE The maximum capital limit for claiming Universal Credit is £16,000 for either a single person or a couple where that capital is held jointly. If capital is above this amount there is no entitlement to UC. Capital or joint capital over £6,000 is treated as providing income, known as “tariff income”, of £4.35 per month for eachadditional

TC603RD NOTES

TC603RD Notes – for use from 6 April 2012 Renewing your tax credits – Getting it right Use these notes to help you Renew now– don’t risk leaving it until 31 JulyTAX CREDIT RENEWALS

4 June 2021 . Tax credit renewals – HMRC scams warning for tax credits customers . HMRC have issued the following message about scams JUNE, 2021 « BLOG « REVENUE BENEFITS Revenue benefits blog posts from June, 2021. 4 June 2021 | Tax credit renewals – HMRC scams warning for tax credits customersTAX CREDIT RENEWALS

9 September 2020 How are the NHS test and trace self-isolation payments treated for tax credits and universal credit? CHILD TRUST FUND (CTF) 27 March 2020 Coronavirus outbreak (Covid-19) – Tax credit and Universal Credit policy announcements WHERE IT ALL STARTED « POLICY « CHILD BENEFIT Child Poverty Action Group (CPAG) was instrumental in ‘changing their minds’ and in 1975 the child benefit bill was enacted. The bill replaced family allowance with a benefit for each child, which was paid to the mothers. The act was not implemented PENSION INCOME « WHAT IS INCOME « HOW DO TAX CREDITS WORK Pension income for tax credits mirrors the tax treatment. It includes the following taxable pension payments and annuities: income from UK social security pensions, ie the state retirement pension, graduated retirement benefit, industrial death benefit, widowed mother’s allowance, widowed parent’s allowance, and widow’s pension (ITEPA BENEFIT CAP « ENTITLEMENT TO UNIVERSAL CREDIT « GUIDANCE The benefit cap is relevant to the final stage of calculating entitlement to UC. Firstly, the amount of excess must be calculated. This is the amount that the UC entitlement (plus any of the other benefits listed above) exceeds the benefit cap minus any amount included in the award for childcare costs. This ensures that childcarecosts are

SURPLUS EARNINGS AND LOSSES « SELF-EMPLOYMENT Self-employment: Surplus earnings and losses . The surplus earnings and loss rules apply from April 2018. These are very complex rules and we have written this guidance to help advisers understand the rules. RTI AND UNIVERSAL CREDIT « ENTITLEMENT TO UNIVERSAL CREDIT In the past, HMRC required employers to send payments of tax and NI to them frequently and then report those figures after the end of each tax year on a series of forms. On 6 April 2013, HMRC introduced a new system of real time reporting for employers. It is often called the RTI (Real Time Information) system. CH2 NOTES - CHILD BENEFIT CLAIM FORM - GETTING IT RIGHT CH2 Notes Child Benefit claim form - Getting it right Use these notes to help you www.hmrc.gov.uk Our helpline number: 0845 302 1444 Ourtextphone number:

ELIGIBILITY CONDITIONS « WHO CAN CLAIM? « GUIDANCE « TAX Eligibility condition 1 - Age. The claimant must be aged at least 16 at the date of declaration. Eligibility condition 2 - Responsible for the child. The claimant must, at the date of declaration, be responsible for the relevant child. The relevant child means the child who the claimant is trying to open a childcare account for or, if theyare

WHERE IT ALL STARTED « POLICY « CHILD BENEFIT Child Poverty Action Group (CPAG) was instrumental in ‘changing their minds’ and in 1975 the child benefit bill was enacted. The bill replaced family allowance with a benefit for each child, which was paid to the mothers. The act was not implemented PENSIONERS « WHO CAN CLAIM UNIVERSAL CREDIT « GUIDANCE Currently, pension claimants are expected to claim help towards their housing costs through housing benefit. Capital. In pension credit, for each £500 of capital over £10,000, £1 is added to the person's income when calculating their entitlement. In UC, for each £250 of capital over £6,000, £4.35 a month is added to the person's income MANAGED MIGRATION « EXISTING TAX CREDIT CLAIMANTS Universal credit: Managed migration - Move to UC . This page explains the managed migration exercise - this is where DWP/HMRC move claimants from tax credits (and other legacy benefits) across to Universal Credit (UC) under a formal exercise, which is sometimes referred to as ‘Move to UC’ by DWP. BENEFIT CAP « ENTITLEMENT TO UNIVERSAL CREDIT « GUIDANCE The benefit cap is relevant to the final stage of calculating entitlement to UC. Firstly, the amount of excess must be calculated. This is the amount that the UC entitlement (plus any of the other benefits listed above) exceeds the benefit cap minus any amount included in the award for childcare costs. This ensures that childcarecosts are

CH2 NOTES - CHILD BENEFIT CLAIM FORM - GETTING IT RIGHT CH2 Notes Child Benefit claim form - Getting it right Use these notes to help you www.hmrc.gov.uk Our helpline number: 0845 302 1444 Ourtextphone number:

BEREAVEMENT « CHANGES OF CIRCUMSTANCES « HOW DO TAX Tax Credits: Bereavement. When a tax credit claimant dies, or a child who is included in a tax credit claim dies, this is a change of circumstances which must be notified to HMRC within 1 month. This has been temporarily extended to 3 months from 23rd May 2020 for critical workers due to the coronavirus pandemic. OVERPAYMENTS AND UNDERPAYMENTS « HOW DO TAX CREDITS WORK Tax Credits: Overpayments and underpayments . Overpayments and underpayments are a normal part of the tax credits system. This is because when a tax credits award is made it is not final until a final entitlement decision is made which is usually after the end of the tax year for which it has been given or shortly after a claim is ended during a tax year (where a person claims Universal Credit CAPITAL RULES « ENTITLEMENT TO UNIVERSAL CREDIT « GUIDANCE The maximum capital limit for claiming Universal Credit is £16,000 for either a single person or a couple where that capital is held jointly. If capital is above this amount there is no entitlement to UC. Capital or joint capital over £6,000 is treated as providing income, known as “tariff income”, of £4.35 per month for eachadditional

TC603RD NOTES

TC603RD Notes – for use from 6 April 2012 Renewing your tax credits – Getting it right Use these notes to help you Renew now– don’t risk leaving it until 31 July ELIGIBILITY CONDITIONS « WHO CAN CLAIM? « GUIDANCE « TAX Eligibility condition 1 - Age. The claimant must be aged at least 16 at the date of declaration. Eligibility condition 2 - Responsible for the child. The claimant must, at the date of declaration, be responsible for the relevant child. The relevant child means the child who the claimant is trying to open a childcare account for or, if theyare

WHERE IT ALL STARTED « POLICY « CHILD BENEFIT Child Poverty Action Group (CPAG) was instrumental in ‘changing their minds’ and in 1975 the child benefit bill was enacted. The bill replaced family allowance with a benefit for each child, which was paid to the mothers. The act was not implemented PENSIONERS « WHO CAN CLAIM UNIVERSAL CREDIT « GUIDANCE Currently, pension claimants are expected to claim help towards their housing costs through housing benefit. Capital. In pension credit, for each £500 of capital over £10,000, £1 is added to the person's income when calculating their entitlement. In UC, for each £250 of capital over £6,000, £4.35 a month is added to the person's income MANAGED MIGRATION « EXISTING TAX CREDIT CLAIMANTS Universal credit: Managed migration - Move to UC . This page explains the managed migration exercise - this is where DWP/HMRC move claimants from tax credits (and other legacy benefits) across to Universal Credit (UC) under a formal exercise, which is sometimes referred to as ‘Move to UC’ by DWP. BENEFIT CAP « ENTITLEMENT TO UNIVERSAL CREDIT « GUIDANCE The benefit cap is relevant to the final stage of calculating entitlement to UC. Firstly, the amount of excess must be calculated. This is the amount that the UC entitlement (plus any of the other benefits listed above) exceeds the benefit cap minus any amount included in the award for childcare costs. This ensures that childcarecosts are

CH2 NOTES - CHILD BENEFIT CLAIM FORM - GETTING IT RIGHT CH2 Notes Child Benefit claim form - Getting it right Use these notes to help you www.hmrc.gov.uk Our helpline number: 0845 302 1444 Ourtextphone number:

BEREAVEMENT « CHANGES OF CIRCUMSTANCES « HOW DO TAX Tax Credits: Bereavement. When a tax credit claimant dies, or a child who is included in a tax credit claim dies, this is a change of circumstances which must be notified to HMRC within 1 month. This has been temporarily extended to 3 months from 23rd May 2020 for critical workers due to the coronavirus pandemic. OVERPAYMENTS AND UNDERPAYMENTS « HOW DO TAX CREDITS WORK Tax Credits: Overpayments and underpayments . Overpayments and underpayments are a normal part of the tax credits system. This is because when a tax credits award is made it is not final until a final entitlement decision is made which is usually after the end of the tax year for which it has been given or shortly after a claim is ended during a tax year (where a person claims Universal Credit CAPITAL RULES « ENTITLEMENT TO UNIVERSAL CREDIT « GUIDANCE The maximum capital limit for claiming Universal Credit is £16,000 for either a single person or a couple where that capital is held jointly. If capital is above this amount there is no entitlement to UC. Capital or joint capital over £6,000 is treated as providing income, known as “tariff income”, of £4.35 per month for eachadditional

TC603RD NOTES

TC603RD Notes – for use from 6 April 2012 Renewing your tax credits – Getting it right Use these notes to help you Renew now– don’t risk leaving it until 31 JulyTAX CREDIT RENEWALS

4 June 2021 . Tax credit renewals – HMRC scams warning for tax credits customers . HMRC have issued the following message about scams JUNE, 2021 « BLOG « REVENUE BENEFITS Revenue benefits blog posts from June, 2021. 4 June 2021 | Tax credit renewals – HMRC scams warning for tax credits customersTAX CREDIT RENEWALS

9 September 2020 How are the NHS test and trace self-isolation payments treated for tax credits and universal credit? CHILD TRUST FUND (CTF) 27 March 2020 Coronavirus outbreak (Covid-19) – Tax credit and Universal Credit policy announcements WHERE IT ALL STARTED « POLICY « CHILD BENEFIT Child Poverty Action Group (CPAG) was instrumental in ‘changing their minds’ and in 1975 the child benefit bill was enacted. The bill replaced family allowance with a benefit for each child, which was paid to the mothers. The act was not implemented PENSION INCOME « WHAT IS INCOME « HOW DO TAX CREDITS WORK Pension income for tax credits mirrors the tax treatment. It includes the following taxable pension payments and annuities: income from UK social security pensions, ie the state retirement pension, graduated retirement benefit, industrial death benefit, widowed mother’s allowance, widowed parent’s allowance, and widow’s pension (ITEPA BENEFIT CAP « ENTITLEMENT TO UNIVERSAL CREDIT « GUIDANCE The benefit cap is relevant to the final stage of calculating entitlement to UC. Firstly, the amount of excess must be calculated. This is the amount that the UC entitlement (plus any of the other benefits listed above) exceeds the benefit cap minus any amount included in the award for childcare costs. This ensures that childcarecosts are

SURPLUS EARNINGS AND LOSSES « SELF-EMPLOYMENT Self-employment: Surplus earnings and losses . The surplus earnings and loss rules apply from April 2018. These are very complex rules and we have written this guidance to help advisers understand the rules. RTI AND UNIVERSAL CREDIT « ENTITLEMENT TO UNIVERSAL CREDIT In the past, HMRC required employers to send payments of tax and NI to them frequently and then report those figures after the end of each tax year on a series of forms. On 6 April 2013, HMRC introduced a new system of real time reporting for employers. It is often called the RTI (Real Time Information) system. CH2 NOTES - CHILD BENEFIT CLAIM FORM - GETTING IT RIGHT CH2 Notes Child Benefit claim form - Getting it right Use these notes to help you www.hmrc.gov.uk Our helpline number: 0845 302 1444 Ourtextphone number:

* ↓

* A

* A

Search: advanced search* Tax Credits

* Universal Credit

* National Minimum Wage* Child Benefit

* Tax-free childcare* Child Trust Fund

* Blog

NEW BLOG POSTS

* Universal Credit managed migration pilot * Tax credit renewals deadline 31 July 2019 * Universal Credit, tax credit and child benefit payments overEaster

* Managed migration pilot to launch in Harrogate * Free School Meals – WalesMore blog posts

APRIL UPDATING

We are currently updating revenuebenefits and adding new content to take account of the start of the 2019/2020 tax year. Keep checking back for the latest information.* _ _

* _ _

* _ _

* _ _

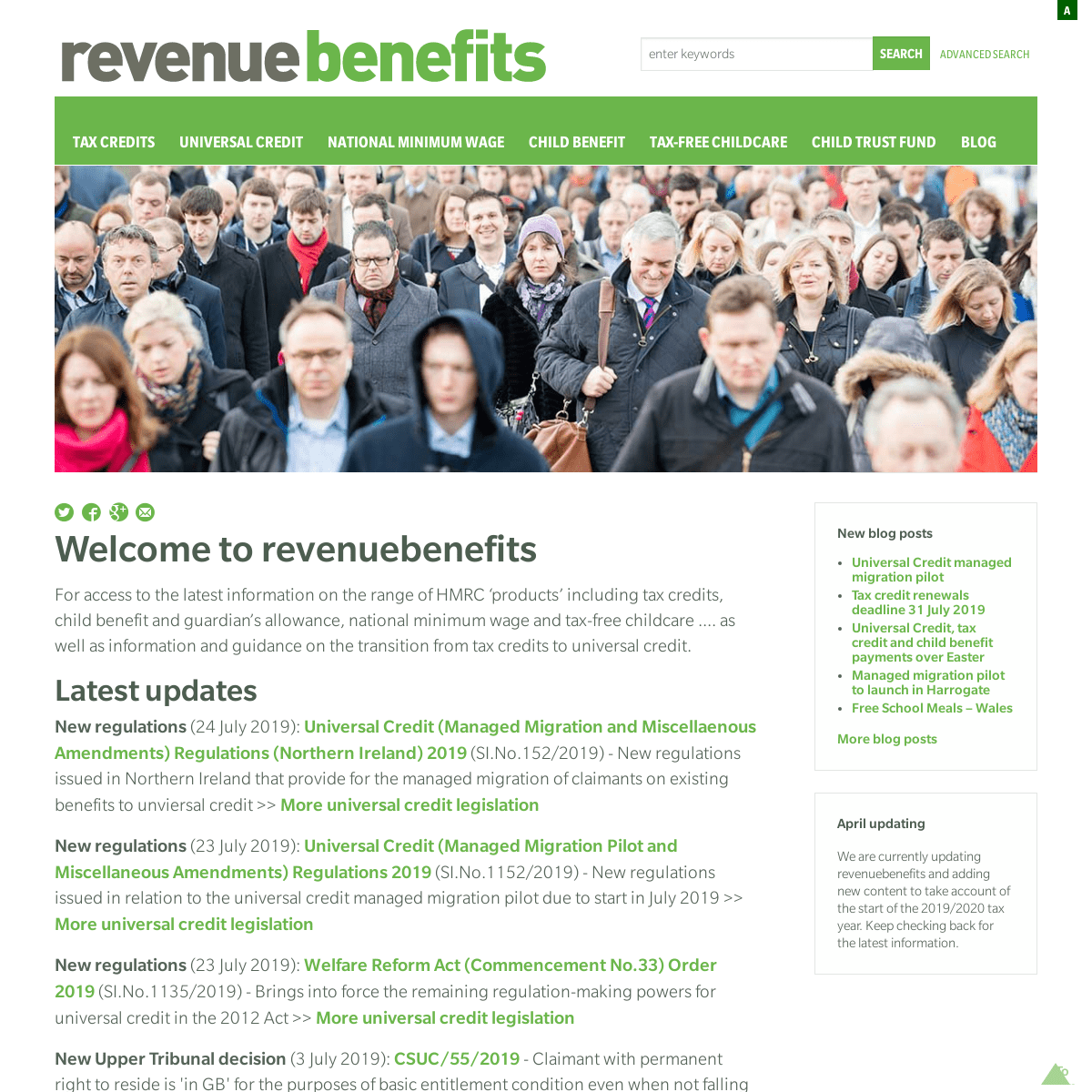

WELCOME TO REVENUEBENEFITS For access to the latest information on the range of HMRC ‘products’ including tax credits, child benefit and guardian’s allowance, national minimum wage and tax-free childcare .... as well as information and guidance on the transition from tax credits touniversal credit.

LATEST UPDATES

NEW REGULATIONS (24 July 2019): Universal Credit (Managed Migration and Miscellaenous Amendments) Regulations (Northern Ireland) 2019(SI.No.152/2019) -

New regulations issued in Northern Ireland that provide for the managed migration of claimants on existing benefits to unviersal credit >> More universal credit legislation NEW REGULATIONS (23 July 2019): Universal Credit (Managed Migration Pilot and Miscellaneous Amendments) Regulations 2019(SI.No.1152/2019)

- New regulations issued in relation to the universal credit managed migration pilot due to start in July 2019 >> More universal creditlegislation

NEW REGULATIONS (23 July 2019): Welfare Reform Act (CommencementNo.33) Order 2019

(SI.No.1135/2019)

- Brings into force the remaining regulation-making powers for universal credit in the 2012 Act >> More universal credit legislation NEW UPPER TRIBUNAL DECISION (3 July 2019): CSUC/55/2019 - Claimant with permanent right to reside is 'in GB' for the purposes of basic entitlement condition even when not falling within any of the situations in regulation 9(4) of the UC Regulations 2013 >> More universal credit case law NEW UPPER TRIBUNAL DECISION (2 May 2019): CTC/2349/2018 - Tax credits - Claim by married woman as a single person - Whether separated in circumstances such that separation seems likely to be permanent (TCA 2002 s.3(5A)(a)) - FTT direction addressed to claimant that husband attend as a witness - Adverse inference drawn when husband failed to attend - Importance of assessing evidence in its cultural context - Attitudes towards separation and divorce within a Muslim community where married couple are first cousins >> More taxcredit case law

NEW UPPER TRIBUNAL DECISION (30 April 2019): CSTC/283/2018 - Working tax credits - definition of "self-employed" in the Working Tax Credit (Entitlement and Maximum Rate) Regulations 2002 - relevance of profitability and "genuine and effective" in the test of carrying on a trade, profession or occupation "on a commercial basis" - circumstances in which the Upper Tribunal will hear an appeal against a decision of the First-tier Tribunal in a case which challenges a decision under Section 16 of the Tax Credits Act 2002 when a Section 18 decision has subsequently been issued >> More tax credit case law NEW REGULATIONS (16 April 2019): Child Benefit and Child Tax Credit (Amendment) (EU Exit) Regulations 2019(SI.No.867/2019) -

New regulations issued in relation to child benefit and child tax credit for those granted leave to enter or remain under the EU Settlement Scheme >> More tax credit legislation>> More child

benefit legislation

NEW UPPER TRIBUNAL DECISION (11 April 2019): CTC/1443/2018 - Whether a school has to be registered or approved in order for a person to be a qualifying young person >> More tax credit case law NEW UPPER TRIBUNAL DECISION (11 April 2019): CTC/2376/2017 - A decision taken by HMRC not to award a tax credit under section 14 of the Tax Credits Act 2002 cannot be followed by a final decision under section 18 of the 2002 Act. Therefore, no section 18 decision may cause an appeal to the First-tier Tribunal against such a decision to lapse. To the extent that a three-judge panel of the Upper Tribunal in LS & RS v HMRC AACR 2; UKUT 0247 (AAC) expressed the contrary view, its comments were obiter and should not be followed >> More tax credit case law NEW UPPER TRIBUNAL DECISION (8 March 2019): CTC/648/2018 - Payments made in settlement of employment tribunal case counted as earned income >> More tax credit case law NEW HIGH COURT JUDGMENT (4 March 2019): TD & Ors v The Secretary of State for Work and Pensions EWHC 462 (Admin) (1 March 2019)- High

Court rules that failure to provide transitional protection for claimants who transferred to universal credit following incorrect legacy benefit decision was not unlawful >> More universal credit caselaw

NEW REGULATIONS (27 February 2019): Tax Credits, Child Benefit and Childcare Payments (Miscellaneous Amendments) Regulations 2019(SI.No.364/2019) -

New regulations that make miscellaneous amendments to tax credits, child benefit and childcare payments >> More tax credit regulations| child

benefit regulations

| tax-free

childcare reglations NEW HIGH COURT JUDGMENT (14 February 2019): Awodiya & Anor v HM Revenue and Customs EWHC 251 (Admin) (12 February 2019)- High

Court refuses leave to appeal in a child tax credit case on the grounds that the claimants had not exhausted their alternative remedies and that it would be inappropriate to permit them to circumvent, through the mechanism of judicial review, the statutory procedures open to them >> More tax credit case law NEW REGULATIONS (6 February 2019): Free School Lunches and Milk (Universal Credit) (Wales) Order 2019 (SI.No.187/2019) - New regulations issued that amend the eligibility criteria for free school meals in Wales >> More universal creditlegislation

NEW REGULATIONS (1 February 2019): Welfare Reform Act 2012 (Commencement No.32 and Savings and Transitional Provisions) Order2019

(SI.No.167/2019) - New regulations issued in Great Britain in relation to the abolition of child tax credit and working tax credit from 1 February 2019. Equivalent changes made in Northern Ireland by the Welfare Reform (Northern Ireland) Order 2015 (Commencement No.14 and Savings and Transitional Provisions) Order 2019(SR.No.7/2019) >>

More tax credit legislation NEW REGULATIONS (15 January 2019): Universal Credit (Restriction on Amounts for Children and Qualifying Young Persons) (Transitional Provisions) (Amendment) Regulations (Northern Ireland) 2019 (SR.No.3/2019) - New regulations issued in Northern Ireland in relation to the two-child limit in universal credit >> More universal credit legislation NEW REGULATIONS (15 January 2019): Universal Credit (Transitional Provisions) (SDP Gateway) Amendment Regulations 2019(SI.No.10/2019) -

New regulations issued that introduce a gateway condition into universal credit preventing claimants with a severe disability premium in a legacy benefit from making a claim. Equivalent changes made in Northern Ireland by the Universal Credit (Transitional Provisions) (SDP Gateway) Amendment (Northern Ireland) Regulations 2019(SR.No.2/2019) >>

More universal credit legislation NEW HIGH COURT JUDGMENT (11 January 2019): R (on the application of Johnson and others) v Secretary of State for Work and Pensions EWHX 23 (Admin) (11 January 2019)- High Court

rules that DWP's method of assessing earned income under universal credit is unlawful >> More universal credit case law NEW REGULATIONS (11 January 2019): Universal Credit (Restriction on Amounts for Children and Qualifying Young Persons) (Transitional Provisions) Amendment Regulations 2019 (SI.No.27/2019) - New regulations that provide for amendments to the two-child limit in universal credit >> More universal creditlegislation

NEW REGULATIONS (7 January 2019): The Housing Benefit and Universal Credit Housing Costs (Executive Determinations) (Amendment) Regulations (Northern Ireland) 2018(SR.No.209/2018) -

Provides for an increase in local housing allowance rates in designated areas when calculating housing benefit and universal credit costs in 2019/2020 >> More about universal credit in Northern Ireland NEW UPPER TRIBUNAL DECISION (7 January 2019): CUC/50/2018 andCUC/51/2018

- The decision contains a comparison of the grounds for recovery of an overpayment in social security benefits generally and UC >> More universal credit case law NEW UPPER TRIBUNAL DECISION (7 January 2019): CTC/1276/2018 - A tax credits case that considers the transition from tax credits to UC and whether the decision to end a CTC claim by HMRC (following a stop notice from DWP) is correct when a claimant had made a claim for UC by mistake and never received an award >> More universal creditcase law

ABOUT REVENUEBENEFITS revenuebenefits is a partnership between the Low Incomes Tax ReformGroup and Lasa .

Find out more about revenuebenefits* Home

* About us

* Contact us

* Accessibility

* Sitemap

* RSS

Get revenuebenefits updates by email LEGAL NOTICE: The content on this site is subject to a disclaimerand a copyright

notice . Your

continued use of revenuebenefits indicates your consent to our use of cookies . Please readour privacy policy

, about the use

we make of the information you provide to us.Web design by MID

* To top

Details

1