4

More Annotations

6

6

Favourite Annotations

6

6

Text

INVESTMENT MOATS

about Pursuing Coast FI with $550,000 – 3 Years Later. CSOP Global Cloud Computing Technology Index ETF (3194.HK) Launches. Here’s what you need to know about the ETF. There is a new exchange-traded fund (ETF) that allows an investor to be exposed to some of the leading global cloud computing companies. The ETF, . OUR FREE ONLINE INVESTMENT STOCK PORTFOLIO TRACKING The stock portfolio tracker is a FREE Google Spreadsheet hosted at Google that can do the following: Track your stocks, shares or bonds by transaction. You can enter Buy, Sell, Stock Splits, Rights Issues (or Cash Calls), Cash Dividends, Stock Dividends, Gift Stocks. Show you each of your asset (stocks, bonds) realized returns, unrealized HUARONG DEBT DEBACLE NEARLY AFFECTED SOME BOND FUNDS AND Huarong Debt Debacle Nearly Affected Some Bond Funds and Cash Solutions. Lai Xiaomin was once dubbed the “God of Fortune”. Xiaomin used to control Huarong Asset Management or China Huarong, a state-owned asset management company in China. Used to because he doesn’t anymore. On Jan 2021, Xiaomin was executed, 24 days after hewas sentenced

HOW TO CONVERT CURRENCIES IN INTERACTIVE BROKERS If the above currency conversion sounds cheem to you, then here is the simple way. Go to your Interactive Brokers mobile app. Click the Convert Currency. You will be presented with a rather clean interface. You can start off with putting in how much of the currency you have or the currency you want. SINGAPORE SAVINGS BONDS SSB JUNE 2021 The 10-yr and 1-yr Singapore Savings Bonds Rate since the first issue in Oct 2015. The June 2021 ’s SSB bonds yield an interest rate of 1.61%/yr for the next 10 years. You can apply through ATM or Internet Banking via the three banks (UOB, OCBC, DBS) However, if you only hold the SSB bonds for 1 year, with 2 semi-annual payments, your KEPPEL PACIFIC OAK US REIT ANNOUNCES HEALTHY RENT Keppel Pacific Oak US REIT (KORE) still spots a pretty attractive dividend. They just announced their first quarter 2021 update and this update provides us a glimpse of their projected income available fordistribution. If we

YOUR PERSONAL CASH FLOW STATEMENT A personal cash flow statement can provide clarity in your life, and serves as a personal review whether you are managing your life well. It also provides you with an opportunity to re-allocate your cash flow to bring your money in alignment with your goals in life. STOCK PORTFOLIO TRACKER First make a copy of my existing version of spreadsheet. You can do this by going to File > Make a copy (don’t use the Share function on the top right side) When you click on the Portfolio History > Copy to.. Secondly, search for your existing Stock Portfolio Tracker and add this Portfolio History to it. Third, clear my data on the HOW WOULD YOUR FIRST $60,000 IN CPF COMPOUND OVER TIME Normally, your Ordinary Account (OA) earns 2.5% interest (not permanent) and your Special Account (SA) earns 4% interest (also not permanent). Before 55 years old, your first $60,000 earns 1% more, up to $20,000 from your OA. This means that if you have $20,000 in your OA, your OA earns 3.5% and the $40,000 in your SA earns 5%. SOLUTION TO YAHOO FINANCE DATA NOT REFRESHING IN GOOGLE A few readers who are currently using my FREE Stock Portfolio Tracker have emailed me that their spreadsheet have failed to get any prices from Yahoo Finance in the past two days (This was written on 11th Dec 2020). In this post, I would provide a fix. Whether it is permanent or not is another question altogether.INVESTMENT MOATS

about Pursuing Coast FI with $550,000 – 3 Years Later. CSOP Global Cloud Computing Technology Index ETF (3194.HK) Launches. Here’s what you need to know about the ETF. There is a new exchange-traded fund (ETF) that allows an investor to be exposed to some of the leading global cloud computing companies. The ETF, . OUR FREE ONLINE INVESTMENT STOCK PORTFOLIO TRACKING The stock portfolio tracker is a FREE Google Spreadsheet hosted at Google that can do the following: Track your stocks, shares or bonds by transaction. You can enter Buy, Sell, Stock Splits, Rights Issues (or Cash Calls), Cash Dividends, Stock Dividends, Gift Stocks. Show you each of your asset (stocks, bonds) realized returns, unrealized HUARONG DEBT DEBACLE NEARLY AFFECTED SOME BOND FUNDS AND Huarong Debt Debacle Nearly Affected Some Bond Funds and Cash Solutions. Lai Xiaomin was once dubbed the “God of Fortune”. Xiaomin used to control Huarong Asset Management or China Huarong, a state-owned asset management company in China. Used to because he doesn’t anymore. On Jan 2021, Xiaomin was executed, 24 days after hewas sentenced

HOW TO CONVERT CURRENCIES IN INTERACTIVE BROKERS If the above currency conversion sounds cheem to you, then here is the simple way. Go to your Interactive Brokers mobile app. Click the Convert Currency. You will be presented with a rather clean interface. You can start off with putting in how much of the currency you have or the currency you want. SINGAPORE SAVINGS BONDS SSB JUNE 2021 The 10-yr and 1-yr Singapore Savings Bonds Rate since the first issue in Oct 2015. The June 2021 ’s SSB bonds yield an interest rate of 1.61%/yr for the next 10 years. You can apply through ATM or Internet Banking via the three banks (UOB, OCBC, DBS) However, if you only hold the SSB bonds for 1 year, with 2 semi-annual payments, your KEPPEL PACIFIC OAK US REIT ANNOUNCES HEALTHY RENT Keppel Pacific Oak US REIT (KORE) still spots a pretty attractive dividend. They just announced their first quarter 2021 update and this update provides us a glimpse of their projected income available fordistribution. If we

YOUR PERSONAL CASH FLOW STATEMENT A personal cash flow statement can provide clarity in your life, and serves as a personal review whether you are managing your life well. It also provides you with an opportunity to re-allocate your cash flow to bring your money in alignment with your goals in life. STOCK PORTFOLIO TRACKER First make a copy of my existing version of spreadsheet. You can do this by going to File > Make a copy (don’t use the Share function on the top right side) When you click on the Portfolio History > Copy to.. Secondly, search for your existing Stock Portfolio Tracker and add this Portfolio History to it. Third, clear my data on the HOW WOULD YOUR FIRST $60,000 IN CPF COMPOUND OVER TIME Normally, your Ordinary Account (OA) earns 2.5% interest (not permanent) and your Special Account (SA) earns 4% interest (also not permanent). Before 55 years old, your first $60,000 earns 1% more, up to $20,000 from your OA. This means that if you have $20,000 in your OA, your OA earns 3.5% and the $40,000 in your SA earns 5%. SOLUTION TO YAHOO FINANCE DATA NOT REFRESHING IN GOOGLE A few readers who are currently using my FREE Stock Portfolio Tracker have emailed me that their spreadsheet have failed to get any prices from Yahoo Finance in the past two days (This was written on 11th Dec 2020). In this post, I would provide a fix. Whether it is permanent or not is another question altogether. CAN YOU BETTER TIME YOUR ANNUAL INVESTMENT BASE ON MARKET There is a popular saying that investors like to say “Sell in May and Go Away”. After a while, people infer that this means if you sell your portfolio in May and move to risk-free instruments, then come back in October or November, your results are better. Many wonder how true this is. There is I HAVE DOUBTS ABOUT STRAITS TIMES INVEST'S FINANCIAL 1 day ago · For a long time, many newspaper readers would look forward to SPH’s Sunday Times have an Invest Section. What is nice about the Sunday Times section is that it contains articles that are lighter, not so business-like, higher on the personal finance content. That is the content that is more OUR FREE ONLINE INVESTMENT STOCK PORTFOLIO TRACKING The stock portfolio tracker is a FREE Google Spreadsheet hosted at Google that can do the following: Track your stocks, shares or bonds by transaction. You can enter Buy, Sell, Stock Splits, Rights Issues (or Cash Calls), Cash Dividends, Stock Dividends, Gift Stocks. Show you each of your asset (stocks, bonds) realized returns, unrealized AN EASY STEP-BY-STEP GUIDE TO SETUP INTERACTIVE BROKERS The whole application approval was done online, my approval took 3 working days. So there were no trips to Asia Square Tower 1 or snail mail. In this post, I bring you through the whole process step-by-step. 1. Start Trading with Interactive Brokers by Opening an Account Application. HOW TO BUY AND SELL STOCKS ON INTERACTIVE BROKERS There is a Buy and Sell button at the bottom of the IWDA information screen. Click on the Buy button. You would need to fill in #1 the quantity, #2 the order type, #3 the price, #4 time-in-force. And then you will slide #5 to buy. Interactive Brokers by default set GROW YOUR WEALTH, RECEIVE RECURRING INCOME WITH MONEYOWL If the portfolio is left with $100, 4.5% gives you an income of $4.50 a year. You cannot do anything with $4.50, but your portfolio don’t run out of money. In Year 3, the income increase to $38,673 because the ending portfolio value in Year 2 is $859,401. After 13 THE 11 STAGES OF WEALTH: WHICH STAGE OF WEALTH ARE YOU AT The 11 stages let you identify the level of wealth you have attain. Each stage either. Gives you some level of psychological freedom. Your level of wealth provides certain level of immediate use. You should aim to level up to a further stage. The higher you go, the more useful your wealth would be. LEVERAGED YIELD OF RETURN FOR YOUR PROPERTY Property rental is a passive income dream for a lot of people, which is why you see many people flocking to condo launches these few years.. And the main attraction why property is better than bonds, equities or other asset class is that it is the easiest for average folks like you and me to leverage up.. Recently, the Singapore Government have been trying to stem this property speculation SEND MONEY FROM TRANSFERWISE TO INTERACTIVE BROKERS Unfortunately, other international banks may charge international investors an exorbitant fee to perform wire transfer to another country. TransferWise is an international payments company with a few payment services that you can use to reduce the cost of currency exchange:. Send money with money in one currency to another entity in another currency at an exchange rate more favorable than SHOULD YOU SURRENDER YOUR PRUFLEXICASH? The PRUFlexiCash Endowment Plan. In 2010, he bought the plan PRUFlexiCash and paid a premium of $73/mth ($876/yr). The tenure of this plan is 25 years. On top of this, he is paying $3.22/mth for a rider to supplement the main plan’s protection (which is against Death, Terminal Illness, Total Permanent Disability) PRUFlexiCash isan insurance

INVESTMENT MOATS

about Pursuing Coast FI with $550,000 – 3 Years Later. CSOP Global Cloud Computing Technology Index ETF (3194.HK) Launches. Here’s what you need to know about the ETF. There is a new exchange-traded fund (ETF) that allows an investor to be exposed to some of the leading global cloud computing companies. The ETF, . HOW TO CONVERT CURRENCIES IN INTERACTIVE BROKERS If the above currency conversion sounds cheem to you, then here is the simple way. Go to your Interactive Brokers mobile app. Click the Convert Currency. You will be presented with a rather clean interface. You can start off with putting in how much of the currency you have or the currency you want. THE 11 STAGES OF WEALTH: WHICH STAGE OF WEALTH ARE YOU AT The 11 stages let you identify the level of wealth you have attain. Each stage either. Gives you some level of psychological freedom. Your level of wealth provides certain level of immediate use. You should aim to level up to a further stage. The higher you go, the more useful your wealth would be. SINGAPORE SAVINGS BONDS SSB JUNE 2021 The 10-yr and 1-yr Singapore Savings Bonds Rate since the first issue in Oct 2015. The June 2021 ’s SSB bonds yield an interest rate of 1.61%/yr for the next 10 years. You can apply through ATM or Internet Banking via the three banks (UOB, OCBC, DBS) However, if you only hold the SSB bonds for 1 year, with 2 semi-annual payments, your STOCK PORTFOLIO TRACKER First make a copy of my existing version of spreadsheet. You can do this by going to File > Make a copy (don’t use the Share function on the top right side) When you click on the Portfolio History > Copy to.. Secondly, search for your existing Stock Portfolio Tracker and add this Portfolio History to it. Third, clear my data on the WHAT IS THE S$NEER? HOW MAS MANAGES SINGAPORE'S MONETARY Credit: Channel News Asia. This is a de facto SGD devaluation used when confronted with difficult economic challenges. “ Kyith: MAS decide to center the band downwards in April 2009 during the GFC to make our currency more competitive in global trade.They center the curve back in April 2010 when the situation looked better. SOLUTION TO YAHOO FINANCE DATA NOT REFRESHING IN GOOGLE A few readers who are currently using my FREE Stock Portfolio Tracker have emailed me that their spreadsheet have failed to get any prices from Yahoo Finance in the past two days (This was written on 11th Dec 2020). In this post, I would provide a fix. Whether it is permanent or not is another question altogether. HOW WOULD YOUR FIRST $60,000 IN CPF COMPOUND OVER TIME Normally, your Ordinary Account (OA) earns 2.5% interest (not permanent) and your Special Account (SA) earns 4% interest (also not permanent). Before 55 years old, your first $60,000 earns 1% more, up to $20,000 from your OA. This means that if you have $20,000 in your OA, your OA earns 3.5% and the $40,000 in your SA earns 5%. TOPPING UP YOUR CPF LIFE TO ENHANCED RETIREMENT SUM (ERS For example, the current 2020 FRS is $181,000. The couple born in 1960 would just be 60 years old. They can top-up his CPF Retirement Account to $181,000 or $271,500 if they wish to get a greater income stream. HYFLUX: I COULD PROBABLY SEE THE STRUCTURAL WEAKNESS BUT I notice that a lot of folks have put out various pieces on this, telling people you ought to see this coming. My feel about this is that, I did not pay attention to Hyflux and the related stuff but my friend have been computing the mathematics behind the CPSINVESTMENT MOATS

about Pursuing Coast FI with $550,000 – 3 Years Later. CSOP Global Cloud Computing Technology Index ETF (3194.HK) Launches. Here’s what you need to know about the ETF. There is a new exchange-traded fund (ETF) that allows an investor to be exposed to some of the leading global cloud computing companies. The ETF, . HOW TO CONVERT CURRENCIES IN INTERACTIVE BROKERS If the above currency conversion sounds cheem to you, then here is the simple way. Go to your Interactive Brokers mobile app. Click the Convert Currency. You will be presented with a rather clean interface. You can start off with putting in how much of the currency you have or the currency you want. THE 11 STAGES OF WEALTH: WHICH STAGE OF WEALTH ARE YOU AT The 11 stages let you identify the level of wealth you have attain. Each stage either. Gives you some level of psychological freedom. Your level of wealth provides certain level of immediate use. You should aim to level up to a further stage. The higher you go, the more useful your wealth would be. SINGAPORE SAVINGS BONDS SSB JUNE 2021 The 10-yr and 1-yr Singapore Savings Bonds Rate since the first issue in Oct 2015. The June 2021 ’s SSB bonds yield an interest rate of 1.61%/yr for the next 10 years. You can apply through ATM or Internet Banking via the three banks (UOB, OCBC, DBS) However, if you only hold the SSB bonds for 1 year, with 2 semi-annual payments, your STOCK PORTFOLIO TRACKER First make a copy of my existing version of spreadsheet. You can do this by going to File > Make a copy (don’t use the Share function on the top right side) When you click on the Portfolio History > Copy to.. Secondly, search for your existing Stock Portfolio Tracker and add this Portfolio History to it. Third, clear my data on the WHAT IS THE S$NEER? HOW MAS MANAGES SINGAPORE'S MONETARY Credit: Channel News Asia. This is a de facto SGD devaluation used when confronted with difficult economic challenges. “ Kyith: MAS decide to center the band downwards in April 2009 during the GFC to make our currency more competitive in global trade.They center the curve back in April 2010 when the situation looked better. SOLUTION TO YAHOO FINANCE DATA NOT REFRESHING IN GOOGLE A few readers who are currently using my FREE Stock Portfolio Tracker have emailed me that their spreadsheet have failed to get any prices from Yahoo Finance in the past two days (This was written on 11th Dec 2020). In this post, I would provide a fix. Whether it is permanent or not is another question altogether. HOW WOULD YOUR FIRST $60,000 IN CPF COMPOUND OVER TIME Normally, your Ordinary Account (OA) earns 2.5% interest (not permanent) and your Special Account (SA) earns 4% interest (also not permanent). Before 55 years old, your first $60,000 earns 1% more, up to $20,000 from your OA. This means that if you have $20,000 in your OA, your OA earns 3.5% and the $40,000 in your SA earns 5%. TOPPING UP YOUR CPF LIFE TO ENHANCED RETIREMENT SUM (ERS For example, the current 2020 FRS is $181,000. The couple born in 1960 would just be 60 years old. They can top-up his CPF Retirement Account to $181,000 or $271,500 if they wish to get a greater income stream. HYFLUX: I COULD PROBABLY SEE THE STRUCTURAL WEAKNESS BUT I notice that a lot of folks have put out various pieces on this, telling people you ought to see this coming. My feel about this is that, I did not pay attention to Hyflux and the related stuff but my friend have been computing the mathematics behind the CPS OUR FREE ONLINE INVESTMENT STOCK PORTFOLIO TRACKING The stock portfolio tracker is a FREE Google Spreadsheet hosted at Google that can do the following: Track your stocks, shares or bonds by transaction. You can enter Buy, Sell, Stock Splits, Rights Issues (or Cash Calls), Cash Dividends, Stock Dividends, Gift Stocks. Show you each of your asset (stocks, bonds) realized returns, unrealized HOW TO SAVE MONEY: DIVIDING UP YOUR SAVINGS AND How to divide up your savings. Here at Investment Moats, we have talked about budgeting using virtual envelopes. To divide your savings based on different objectives, create individual virtual envelopes for it. In the case of a person earning $4000, his take home pay after government forced savings will be $3200. KEPPEL PACIFIC OAK US REIT ANNOUNCES HEALTHY RENT Keppel Pacific Oak US REIT (KORE) still spots a pretty attractive dividend. They just announced their first quarter 2021 update and this update provides us a glimpse of their projected income available fordistribution. If we

THE 11 STAGES OF WEALTH: WHICH STAGE OF WEALTH ARE YOU AT The 11 stages let you identify the level of wealth you have attain. Each stage either. Gives you some level of psychological freedom. Your level of wealth provides certain level of immediate use. You should aim to level up to a further stage. The higher you go, the more useful your wealth would be. HOW TO FUND & WITHDRAW FUNDS FROM YOUR INTERACTIVE BROKERS Once you have setup your Interactive Brokers account through an entirely online sequence, you need to fund your account to start trading.. You can fund your Interactive Brokers account from banks and financial institutions from all over the globe. The transfer is free and you are entitled to one free withdrawal per calendar month. I willshow you how to

HUARONG DEBT DEBACLE NEARLY AFFECTED SOME BOND FUNDS AND Huarong Debt Debacle Nearly Affected Some Bond Funds and Cash Solutions. Lai Xiaomin was once dubbed the “God of Fortune”. Xiaomin used to control Huarong Asset Management or China Huarong, a state-owned asset management company in China. Used to because he doesn’t anymore. On Jan 2021, Xiaomin was executed, 24 days after hewas sentenced

YOUR PERSONAL CASH FLOW STATEMENT A personal cash flow statement can provide clarity in your life, and serves as a personal review whether you are managing your life well. It also provides you with an opportunity to re-allocate your cash flow to bring your money in alignment with your goals in life. TOPPING UP YOUR CPF LIFE TO ENHANCED RETIREMENT SUM (ERS For example, the current 2020 FRS is $181,000. The couple born in 1960 would just be 60 years old. They can top-up his CPF Retirement Account to $181,000 or $271,500 if they wish to get a greater income stream. HOW WELL DID STOCKS PERFORMED DURING HYPERINFLATION DURING There is a prevailing idea that to combat a very inflationary scenario, you will need a precious metal such as gold or commodities. In today’s discovery, I found a post that relates to how stocks did during the Weimar Republic in Germany when the country experience a SHOULD YOU SURRENDER YOUR PRUFLEXICASH? The PRUFlexiCash Endowment Plan. In 2010, he bought the plan PRUFlexiCash and paid a premium of $73/mth ($876/yr). The tenure of this plan is 25 years. On top of this, he is paying $3.22/mth for a rider to supplement the main plan’s protection (which is against Death, Terminal Illness, Total Permanent Disability) PRUFlexiCash isan insurance

INVESTMENT MOATS

Wealth Mentor for Financial Independence. Thoughtworthy was a YouTube channel that popped onto my social feed some time ago. FUTURE INSURANCE POLICY ILLUSTRATED INVESTMENT RATE TO BE Last week, we received an announcement that with effect from 1st July 2021, the policy illustrated investment rate (PIRR) will be lowered from 4.75% to 4.25% and 3.25% to 3.00% respectively. What is YourPolicy's

HOW TO CONVERT CURRENCIES IN INTERACTIVE BROKERS These are cost to you and if you are investing passively in a portfolio of low cost, diversified ETFs in UK or USA, cost matters. With IBKR, the usual currency spread I get is soooo low that it is almost like there isn’t a currency spread (as small as 0.1 PIP)..However, there is

HOW TO SAVE MONEY: DIVIDING UP YOUR SAVINGS AND Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing. HUARONG DEBT DEBACLE NEARLY AFFECTED SOME BOND FUNDS AND On Jan 2021, Xiaomin was executed, 24 days after he was sentenced to death for receiving bribes and committing bigamy. China Huarong was established in 1999 by the China government in response to the 1997 Asian Financial Crisis. WHAT IS THE S$NEER? HOW MAS MANAGES SINGAPORE'S MONETARY Credit: Channel News Asia. This is a de facto SGD devaluation used when confronted with difficult economic challenges. “ Kyith: MAS decide to center the band downwards in April 2009 during the GFC to make our currency more competitive in global trade.They center the curve back in April 2010 when the situation looked better. HOW WELL DID STOCKS PERFORMED DURING HYPERINFLATION DURING There is a prevailing idea that to combat a very inflationary scenario, you will need a precious metal such as gold or commodities. In today’s discovery, I found a post that relates to how stocks did during the Weimar Republic in Germany when the country experience a HOW WOULD YOUR FIRST $60,000 IN CPF COMPOUND OVER TIME If You Have $60,000 and Do Not Add on, How would this $60,000 Grow? So my reader was messing with the numbers to see if we hit this first $60,000, and we do not add on anymore to our CPF, how would this $60,000 grow?. Would it satisfy the minimum sum?. Firstly, I think its awesome if you are messing with the spreadsheet to see what numbers you come up with in your wealth building journey. WHY LIVING OFF DIVIDEND INCOME IN RETIREMENT IS NOT The real balance of the $1 million invested. The above chart shows the capital for all 66 30-year instances. You would realize that your capital value is never zero.However, there are some sequences wherein the end, the real value is less than the starting. WHAT IF YOU REPLACE SOME GOLD WITH REITS IN THE PERMANENTSEE MORE ONINVESTMENTMOATS.COM

INVESTMENT MOATS

Wealth Mentor for Financial Independence. Thoughtworthy was a YouTube channel that popped onto my social feed some time ago. FUTURE INSURANCE POLICY ILLUSTRATED INVESTMENT RATE TO BE Last week, we received an announcement that with effect from 1st July 2021, the policy illustrated investment rate (PIRR) will be lowered from 4.75% to 4.25% and 3.25% to 3.00% respectively. What is YourPolicy's

HOW TO CONVERT CURRENCIES IN INTERACTIVE BROKERS These are cost to you and if you are investing passively in a portfolio of low cost, diversified ETFs in UK or USA, cost matters. With IBKR, the usual currency spread I get is soooo low that it is almost like there isn’t a currency spread (as small as 0.1 PIP)..However, there is

HOW TO SAVE MONEY: DIVIDING UP YOUR SAVINGS AND Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing. HUARONG DEBT DEBACLE NEARLY AFFECTED SOME BOND FUNDS AND On Jan 2021, Xiaomin was executed, 24 days after he was sentenced to death for receiving bribes and committing bigamy. China Huarong was established in 1999 by the China government in response to the 1997 Asian Financial Crisis. WHAT IS THE S$NEER? HOW MAS MANAGES SINGAPORE'S MONETARY Credit: Channel News Asia. This is a de facto SGD devaluation used when confronted with difficult economic challenges. “ Kyith: MAS decide to center the band downwards in April 2009 during the GFC to make our currency more competitive in global trade.They center the curve back in April 2010 when the situation looked better. HOW WELL DID STOCKS PERFORMED DURING HYPERINFLATION DURING There is a prevailing idea that to combat a very inflationary scenario, you will need a precious metal such as gold or commodities. In today’s discovery, I found a post that relates to how stocks did during the Weimar Republic in Germany when the country experience a HOW WOULD YOUR FIRST $60,000 IN CPF COMPOUND OVER TIME If You Have $60,000 and Do Not Add on, How would this $60,000 Grow? So my reader was messing with the numbers to see if we hit this first $60,000, and we do not add on anymore to our CPF, how would this $60,000 grow?. Would it satisfy the minimum sum?. Firstly, I think its awesome if you are messing with the spreadsheet to see what numbers you come up with in your wealth building journey. WHY LIVING OFF DIVIDEND INCOME IN RETIREMENT IS NOT The real balance of the $1 million invested. The above chart shows the capital for all 66 30-year instances. You would realize that your capital value is never zero.However, there are some sequences wherein the end, the real value is less than the starting. WHAT IF YOU REPLACE SOME GOLD WITH REITS IN THE PERMANENTSEE MORE ONINVESTMENTMOATS.COM

STOCK PORTFOLIO TRACKER It is FREE and to use it, you can read the instructions here.. This stock portfolio tracker is suitable for you if: You are more of a buy and hold investor; Wants to track your portfolio based on transactions (buy, sell, dividend, bonus shares, rights issues, capital reductions) HUARONG DEBT DEBACLE NEARLY AFFECTED SOME BOND FUNDS AND On Jan 2021, Xiaomin was executed, 24 days after he was sentenced to death for receiving bribes and committing bigamy. China Huarong was established in 1999 by the China government in response to the 1997 Asian Financial Crisis. GETTING STARTED WITH REITS: WHERE TO FIND THE INFORMATION You can also find the symbol and quote here. For example Cache Log Trust’s symbol is K2LU. Starhill Global symbol is P40U. With this code and name of the stock, you can go to other platforms to find thehistorical prices.

AN EASY STEP-BY-STEP GUIDE TO SETUP INTERACTIVE BROKERS Here is a short list: Through IBKR, I can buy and sell stocks in a lot of markets.Much more than most brokers out there. (Currently, as a Singaporean, you cannot use IBKR to trade the stocks listed on SGX in Singapore but foreigners can. LEVERAGED YIELD OF RETURN FOR YOUR PROPERTY Property rental is a passive income dream for a lot of people, which is why you see many people flocking to condo launches these few years.. And the main attraction why property is better than bonds, equities or other asset class is that it is the easiest for average folks like you and me to leverage up.. Recently, the Singapore Government have been trying to stem this property speculation PORTFOLIO REBALANCING IN INDIVIDUAL STOCK INVESTING Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing. A GOOD EXPLANATION ON PARTICIPATING FUND Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing. YOUR PERSONAL CASH FLOW STATEMENT A personal cash flow statement can provide clarity in your life, and serves as a personal review whether you are managing your life well. It also provides you with an opportunity to re-allocate your cash flow to bring your money in alignment with your goals in life. WHY LIVING OFF DIVIDEND INCOME IN RETIREMENT IS NOT The real balance of the $1 million invested. The above chart shows the capital for all 66 30-year instances. You would realize that your capital value is never zero.However, there are some sequences wherein the end, the real value is less than the starting. SHOULD YOU SURRENDER YOUR PRUFLEXICASH? He was asking me whether should he continue the policy till maturity or surrender the policy.. The PRUFlexiCash Endowment Plan. In 2010, he bought the plan PRUFlexiCash and paid a premium of $73/mth ($876/yr).. The tenure of this plan is 25 years. On top of this, he is paying $3.22/mth for a rider to supplement the main plan’s protection (which is against Death, Terminal Illness, TotalINVESTMENT MOATS

about Pursuing Coast FI with $550,000 – 3 Years Later. CSOP Global Cloud Computing Technology Index ETF (3194.HK) Launches. Here’s what you need to know about the ETF. There is a new exchange-traded fund (ETF) that allows an investor to be exposed to some of the leading global cloud computing companies. The ETF, . FUTURE INSURANCE POLICY ILLUSTRATED INVESTMENT RATE TO BE Last week, we received an announcement that with effect from 1st July 2021, the policy illustrated investment rate (PIRR) will be lowered from 4.75% to 4.25% and 3.25% to 3.00% respectively. What is YourPolicy's

HOW TO CONVERT CURRENCIES IN INTERACTIVE BROKERS If the above currency conversion sounds cheem to you, then here is the simple way. Go to your Interactive Brokers mobile app. Click the Convert Currency. You will be presented with a rather clean interface. You can start off with putting in how much of the currency you have or the currency you want. SINGAPORE SAVINGS BONDS SSB JUNE 2021 The 10-yr and 1-yr Singapore Savings Bonds Rate since the first issue in Oct 2015. The June 2021 ’s SSB bonds yield an interest rate of 1.61%/yr for the next 10 years. You can apply through ATM or Internet Banking via the three banks (UOB, OCBC, DBS) However, if you only hold the SSB bonds for 1 year, with 2 semi-annual payments, your HOW WOULD YOUR FIRST $60,000 IN CPF COMPOUND OVER TIME Normally, your Ordinary Account (OA) earns 2.5% interest (not permanent) and your Special Account (SA) earns 4% interest (also not permanent). Before 55 years old, your first $60,000 earns 1% more, up to $20,000 from your OA. This means that if you have $20,000 in your OA, your OA earns 3.5% and the $40,000 in your SA earns 5%. WHAT IS THE S$NEER? HOW MAS MANAGES SINGAPORE'S MONETARY Credit: Channel News Asia. This is a de facto SGD devaluation used when confronted with difficult economic challenges. “ Kyith: MAS decide to center the band downwards in April 2009 during the GFC to make our currency more competitive in global trade.They center the curve back in April 2010 when the situation looked better. TOPPING UP YOUR CPF LIFE TO ENHANCED RETIREMENT SUM (ERS For example, the current 2020 FRS is $181,000. The couple born in 1960 would just be 60 years old. They can top-up his CPF Retirement Account to $181,000 or $271,500 if they wish to get a greater income stream. HOW WELL DID STOCKS PERFORMED DURING HYPERINFLATION DURING There is a prevailing idea that to combat a very inflationary scenario, you will need a precious metal such as gold or commodities. In today’s discovery, I found a post that relates to how stocks did during the Weimar Republic in Germany when the country experience a SHOULD YOU SURRENDER YOUR PRUFLEXICASH? The PRUFlexiCash Endowment Plan. In 2010, he bought the plan PRUFlexiCash and paid a premium of $73/mth ($876/yr). The tenure of this plan is 25 years. On top of this, he is paying $3.22/mth for a rider to supplement the main plan’s protection (which is against Death, Terminal Illness, Total Permanent Disability) PRUFlexiCash isan insurance

HYFLUX: I COULD PROBABLY SEE THE STRUCTURAL WEAKNESS BUT I notice that a lot of folks have put out various pieces on this, telling people you ought to see this coming. My feel about this is that, I did not pay attention to Hyflux and the related stuff but my friend have been computing the mathematics behind the CPSINVESTMENT MOATS

about Pursuing Coast FI with $550,000 – 3 Years Later. CSOP Global Cloud Computing Technology Index ETF (3194.HK) Launches. Here’s what you need to know about the ETF. There is a new exchange-traded fund (ETF) that allows an investor to be exposed to some of the leading global cloud computing companies. The ETF, . HOW TO CONVERT CURRENCIES IN INTERACTIVE BROKERS If the above currency conversion sounds cheem to you, then here is the simple way. Go to your Interactive Brokers mobile app. Click the Convert Currency. You will be presented with a rather clean interface. You can start off with putting in how much of the currency you have or the currency you want. THE 11 STAGES OF WEALTH: WHICH STAGE OF WEALTH ARE YOU AT The 11 stages let you identify the level of wealth you have attain. Each stage either. Gives you some level of psychological freedom. Your level of wealth provides certain level of immediate use. You should aim to level up to a further stage. The higher you go, the more useful your wealth would be. SINGAPORE SAVINGS BONDS SSB JUNE 2021 The 10-yr and 1-yr Singapore Savings Bonds Rate since the first issue in Oct 2015. The June 2021 ’s SSB bonds yield an interest rate of 1.61%/yr for the next 10 years. You can apply through ATM or Internet Banking via the three banks (UOB, OCBC, DBS) However, if you only hold the SSB bonds for 1 year, with 2 semi-annual payments, your WHAT IS THE S$NEER? HOW MAS MANAGES SINGAPORE'S MONETARY Credit: Channel News Asia. This is a de facto SGD devaluation used when confronted with difficult economic challenges. “ Kyith: MAS decide to center the band downwards in April 2009 during the GFC to make our currency more competitive in global trade.They center the curve back in April 2010 when the situation looked better. STOCK PORTFOLIO TRACKER First make a copy of my existing version of spreadsheet. You can do this by going to File > Make a copy (don’t use the Share function on the top right side) When you click on the Portfolio History > Copy to.. Secondly, search for your existing Stock Portfolio Tracker and add this Portfolio History to it. Third, clear my data on the SOLUTION TO YAHOO FINANCE DATA NOT REFRESHING IN GOOGLE A few readers who are currently using my FREE Stock Portfolio Tracker have emailed me that their spreadsheet have failed to get any prices from Yahoo Finance in the past two days (This was written on 11th Dec 2020). In this post, I would provide a fix. Whether it is permanent or not is another question altogether. HOW WOULD YOUR FIRST $60,000 IN CPF COMPOUND OVER TIME Normally, your Ordinary Account (OA) earns 2.5% interest (not permanent) and your Special Account (SA) earns 4% interest (also not permanent). Before 55 years old, your first $60,000 earns 1% more, up to $20,000 from your OA. This means that if you have $20,000 in your OA, your OA earns 3.5% and the $40,000 in your SA earns 5%. TOPPING UP YOUR CPF LIFE TO ENHANCED RETIREMENT SUM (ERS For example, the current 2020 FRS is $181,000. The couple born in 1960 would just be 60 years old. They can top-up his CPF Retirement Account to $181,000 or $271,500 if they wish to get a greater income stream. HYFLUX: I COULD PROBABLY SEE THE STRUCTURAL WEAKNESS BUT I notice that a lot of folks have put out various pieces on this, telling people you ought to see this coming. My feel about this is that, I did not pay attention to Hyflux and the related stuff but my friend have been computing the mathematics behind the CPS HOW TO SAVE MONEY: DIVIDING UP YOUR SAVINGS AND How to divide up your savings. Here at Investment Moats, we have talked about budgeting using virtual envelopes. To divide your savings based on different objectives, create individual virtual envelopes for it. In the case of a person earning $4000, his take home pay after government forced savings will be $3200. HUARONG DEBT DEBACLE NEARLY AFFECTED SOME BOND FUNDS AND Huarong Debt Debacle Nearly Affected Some Bond Funds and Cash Solutions. Lai Xiaomin was once dubbed the “God of Fortune”. Xiaomin used to control Huarong Asset Management or China Huarong, a state-owned asset management company in China. Used to because he doesn’t anymore. On Jan 2021, Xiaomin was executed, 24 days after hewas sentenced

YOUR PERSONAL CASH FLOW STATEMENT A personal cash flow statement can provide clarity in your life, and serves as a personal review whether you are managing your life well. It also provides you with an opportunity to re-allocate your cash flow to bring your money in alignment with your goals in life. HOW WELL DID STOCKS PERFORMED DURING HYPERINFLATION DURING There is a prevailing idea that to combat a very inflationary scenario, you will need a precious metal such as gold or commodities. In today’s discovery, I found a post that relates to how stocks did during the Weimar Republic in Germany when the country experience a LEVERAGED YIELD OF RETURN FOR YOUR PROPERTY Property rental is a passive income dream for a lot of people, which is why you see many people flocking to condo launches these few years.. And the main attraction why property is better than bonds, equities or other asset class is that it is the easiest for average folks like you and me to leverage up.. Recently, the Singapore Government have been trying to stem this property speculation WHY LIVING OFF DIVIDEND INCOME IN RETIREMENT IS NOT There are some months you spend $4716 a month, some months $1754 a month and a lot of month $2972 a month. Of course, in the median, you end up spending more, but nevertheless there is volatility in the income. A median income of $2972 a month in the worst case is about $36,000 a year which is almost a 3.6% yield. THE AFFLUENT OF SINGAPORE: RICH BUT NOT RICH ENOUGH The difference is that this group may not have the income. If you look at the salary gauge of Singapore, this report seems to be talking about individuals. The emerging affluent are the people that have an income that ranges from SGD5000 to 10631. These should be above the 50 decile to 80 decile of Singapore individual income. 2 NEW ETFS HELPING SINGAPOREANS GAIN DIVERSIFIED GLOBAL If you are invested in IWDA, you would have gained 17.37% this year to date (from 1 Jan to 30th Aug or 8 months). DFA Global Core Equity clocks in at 13.41% and World Equity fund clocks in at 10.47%. The MSCI World Small Cap ETF (WDSC) did rather well at 12.83% but the Emerging Market ETF returned only 3.30%. SOLUTION TO YAHOO FINANCE DATA NOT REFRESHING IN GOOGLE A few readers who are currently using my FREE Stock Portfolio Tracker have emailed me that their spreadsheet have failed to get any prices from Yahoo Finance in the past two days (This was written on 11th Dec 2020). In this post, I would provide a fix. Whether it is permanent or not is another question altogether. HOW TO GET MY DECEASED FAMILY MEMBER'S MONEY OUT? (IF THE About 1 year ago, my mom passed away. There are some things I learn with the experience of someone that close leaving us, but that is a topic for another day. However, there are some administrative thingsINVESTMENT MOATS

about Pursuing Coast FI with $550,000 – 3 Years Later. CSOP Global Cloud Computing Technology Index ETF (3194.HK) Launches. Here’s what you need to know about the ETF. There is a new exchange-traded fund (ETF) that allows an investor to be exposed to some of the leading global cloud computing companies. The ETF, . HUARONG DEBT DEBACLE NEARLY AFFECTED SOME BOND FUNDS AND Huarong Debt Debacle Nearly Affected Some Bond Funds and Cash Solutions. Lai Xiaomin was once dubbed the “God of Fortune”. Xiaomin used to control Huarong Asset Management or China Huarong, a state-owned asset management company in China. Used to because he doesn’t anymore. On Jan 2021, Xiaomin was executed, 24 days after hewas sentenced

HOW TO CONVERT CURRENCIES IN INTERACTIVE BROKERS If the above currency conversion sounds cheem to you, then here is the simple way. Go to your Interactive Brokers mobile app. Click the Convert Currency. You will be presented with a rather clean interface. You can start off with putting in how much of the currency you have or the currency you want. HOW TO FUND & WITHDRAW FUNDS FROM YOUR INTERACTIVE BROKERS Once you have setup your Interactive Brokers account through an entirely online sequence, you need to fund your account to start trading.. You can fund your Interactive Brokers account from banks and financial institutions from all over the globe. The transfer is free and you are entitled to one free withdrawal per calendar month. I willshow you how to

AN EASY STEP-BY-STEP GUIDE TO SETUP INTERACTIVE BROKERS So there were no trips to Asia Square Tower 1 or snail mail. In this post, I bring you through the whole process step-by-step. 1. Start Trading with Interactive Brokers by Opening an Account Application. You start the process by clicking on the Open Application button. GETTING STARTED WITH REITS: WHERE TO FIND THE INFORMATION You can also find the symbol and quote here. For example Cache Log Trust’s symbol is K2LU. Starhill Global symbol is P40U. With this code and name of the stock, you can go to other platforms to find thehistorical prices.

HOW WOULD YOUR FIRST $60,000 IN CPF COMPOUND OVER TIMECPF CALCULATION TABLECPF CALCULATOR CPF CONTRIBUTIONCPF CALCULATOR SGCPF FIRST PAGECPF LIFE CALCULATOREMPLOYER CPF CONTRIBUTION CALCULATOR Before 55 years old, your first $60,000 earns 1% more, up to $20,000 from your OA. This means that if you have $20,000 in your OA, your OA earns 3.5% and the $40,000 in your SA earns 5%. You can transfer your money from your OA to your SA, to earn a higher interest rate. This transfer is irreversible, so do think carefully if you were to dothat.

WHAT IS THE S$NEER? HOW MAS MANAGES SINGAPORE'S MONETARY Credit: Channel News Asia. This is a de facto SGD devaluation used when confronted with difficult economic challenges. “ Kyith: MAS decide to center the band downwards in April 2009 during the GFC to make our currency more competitive in global trade.They center the curve back in April 2010 when the situation looked better. HOW WELL DID STOCKS PERFORMED DURING HYPERINFLATION DURING There is a prevailing idea that to combat a very inflationary scenario, you will need a precious metal such as gold or commodities. In today’s discovery, I found a post that relates to how stocks did during the Weimar Republic in Germany when the country experience a WHY LIVING OFF DIVIDEND INCOME IN RETIREMENT IS NOT401K DIVIDEND INCOMEBEST RETIREMENT DIVIDEND INCOME FUNDSDIVIDEND ONLY RETIREMENTRETIREMENT STRATEGIES DIVIDEND INCOMEBEST DIVIDENDS FORRETIREMENT INCOME

There are some months you spend $4716 a month, some months $1754 a month and a lot of month $2972 a month. Of course, in the median, you end up spending more, but nevertheless there is volatility in the income. A median income of $2972 a month in the worst case is about $36,000 a year which is almost a 3.6% yield.INVESTMENT MOATS

about Pursuing Coast FI with $550,000 – 3 Years Later. CSOP Global Cloud Computing Technology Index ETF (3194.HK) Launches. Here’s what you need to know about the ETF. There is a new exchange-traded fund (ETF) that allows an investor to be exposed to some of the leading global cloud computing companies. The ETF, . HUARONG DEBT DEBACLE NEARLY AFFECTED SOME BOND FUNDS AND Huarong Debt Debacle Nearly Affected Some Bond Funds and Cash Solutions. Lai Xiaomin was once dubbed the “God of Fortune”. Xiaomin used to control Huarong Asset Management or China Huarong, a state-owned asset management company in China. Used to because he doesn’t anymore. On Jan 2021, Xiaomin was executed, 24 days after hewas sentenced

HOW TO CONVERT CURRENCIES IN INTERACTIVE BROKERS If the above currency conversion sounds cheem to you, then here is the simple way. Go to your Interactive Brokers mobile app. Click the Convert Currency. You will be presented with a rather clean interface. You can start off with putting in how much of the currency you have or the currency you want. HOW TO FUND & WITHDRAW FUNDS FROM YOUR INTERACTIVE BROKERS Once you have setup your Interactive Brokers account through an entirely online sequence, you need to fund your account to start trading.. You can fund your Interactive Brokers account from banks and financial institutions from all over the globe. The transfer is free and you are entitled to one free withdrawal per calendar month. I willshow you how to

AN EASY STEP-BY-STEP GUIDE TO SETUP INTERACTIVE BROKERS So there were no trips to Asia Square Tower 1 or snail mail. In this post, I bring you through the whole process step-by-step. 1. Start Trading with Interactive Brokers by Opening an Account Application. You start the process by clicking on the Open Application button. GETTING STARTED WITH REITS: WHERE TO FIND THE INFORMATION You can also find the symbol and quote here. For example Cache Log Trust’s symbol is K2LU. Starhill Global symbol is P40U. With this code and name of the stock, you can go to other platforms to find thehistorical prices.

HOW WOULD YOUR FIRST $60,000 IN CPF COMPOUND OVER TIMECPF CALCULATION TABLECPF CALCULATOR CPF CONTRIBUTIONCPF CALCULATOR SGCPF FIRST PAGECPF LIFE CALCULATOREMPLOYER CPF CONTRIBUTION CALCULATOR Before 55 years old, your first $60,000 earns 1% more, up to $20,000 from your OA. This means that if you have $20,000 in your OA, your OA earns 3.5% and the $40,000 in your SA earns 5%. You can transfer your money from your OA to your SA, to earn a higher interest rate. This transfer is irreversible, so do think carefully if you were to dothat.

WHAT IS THE S$NEER? HOW MAS MANAGES SINGAPORE'S MONETARY Credit: Channel News Asia. This is a de facto SGD devaluation used when confronted with difficult economic challenges. “ Kyith: MAS decide to center the band downwards in April 2009 during the GFC to make our currency more competitive in global trade.They center the curve back in April 2010 when the situation looked better. HOW WELL DID STOCKS PERFORMED DURING HYPERINFLATION DURING There is a prevailing idea that to combat a very inflationary scenario, you will need a precious metal such as gold or commodities. In today’s discovery, I found a post that relates to how stocks did during the Weimar Republic in Germany when the country experience a WHY LIVING OFF DIVIDEND INCOME IN RETIREMENT IS NOT401K DIVIDEND INCOMEBEST RETIREMENT DIVIDEND INCOME FUNDSDIVIDEND ONLY RETIREMENTRETIREMENT STRATEGIES DIVIDEND INCOMEBEST DIVIDENDS FORRETIREMENT INCOME

There are some months you spend $4716 a month, some months $1754 a month and a lot of month $2972 a month. Of course, in the median, you end up spending more, but nevertheless there is volatility in the income. A median income of $2972 a month in the worst case is about $36,000 a year which is almost a 3.6% yield. TAKING A DEEPER LOOK AT ISHARES EDGE MSCI WORLD MOMENTUM In my introductory post on factor investing, one of the more popular factors is the momentum factor. The momentum factor, is rather controversial. On the surface, the economic drivers behind the momentum style are not clear. It makes little sense to HOW TO TRANSFER YOUR SHARES FROM STANDARD CHARTERED ONLINE Many investors wish to build their wealth through investing in a diversified portfolio of low-cost exchange-traded funds (ETFs). One of the key criteria is to use a platform that allows them to optimize their overall costs and keep that cost low. Roughly how AN EASY STEP-BY-STEP GUIDE TO SETUP INTERACTIVE BROKERS So there were no trips to Asia Square Tower 1 or snail mail. In this post, I bring you through the whole process step-by-step. 1. Start Trading with Interactive Brokers by Opening an Account Application. You start the process by clicking on the Open Application button. HOW TO BUY AND SELL STOCKS ON INTERACTIVE BROKERS There is a Buy and Sell button at the bottom of the IWDA information screen. Click on the Buy button. You would need to fill in #1 the quantity, #2 the order type, #3 the price, #4 time-in-force. And then you will slide #5 to buy. Interactive Brokers by default set YOUR PERSONAL CASH FLOW STATEMENT A personal cash flow statement can provide clarity in your life, and serves as a personal review whether you are managing your life well. It also provides you with an opportunity to re-allocate your cash flow to bring your money in alignment with your goals in life. IS DIVIDEND WITHHOLDING TAX IMPORTANT IN INVESTING The Domicile of the Company Determines the Dividend Withholding Tax Rate. Not Where the Company is Listed. Same for Unit Trust and ETF. One thing that bamboozled a lot of investor is that they think that all the stocks listed in the United States are automatically subjected to a 30% withholding tax (which is the withholding tax for United States). The way to remember is where the company is UPDATES TO THE FREE GOOGLE STOCK PORTFOLIO TRACKER 2. Update and Propagate Yahoo Price with new Function. Once you have saved the script, and click Run, you will be able to use the functions. Go to Stock Summary. At the first cell below the header, or cell G2, titled Yahoo Price, change the formula WHY LIVING OFF DIVIDEND INCOME IN RETIREMENT IS NOT There are some months you spend $4716 a month, some months $1754 a month and a lot of month $2972 a month. Of course, in the median, you end up spending more, but nevertheless there is volatility in the income. A median income of $2972 a month in the worst case is about $36,000 a year which is almost a 3.6% yield. EXPLAINING SEQUENCE OF RETURN RISK AND POSSIBLE SOLUTIONS In terms of the geometric sequence of returns, they don’t matter that much. Consider that A and B have $1 at the start. For the next 5 years A’s geometric return profile is as follows: A’s $1 at the end of the 5 years is: $1 x 1.1 x 1.3 x 0.5 x 1.4 x 1.05 = $1.051. B’s $1 at the end of the 5 years is: $1 x 0.5 x 1.1 x 1.05 x 1.3 x1.4

TOPPING UP YOUR CPF LIFE TO ENHANCED RETIREMENT SUM (ERS For example, the current 2020 FRS is $181,000. The couple born in 1960 would just be 60 years old. They can top-up his CPF Retirement Account to $181,000 or $271,500 if they wish to get a greater income stream. Consumer Privacy Information We and our advertising partners collect personal information (such as the cookies stored on your browser, the advertising identifier on your mobile device, or the IP address of your device) when you visit our site. We, and our partners, use this information to tailor and deliver ads to you on our site, or to help tailor ads to you when you visit others' sites. To tailor ads that may be more relevant to you, we and/or our partners may share the information we collect with thirdparties.

To learn more about the information we collect and use for advertising purposes, please see our Privacy Policy. If you do not

wish for us or our partners to sell your personal information to third parties for advertising purposes, select the applicable control from the "Do Not Sell My Personal Information" link provided. Note that although we will not sell your personal information after you click that button, we will continue to share some personal information with our partners (who will function as our service providers in such instance) to help us perform advertising-related functions such as, but not limited to, measuring the effectiveness of our ads, managing how many times you may see an ad, reporting on the performance of our ads, ensuring services are working correctly and securely, providing aggregate statistics and analytics, improving when and where you may see ads and/or reducing ad fraud. If you access this site from other devices or browsers, visit the link below from those devices or browsers to ensure your choice applies to the data collected when you use those devices or browsers. Additionally, although clicking the "Do Not Sell My Personal Information" link will opt you out of the sale of your personal information for advertising purposes, it will not opt you out of the use of previously collected and sold personal information (except for personal information sold within 90 days prior to your exercising your right to opt out) or all interest-based advertising. If you would like more information about how to opt out of interest-based advertising in desktop and mobile browsers on a particular device, please visit http://optout.aboutads.info/#/ and http://optout.networkadvertising.org/#. You may download the AppChoices app at http://www.aboutads.info/appchoices to opt out in connection with mobile apps, or use the platform controls on your mobile device to opt out.undefined

Do Not Sell My Personal InformationI Understand

Do not sell my personal informationINVESTMENT MOATS

* Home

* High Yield Dividend Stocks * My Current Portfolio* About

* Advertise / Hire Me* My Guides

* Build Wealth Foundation* Active Investing

* REITs Investing

* Redesigning Your Life * Retirement Planning* FREE Calculators

* Dividend Stock Tracker * Stock Portfolio Tracker * Cost of Car Ownership Online Calculator * Wealthy Calculator * Property Investment Calculator SINGAPORE SAVINGS BONDS SSB JULY 2020 ISSUE YIELDS 0.80% FOR 10 YEAR AND 0.30% FOR 1 YEAR June 2, 2020 by KyithLeave a Comment

_Here is a SAFE way to save your money that you have NO IDEA WHEN YOU WILL NEED to use it, or your EMERGENCY FUND._The

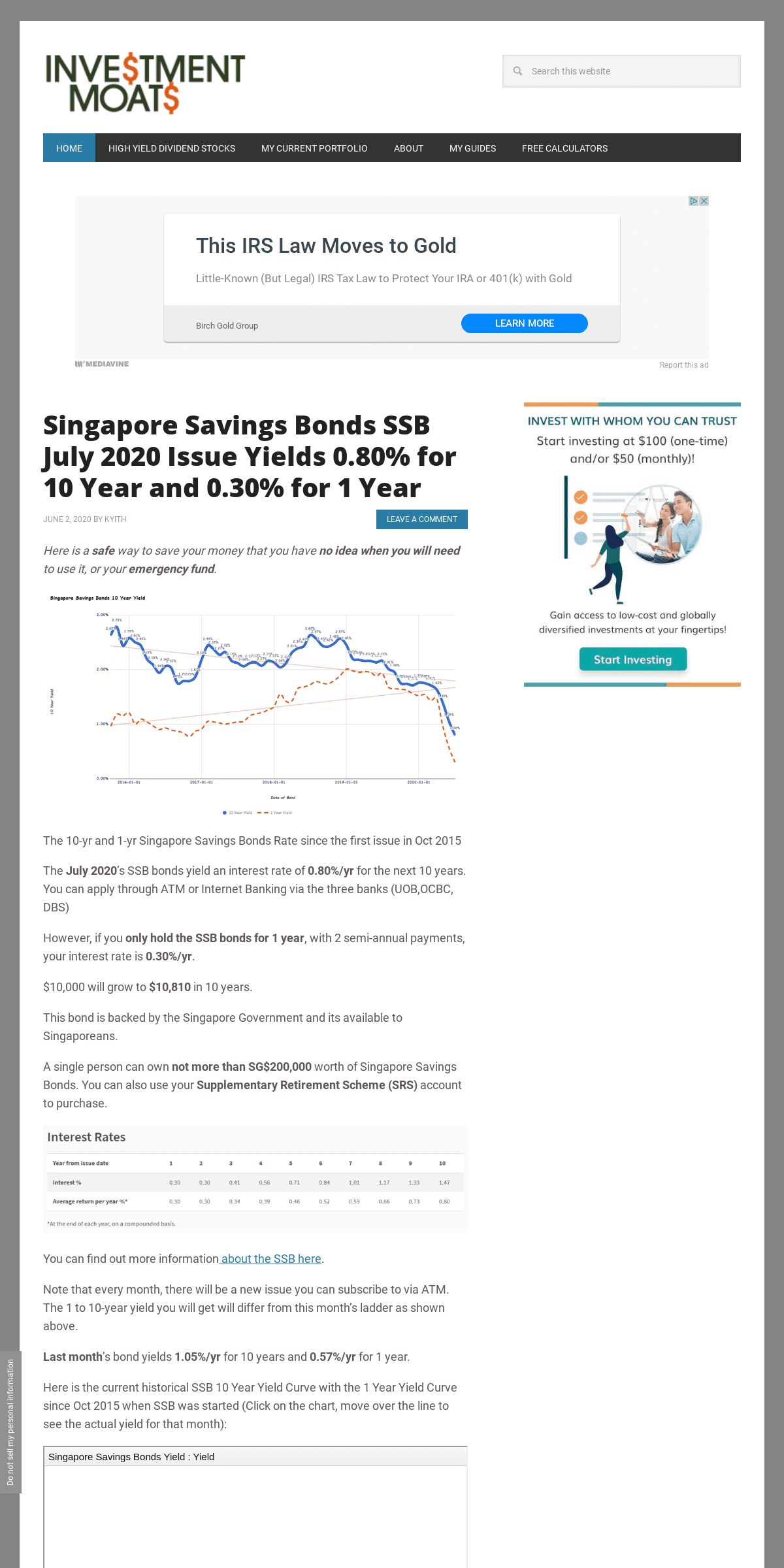

10-yr and 1-yr Singapore Savings Bonds Rate since the first issue inOct 2015

The JULY 2020’s SSB bonds yield an interest rate of 0.80%/YR for the next 10 years. You can apply through ATM or Internet Banking via the three banks (UOB,OCBC, DBS) However, if you ONLY HOLD THE SSB BONDS FOR 1 YEAR, with 2 semi-annual payments, your interest rate is 0.30%/YR. $10,000 will grow to $10,810 in 10 years. This bond is backed by the Singapore Government and its available toSingaporeans.

A single person can own NOT MORE THAN SG$200,000 worth of Singapore Savings Bonds. You can also use your SUPPLEMENTARY RETIREMENT SCHEME (SRS) account to purchase. You can find out more information about the SSB here.

Note that every month, there will be a new issue you can subscribe to via ATM. The 1 to 10-year yield you will get will differ from this month’s ladder as shown above. LAST MONTH’s bond yields 1.05%/YR for 10 years and 0.57%/YR for 1year.

Here is the current historical SSB 10 Year Yield Curve with the 1 Year Yield Curve since Oct 2015 when SSB was started (Click on the chart, move over the line to see the actual yield for that month): THE APPLICATION AND REDEMPTION SCHEDULE You will apply for the bonds through the month. At the end of the month, you will know how much of the bond you applied was successful. Here is the schedule for application and redemption if you wish tosell:

Click

to see larger schedule You have 02 to about 25th of the month (technically the 4th day from the last working day of the month) to apply or decide to redeem the SSB that you wish to redeem. Your bond will be in your CDP on the 1st of the next month. You will see your cash in your bank account linked to your CDP account on the1st of next month.

HOW DOES THE SINGAPORE SAVINGS BONDS COMPARE VERSUS SGS BONDS VERSUS SINGAPORE TREASURY BILLS? Singapore savings bonds is like a “unit trust” or a “fund” ofSGS Bonds.

But what is the difference between you buying SGS Bonds and its sister the T-Bills directly? BOTH THE SGS BONDS AND T-BILLS ARE ALSO ISSUED BY THE GOVERNMENT ANDARE AAA RATED.

Here is an MAS detailed comparison of the three:Click

to see bigger comparison table What is this Singapore Savings Bonds? Read my past write-ups: * This Singapore Savings Bonds: Liquidity, Higher Returns and Government Backing. Dream? * More details of the Singapore Savings Bond. Looks like my EmergencyFunds now

* Singapore Savings Bonds Max Holding Limit is $200,000 for now. Apply via DBS, OCBC, UOB ATM * Singapore Savings Bonds’ Inflation Protection Abilities * Some instructions on how to apply for the Singapore Savings Bonds Past Issues of SSB and their Rates:* 2015 Oct

* 2015 Nov

* 2015 Dec

* 2016 Jan

* 2016 Feb

* 2016 Mar

* 2016 Apr

* 2016 May

* 2016 Jun

* 2016 Jul

* 2016 Aug

* 2016 Sep

* 2016 Oct

* 2016 Nov

* 2016 Dec

* 2017 Jan

* 2017 Feb

* 2017 Mar

* 2017 Apr

* 2017 May

* 2017 Jun

* 2017 Jul

* 2017 Aug

* 2017 Sep

* 2017 Oct

* 2017 Nov

* 2018 Jan

* 2018 Feb

* 2018 Mar

* 2018 Apr

* 2018 May

* 2018 Jun

* 2018 Jul

* 2018 Aug

* 2018 Sep

* 2018 Oct

* 2018 Nov

* 2018 Dec

* 2019 Jan

* 2019 Feb

* 2019 Mar

* 2019 Apr

* 2019 May

* 2019 Jun

* 2019 Jul

* 2019 Aug

* 2019 Sep

* 2019 Oct

* 2019 Nov

* 2019 Dec

* 2020 Jan

* 2020 Feb

* 2020 Mar

* 2020 Apr

* 2020 May

* 2020 Jun

Do LIKE ME  on FACEBOOK. I share some tidbits that is not on the blog post there often. You can also choose to subscribe to my content via EMAIL BELOW. I break down my resources according to these topics: * Building Your Wealth Foundation– If you know and

apply these simple financial concepts, your long term wealth should be pretty well managed. Find out what they are* Active Investing

– For the active

stock investors. My deeper thoughts from my stock investing experience * Learning about REITs– My Free

“Course” on REIT Investing for Beginners and Seasoned Investors * Dividend Stock Tracker – Track all the common 4-10% yielding dividend stocks in SG * Free Stock Portfolio Tracking Google Sheets that many love * Retirement Planning, Financial Independence and Spending down money–

My deep dive into how much you need to achieve these, and the different ways you can be financially free* Providend

– Where

I work doing research. Fee-Only Advisory. No Commissions. Financial Independence Advisers and Retirement Specialists. No charge for the first meeting to understand how it works Filed Under: Saving and Investing My Money A WEDDING PHOTOGRAPHER PURSUES FINANCIAL INDEPENDENCE – THE 10LESSONS I LEARN

May 31, 2020 by Kyith 5Comments

I first got to know Samuel when he reached out to me because he needed some help figuring out his plan for financial independence. He explained to me why his wife and himself are focus on accumulating for financial independence. That conversation also gave me a glimpse of the world of professional photography. I have this insecurity after I wrote about how freelancers shouldmanage their money

. I

wasn’t sure if what I wrote was realistic at all. So I reached out and asked Samuel whether he is willing to share his story with my readers. He was very gracious to share with us some of his life and money stories, lessons learned that enable him to feel financially stable and secure. You can check out his guide to the BEST wedding venuesand planning

a (kick-ass) wedding celebration as well as his creativeworks.

_If you think you have a unique life & money story that you would like to share with us, do contact me._ ------------------------- I had big dreams when I first set foot on the land down under back in2006.

I would ace my classes as a physiotherapy student. I had my sights on having my name upon the dean’s list. I planned to run my own physiotherapy practice. Perhaps even a chain of them. I was going to buy a house, settle down with kids, and go fishing on the weekend. Life was going to be great. It sounded like a perfect plan, _until it all came crashing down_. My name is Samuel, and I take pictures for a living. Most of my weekends are spent hanging out with couples making the biggest commitment of their lives, and then partying the night away in all sorts of manner possible. I know, it’s a far cry from what I initially envisioned my life tobe, right?

But let’s backtrack a little and start from the beginning. My family left for Australia when I was midway through my national service, and I packed my bags and joined them soon after. Life in Australia wasn’t what I dreamed it would be. I’ll sum it up by saying that a combination of unrealistic expectations, a sudden change in culture, and a two-year-long bout of severe eczema led to a long drawn battle with depression and an eatingdisorder.

My interactions with my younger classmates also helped me realize that my sheltered upbringing in Singapore in a middle-class household resulted in many shortcomings. Whilst proficient academically and perfectly skilled at memorizing and regurgitating, my critical thinking skills and emotional intelligence were severely lacking. I couldn’t even hold a decent conversation, for crying out loud. Although I was able to ace most of the exams, my poor communication and practical skills led to misunderstandings with patients and supervisors and poor execution of procedures that ultimately secured the demise of my hospital attachments. I had to repeat the year and the university removed me from my honors program. My appeals were rejected and no one, except for my honors supervisor, lifted a fingerto help.

As simple as that, I lost everything I worked for over a period of three years and I lost all interest for physiotherapy. I came back to Singapore and over the next six months, contemplated what to do with my life. Coming back to Singapore was tough, because, besides despair, I also felt shame – I felt like I had let down everyone who had believed in me. I took those two months to think… a lot. I thought about life, the meaning of life, the shortness of it. I would also think about my dreams if I had any and what they were. At the end of my trip, I couldn’t figure out what I wanted, but I knew one thing, that life was far too short to be stuck doing something not worth my time. So I made up my mind then, to pursue my passion and to become aphotographer.

Prior to this, I had never held a part-time job for more than three months other than a short stint as a sports trainer at the soccer club. This meant that my work experience solely consisted of massaging grown men’s calf muscles and carrying them off the field when theygot injured.

So I had to hustle and do photography work at all sorts of events. These jobs earn me a measly $10,000 after a grueling two years. I was ready to give up, but I hung on and went into photographing weddings. The lack of work then meant I tried to survive by taking on jobs both in Singapore and Australia just to make ends meet, and business began to gradually take off. My wife (who is also a photographer) and I have two independent brands. My wife serves mainly events in Singapore. I was able to have opportunities to work with clients in Perth, Australia. It was not always easy being away from her and those trips can be rather intense that I was not able to find time to visit my family in Australia. Our ability to deliver value to our clients has enabled us to gradually scale up our fees. Life became less of a struggle but it also opens up to some adult problems that we have to come to termswith.

I NEEDED TO MANAGE MY MONEY BETTER I was rather _ecstatic_ when I finally saw my savings account reach six figures for the first time. You have no idea how much I cherish having enough financial buffers such that I do not have to worry if I have enough money for myexpenses.

The nature of my projects-based work means that cash inflow tends to be uncertain. Our strategy, on a high level, is always to put a distance between our expenses and how many months of expenses our savings can last us. At least this is for my wife and me. Throughout my life, I have beenrather frugal.

When I started seeing my savings go up, I thought I better learn to manage my family’s money in the right way so that I will not lose what I have painstakingly built up. Being more introverted, I would try to see if I can find out what I don’t know online. I came across A Singapore Stock Investor . Ak71’s blog was a wealth of information. I greedily absorbed his sharing on * The right insurance policies to purchase * The impact of saving rates * Investing for passive income to supplement our lifestyles * The power of compound interest using CPF I devoured more articles and came across Mr. Money Mustache . Mr. Money Mustache gave me a path to focus upon to escape the challenges of the photography business. I have experienced the volatile industry dynamics and came to the conclusion that we might not be able to figure out the outlook of my niche in the next 5 years. Due to the physical nature of our work, I felt that it was impossible to keep up with the same level of dedication well into our 40s. By pursuing the path to financial independence, there was something in there that may give me a sense of security and not always be subject to the whims of this creative industry.CREATIVES AND MONEY

Kyith reached out to me to see if I could share my experience in managing both my money and the money aspects of my small business. I hope that by sharing my experience, some of my peers would recognize that they have to manage the money side of their life and businesswell.

The creative industry is an extremely competitive industry. There are consistently new players and the rules are always changing. The consistency is that you cannot rest on your laurels. Yet many creatives failed to join the dots between the dynamics of our industry with the money aspect. It is not uncommon to hear of stories of someone you think was doing very well suddenly fade away. It is only later that you hear that their business hit a snag they could not recover from. Cash flowproblems ensued.

I would be the first to admit I have not got the money formula sorted to perfection but I hope that some of what works for me would work foryou as well.

So here is the first lesson. LESSON #1 – CALCULATE YOUR EARNINGS BASED ON NET PROFIT In our industry, the money comes in a lumpy fashion. It is not uncommon to be paid a sum that you can spend for 1 or 2 months (or even more). February and August tend to be months which are relativelyquiet as well.

My observation is that some of my peers cannot match the cash inflow with their cash outflow. Our cash outflow tends to be more recurring. Resolving between lumpy and recurring can be a nightmare for creatives. They will think that they could consistently bring in projects that pays them a lumpy cash flow. When there is a late payment, or a seasonal period where they did not get jobs, they had to dig deeperinto their savings.

I find that if we account based on net profit, it allows me to see how much we are making, net of expenses much better. When customers pay me a big lumpy payout, I do not get overly ecstatic about it as I know part of it will need to pay for some business expenses in thefollowing months.

LESSON #2 – PLAN AHEAD IF YOU ARE THINKING OF APPLYING FOR A HOUSING LOAN AS A FREELANCER. When we came back to Singapore, we stayed in rented HDB flats. Renting was not always a great experience. The last place we rented had such a weird layout that we just could not get a good night’s sleep. That experience was the ultimate and we decided to get a placeof our own.

However, when we wanted to get a place of our own, every bank rejected our application for a housing loan, even an independent financial advisor shook his head. Apparently, it seems that as a self-employed, your credit scores are much lower than if you were an employee. In order to obtain a housing loan, you need to provide a level of certainty of being able to service the loan. That includes two years’ worth of IRAS Notice of Assessments and CPF contributions. Financial institutions also generally assume that as a freelancer, your income is unstable, hence they will reduce your stated monthly income by 30% when calculating your Total Debt Servicing Ratio. Therefore, ensure that the price of the house you are looking at fits within your budget based on your level of income before applying for aloan.

LESSON #3 – SEPARATE YOUR BUSINESS AND PERSONAL ACCOUNTS AND SET UPRAIN BUCKETS

Despite the amount of time and effort we put into our business, as a wedding photographer, there are multiple factors that can impact the amount of work we end up booking. As a result, the income we earn can drastically fluctuate every year. We felt that it is absolutely essential to creating separate business accounts and personal accounts. The business accounts then pay a recurring income into our personal accounts. Then we further divide our personal accounts into sub-accounts for different goals.Deduct

your business expense from your revenue. Then pay yourself a salary. Our plan can be illustrated in the diagram above. Our business account records all invoices and expenses. From this business account, we pay ourselves a consistent salary of $5000 (as anexample).

We were fortunate that our business account can pay a consistent salary. This income gives us stability. We can then accurately funnel this $5,000 into 5 different “rain buckets”, each with a particular life goal. The rain buckets create boundaries between the money meant for different purposes so that we know if we are overspending in some areas and whether our wealth machine is getting stronger. We use apps to create virtual rain buckets. You can check out applications such as YOU-NEED-A-BUDGET (YNAB) and WALLY to help you dothis.

LESSON #4 – KNOW WHERE YOU ARE AND WHERE YOU WANT TO BE As I went deeper down the financial education rabbit hole, Mr Money Mustache taught me one of the most important concepts. This was the FIRE concept or financial independence, retire early. Reading on financial independence where the passive income I earned could potentially cover my lifestyle expenses was a great revelation for me, and I saw a practical solution to my problems. However, we need to know where we stand (financially), before we can plan our destination and how we can get there. I will recommend that you tally up all your assets and liabilities and creating a statement of net worth that you can update on a monthlybasis.

Here is an example that worked well for us:Samuel’s

way of tracking the net worth We use a simple tracking where we laid out all our assets (cash, equities, CPF, bonds, property), our liabilities, and net worth. We felt more relaxed when we saw our numbers getting better. When I learn about the shockingly simple math behind early retirement,

you get more motivated when you realize the math might work out inreality.

Despite earning well, our lifestyle expenditure was keeping up with our earnings and we couldn’t save much. When we start tracking these numbers, we begin noticing where the problems are. We discussed and found that some of our spendings were unnecessary and so we reducedthem…

Where I learn from Kyith is to also create a separate column ofessential expenses.

This allows us to have an idea if we need to really cut back (like during this Covid-19 period), we know how much we can live on, what is the quality of life, and roughly how much to cut back. By doing this, we get a clearer picture about where we are. We can then consider where we want to get to. HOW MANY PROJECTS FOR ME TO REACH FINANCIAL INDEPENDENCE? After evaluating the formula to financial independence by Mr Money Mustache, I began to see how I can link how much we need to accumulate with our photography work. Recently, I shared with some of my peers how I link where I want to bewith my daily work:

Samuel’s

business plan that will lead to financial independence. Going through this exercise allows me to see whether my goal is realistic or not. For example, based on my past experience, can I do 40 weddings and 20 pre-weddings in a year. Can I raise my rate? It also gives me an indicator whether I am working too hard. Instead of always focusing on a dreamy goal, I can get to business to focus on getting X number of weddings and Y number of events. LESSON #4 – BUILDING A SOLID EMERGENCY FUND Most financial gurus advocate for six months of emergency fund. However, I understood early on how financially rocky it can be as a freelancer, and I felt that I needed AT LEAST 12 – 24 MONTHS OF ESSENTIAL EXPENSES because when shit hits the fan, it hits hard. I didn’t predict this pandemic, but I guess I prepared for it allalong.

Building up your emergency fund is so important in providing lifestyle stability during times like this when the entire industry is halted and there is no foreseeable work for the next 1-2 years, or if we encounter any crippling injury that stops us from being able to work. In case of a recession, it also acts as a buffer to prevent us from selling our equities or bonds at a loss for liquidity. LESSON #5 – HIGH SAVINGS RATE MATTERS FOR MY GOAL The spectrum of profit that creatives can earn in the industry vary widely. There are some who despite their best efforts, could not put a distance between their expenses and what they earn. Then there are some who get huge revenue bumps once once in a while. As we steadied each of our individual businesses, we were getting our work calendar filled and we were earning good money. Yet I noticed we weren’t feeling like we were saving well. We realized that was because our lifestyle expenses crept up as ourearnings increased.

Reading both Mr Money Moustache and ASSIÂ on savings rate helped me understand how important it was to keep expenses low, whilst increasing earnings so that we have a high savings rate. I realize if I want to reach my financial goal, we have got tosomething.

Your savings rate is the percentage of your salary that you do not spend. According to conventional theory, a 20% savings rate will not cut it, and here’s why. Assuming that you spend the remainder of your salary: * SAVING 50% OF YOUR SALARY means that for every one year that you work, you can take one year off. * SAVING 20% OF YOUR SALARY means that every five years that you work, you can take one year off. Hence, if you want to retire for 30 years at the age of 50 and without additional wealth building tools, you will need to save for 150 years – This does not make sense to me at all, and it’s virtually impossible to retire. However, SAVING 80% OF YOUR SALARY means that every ten years that you work, you can take forty years off. That is why a high savings rate is so crucial for early retirement. It’s important that we live comfortably, but at the same time minimising our expenses ensured a higher savings rate. Early on, we made the decision to not own a car, purchase a smaller flat to reduce our mortgage payments, and to cook at home more often to build up our savings. This worked to our advantage as we increased our wealth gap, thereby channeling the extra savings to instruments that generate more passiveincome.

LESSON #6 – BUY TERM AND INVEST THE REST Early in my career, I had an accident and broke both my wrists. I still went on to photograph a wedding the next day for twelve grueling hours with both my arms in casts – that incident solidified the importance of insurance. INSURANCE DOESN’T HAVE TO BE EXPENSIVE. From the meager returns of my parent’s investment-linked insurance policies after ten years, I learned at a young age that those are pretty mediocre instruments for building wealth. The purpose of insurance is to, well.. insure! Or rather, to provide a source of income for our dependables in the unfortunate event of our passing or loss of function. A solid TERM INSURANCE PLAN that pays out in the event of death, critical illness or total permanent disability will solve that, and they are fairly inexpensive, especially if you start young. A hospital shield plan is also absolutely essential in the event that we need to be hospitalised for whatever reasons. A hefty medical bill is a surefire way to diminish our savings, and it’s far better to budget a set amount to negate that unknown scary possibility. For the above, I’ll recommend a fee-only financial planner. This ensures that they will recommend the right products for you without any reward bias in the form of commissions and kickbacks. MoneyOwl will be a great place to start for most (this post is non-sponsored nor am I affiliated to MoneyOwlin any way).