6

More Annotations

4

6

Favourite Annotations

6

4

Text

LIFESCIVC | BRUCE BOOTH, PARTNER AT ATLAS VENTURE, BLOGSBIOTECH FINANCINGVC-BACKED BIOTECH RETURNSBUSINESS DEVELOPMENTTALENT Despite saving the world from COVID, pharma and biotech are still in the crosshairs of many politicians. With many anti-Pharma politicians and regulators emboldened in the current environment, and with more aggressive tax and spending policy in the works, there a number of risks to biotech over the next 1-2 years out of Washington. THE BIOTECH JOB MARKET IS AS HOT AS THE HOUSING MARKET The biotech job market is a bit like the suburban housing market—red hot. It’s a buyer’s market, don’t waive your inspection rights! By Pamela L. Esposito, CBO of Replimune as part of the From The Trenches feature of LifeSciVC.. It is possibly the tightest biotech Email

The universe of public biotech companies has been growing for a decade, and increasingly so in the past few years as the IPO market has flourished. Hundreds of young aspiring biotechs have tapped into the public equity markets, swelling the ranks of small- and mid-capEmail

Email

Despite saving the world from COVID, pharma and biotech are still in the crosshairs of many politicians. With many anti-Pharma politicians and regulators emboldened in the current environment, and with more aggressive tax and spending policy in the works, there a number of risks to biotech over the next 1-2 years out of Washington. Here are five themes that could cause sleepless nights: drug pricing, deal-making constraints, drug approval uncertainty, inflationary pressures, and adverse tax policy changes. Some of these are priced into the markets already, some are not. Depending on how they unfold, these risks could even resolve to the upside, in ways more favorable than current expectations. But all of these risks have the ability to shape market sentiment for biopharma, as well as accelerate sector rotations and asset class reallocations. Of course, each risk is not created equal. Some pose more significant threats to innovation than others. Yet all could be impactful, so figuring out how to mitigate the downside risks and position the sector most favorably for the long run is important. Here’s my rather long-winded take on these five macro risks and some possible implications to the sector. * DRUG PRICING OVERHAUL COULD HURT INNOVATION. We’re likely to see drug legislation of some sort this year as certain politicians from both sides of the isle embrace a populist anti-Pharma view of the world; it seems the drumbeat for “doing something” has become too loud to ignore. Rather than address the real issues around insurance and out-of-pocket costs, Pharma is an easy albeit lazy targetEmail

TWITTER

labor

REIMAGINING THE WORKPLACE POST PANDEMIC In a recent Harvard Business Review report (Figure 2) virtually all respondents felt that workplace wellbeing had declined since the pandemic. This is no surprise, but interestingly, 56% noted that increased job demands were to blame in large part due to a loss of work-life separation. Only 24% of respondents noted feeling of lostconnection

BIOTECH FUNDING TOPS THE CHARTS AGAIN Venture funding for US-based biopharma companies in 1Q 2021 topped the charts above $12B for the first time ever according to Pitchbook; amazingly, we’ve had 4 straight chart-topping quarters in a row. IPOs raised over $5B, making it one of the strongest quarters ever (#2 behind 3Q 2020). And public follow-on financings topped $11B, againone

SELECTIVE ALLOSTERIC TYK2 INHIBITORS Deucravacitinib is the first truly selective TYK2 inhibitor due to the fact that it targets the allosteric site. Due to improvements in the Nimbus chemical series, our TYK2 allosteric inhibitor extends these margins on JAK1, 2, and 3 even further. Until the BMS paper on deucravacitinib’s Phase 2b results in psoriasis ( NEJM, Sept 2018 ),the

NEW BIOTECH CORPORATE STRUCTURES: POSSIBLE ALTERNATIVES Not a biotech conference goes by these days without a discussion about new models for financing or exiting companies, and BioPharm America in Boston this week is no different. I’m on a panel discussing the topic on Wednesday afternoon. New BIOTECH STARTUPS AND THE HARD TRUTH OF INNOVATION Gary Pisano’s recent Harvard Business Review piece, The Hard Truth About Innovative Cultures, beautifully frames up how innovative corporate environments are frequently misunderstood.Innovative startups aren’t just about being cool and nimble, having beer taps in the kitchen, or an endless bounty of swag. Pisano sums up the harder, harsher reality of truly innovative WHERE DOES ALL THAT BIOTECH VENTURE CAPITAL GO Venture capital investing in biotech has long been hard to disaggregate: how much goes to “early stage” vs “late stage”, how much goes to CNS vs oncology, discovery vs Phase 3, etc Today BIO’s David Thomas and Chad Wessel have SEVEN HABITS OF CELGENE’S HIGHLY SUCCESSFUL STRATEGY Seven Habits of Celgene’s Highly Successful Strategy. Over the past seven years, Celgene has emerged as one of the most active and creative deal-makers in the biopharma industry. The Boston Consulting Group’s Biopharma Partnering Survey and Benchmarking analysis examines BD activity and perceptions across the industry, and their2014

RETURN OF THE JEDI: STROMEDIX ACQUIRED BY BIOGEN Return of the Jedi: Stromedix Acquired by Biogen. Biogen just announced its acquisition of Stromedix for up to $562M. Another solid M&A exit in biotech emphasizing how innovation matters. With a very different model than Avila Therapeutics, an exit we announced in January, Stromedix is a biology-focused, asset-centric companydedicated to

LIFESCIVC | BRUCE BOOTH, PARTNER AT ATLAS VENTURE, BLOGSBIOTECH FINANCINGVC-BACKED BIOTECH RETURNSBUSINESS DEVELOPMENTTALENT Despite saving the world from COVID, pharma and biotech are still in the crosshairs of many politicians. With many anti-Pharma politicians and regulators emboldened in the current environment, and with more aggressive tax and spending policy in the works, there a number of risks to biotech over the next 1-2 years out of Washington. THE BIOTECH JOB MARKET IS AS HOT AS THE HOUSING MARKET The biotech job market is a bit like the suburban housing market—red hot. It’s a buyer’s market, don’t waive your inspection rights! By Pamela L. Esposito, CBO of Replimune as part of the From The Trenches feature of LifeSciVC.. It is possibly the tightest biotechlabor

REIMAGINING THE WORKPLACE POST PANDEMIC In a recent Harvard Business Review report (Figure 2) virtually all respondents felt that workplace wellbeing had declined since the pandemic. This is no surprise, but interestingly, 56% noted that increased job demands were to blame in large part due to a loss of work-life separation. Only 24% of respondents noted feeling of lostconnection

BIOTECH FUNDING TOPS THE CHARTS AGAIN Venture funding for US-based biopharma companies in 1Q 2021 topped the charts above $12B for the first time ever according to Pitchbook; amazingly, we’ve had 4 straight chart-topping quarters in a row. IPOs raised over $5B, making it one of the strongest quarters ever (#2 behind 3Q 2020). And public follow-on financings topped $11B, againone

SELECTIVE ALLOSTERIC TYK2 INHIBITORS Deucravacitinib is the first truly selective TYK2 inhibitor due to the fact that it targets the allosteric site. Due to improvements in the Nimbus chemical series, our TYK2 allosteric inhibitor extends these margins on JAK1, 2, and 3 even further. Until the BMS paper on deucravacitinib’s Phase 2b results in psoriasis ( NEJM, Sept 2018 ),the

NEW BIOTECH CORPORATE STRUCTURES: POSSIBLE ALTERNATIVES Not a biotech conference goes by these days without a discussion about new models for financing or exiting companies, and BioPharm America in Boston this week is no different. I’m on a panel discussing the topic on Wednesday afternoon. New BIOTECH STARTUPS AND THE HARD TRUTH OF INNOVATION Gary Pisano’s recent Harvard Business Review piece, The Hard Truth About Innovative Cultures, beautifully frames up how innovative corporate environments are frequently misunderstood.Innovative startups aren’t just about being cool and nimble, having beer taps in the kitchen, or an endless bounty of swag. Pisano sums up the harder, harsher reality of truly innovative WHERE DOES ALL THAT BIOTECH VENTURE CAPITAL GO Venture capital investing in biotech has long been hard to disaggregate: how much goes to “early stage” vs “late stage”, how much goes to CNS vs oncology, discovery vs Phase 3, etc Today BIO’s David Thomas and Chad Wessel have SEVEN HABITS OF CELGENE’S HIGHLY SUCCESSFUL STRATEGY Seven Habits of Celgene’s Highly Successful Strategy. Over the past seven years, Celgene has emerged as one of the most active and creative deal-makers in the biopharma industry. The Boston Consulting Group’s Biopharma Partnering Survey and Benchmarking analysis examines BD activity and perceptions across the industry, and their2014

RETURN OF THE JEDI: STROMEDIX ACQUIRED BY BIOGEN Return of the Jedi: Stromedix Acquired by Biogen. Biogen just announced its acquisition of Stromedix for up to $562M. Another solid M&A exit in biotech emphasizing how innovation matters. With a very different model than Avila Therapeutics, an exit we announced in January, Stromedix is a biology-focused, asset-centric companydedicated to

SELECTIVE ALLOSTERIC TYK2 INHIBITORS Deucravacitinib is the first truly selective TYK2 inhibitor due to the fact that it targets the allosteric site. Due to improvements in the Nimbus chemical series, our TYK2 allosteric inhibitor extends these margins on JAK1, 2, and 3 even further. Until the BMS paper on deucravacitinib’s Phase 2b results in psoriasis ( NEJM, Sept 2018 ),the

BIOTECH FUNDING TOPS THE CHARTS AGAIN Venture funding for US-based biopharma companies in 1Q 2021 topped the charts above $12B for the first time ever according to Pitchbook; amazingly, we’ve had 4 straight chart-topping quarters in a row. IPOs raised over $5B, making it one of the strongest quarters ever (#2 behind 3Q 2020). And public follow-on financings topped $11B, againone

THE ELEPHANT IN THE ROOM By Philip Astley-Sparke, CEO of Replimune, as part of the From The Trenches feature of LifeSciVC. One of the biggest elephants in the room regarding starting and scaling young companies is the tension, often healthy but sometimes detrimental, that exist between CEOs and venture capital firms. THE RECORD-BREAKING BIOTECH FUNDING TSUNAMI OF 1H2020 According to data from BMO Capital Markets, in aggregate, we’ve seen over $17.6B in equity funding in 2Q2020 into biopharma across both IPOs and follow-on’s (excluding offerings from Regeneron and Royalty Pharma). The biotech IPO fundraising level, in terms of capital raised, is the largest ever witnessed in a quarter, and the follow-on BIOTECH SCIENTIFIC ADVISORY BOARDS: WHAT WORKS, WHAT DOESN Cons – The real costs of a poorly used SAB. SABs don’t come for free . Good ones are a lot of work. And they are also costly for a startup in terms of dollars and equity. A typical SAB member may charge $2.5-5K per day and receive 0.1-0.3% equity. Hollywood-star advisors can be much, much more expensive than that on the equityfront.

LITTLE BY LITTLE: REAL LIFE LESSONS IN BUSINESS Little by Little: Real Life Lessons In Business Development. Posted April 16th, 2018 by Tariq Kassum, in Business Development, From The Trenches. This blog was written by Tariq Kassum, COO and Head of Corporate Development at Obsidian Therapeutics, as part of the From The Trenches feature of LifeSciVC. Experience can be a tough teacher. SEVEN HABITS OF CELGENE’S HIGHLY SUCCESSFUL STRATEGY Over the past seven years, Celgene has emerged as one of the most active and creative deal-makers in the biopharma industry. The Boston Consulting Group’s Biopharma Partnering Survey and Benchmarking analysis examines BD activity and perceptions across the industry, and their 2014 analysis was very telling. Celgene scored as the best partner on 78% of the partnering and culture metrics (7/9 OUR EXPERIENCE WITH FIRST-TIME BIOTECH CEOS: FIVE Of the 34 biotech companies, a whopping 82% had first-time CEOs. Further, only 26% of our CEOs had worked for prior Atlas companies; the vast majority were, by that definition, “new” relationships in the Atlas portfolio. Many of these were new introductions to our firm, often through referrals or via executive search processes. HIGH-PERFORMING BOARDS IN EARLY STAGE BIOTECH High-Performing Boards in Early Stage Biotech. Posted March 3rd, 2012 in Biotech startup advice, General Venture Capital. Having a highly functional and productive Board of Directors is a key ingredient for success for most companies, but its of particular importance for early stage startups. The web is full of advice around what are the BIOTECH CEO PAY: INFLATION HELD AT BAY Biotech CEO Pay: Inflation Held At Bay. The private biotech sector is awash in capital today: funding over the last few quarters has been record-breaking, up over 250% since 2013, as biotech CEOs have worked hard to strengthen their companies’ balance sheets. But in the process of filling up their corporate coffers, have they also filledup

LIFESCIVC | BRUCE BOOTH, PARTNER AT ATLAS VENTURE, BLOGSBIOTECH FINANCINGVC-BACKED BIOTECH RETURNSBUSINESS DEVELOPMENTTALENT Despite saving the world from COVID, pharma and biotech are still in the crosshairs of many politicians. With many anti-Pharma politicians and regulators emboldened in the current environment, and with more aggressive tax and spending policy in the works, there a number of risks to biotech over the next 1-2 years out of Washington. THE BIOTECH JOB MARKET IS AS HOT AS THE HOUSING MARKET The biotech job market is a bit like the suburban housing market—red hot. It’s a buyer’s market, don’t waive your inspection rights! By Pamela L. Esposito, CBO of Replimune as part of the From The Trenches feature of LifeSciVC.. It is possibly the tightest biotechlabor

REIMAGINING THE WORKPLACE POST PANDEMIC In a recent Harvard Business Review report (Figure 2) virtually all respondents felt that workplace wellbeing had declined since the pandemic. This is no surprise, but interestingly, 56% noted that increased job demands were to blame in large part due to a loss of work-life separation. Only 24% of respondents noted feeling of lostconnection

BIOTECH FUNDING TOPS THE CHARTS AGAIN Venture funding for US-based biopharma companies in 1Q 2021 topped the charts above $12B for the first time ever according to Pitchbook; amazingly, we’ve had 4 straight chart-topping quarters in a row. IPOs raised over $5B, making it one of the strongest quarters ever (#2 behind 3Q 2020). And public follow-on financings topped $11B, againone

SELECTIVE ALLOSTERIC TYK2 INHIBITORS Deucravacitinib is the first truly selective TYK2 inhibitor due to the fact that it targets the allosteric site. Due to improvements in the Nimbus chemical series, our TYK2 allosteric inhibitor extends these margins on JAK1, 2, and 3 even further. Until the BMS paper on deucravacitinib’s Phase 2b results in psoriasis ( NEJM, Sept 2018 ),the

NEW BIOTECH CORPORATE STRUCTURES: POSSIBLE ALTERNATIVES Not a biotech conference goes by these days without a discussion about new models for financing or exiting companies, and BioPharm America in Boston this week is no different. I’m on a panel discussing the topic on Wednesday afternoon. New BIOTECH STARTUPS AND THE HARD TRUTH OF INNOVATION Gary Pisano’s recent Harvard Business Review piece, The Hard Truth About Innovative Cultures, beautifully frames up how innovative corporate environments are frequently misunderstood.Innovative startups aren’t just about being cool and nimble, having beer taps in the kitchen, or an endless bounty of swag. Pisano sums up the harder, harsher reality of truly innovative BIOTECH VENTURE DEAL TERMS ARE MORE "STARTUP-FRIENDLY Biotech Venture Deal Terms Are More “Startup-Friendly” Than Ever. Posted September 10th, 2018 in Biotech financing, Fundraising. Biotech is booming, with eye-popping new financings seemingly announced daily. The sector is having an epic year for startup fundraising, breaking records for what will end up as the most active private biotech WHERE DOES ALL THAT BIOTECH VENTURE CAPITAL GO Venture capital investing in biotech has long been hard to disaggregate: how much goes to “early stage” vs “late stage”, how much goes to CNS vs oncology, discovery vs Phase 3, etc Today BIO’s David Thomas and Chad Wessel have RETURN OF THE JEDI: STROMEDIX ACQUIRED BY BIOGEN Return of the Jedi: Stromedix Acquired by Biogen. Biogen just announced its acquisition of Stromedix for up to $562M. Another solid M&A exit in biotech emphasizing how innovation matters. With a very different model than Avila Therapeutics, an exit we announced in January, Stromedix is a biology-focused, asset-centric companydedicated to

LIFESCIVC | BRUCE BOOTH, PARTNER AT ATLAS VENTURE, BLOGSBIOTECH FINANCINGVC-BACKED BIOTECH RETURNSBUSINESS DEVELOPMENTTALENT Despite saving the world from COVID, pharma and biotech are still in the crosshairs of many politicians. With many anti-Pharma politicians and regulators emboldened in the current environment, and with more aggressive tax and spending policy in the works, there a number of risks to biotech over the next 1-2 years out of Washington. THE BIOTECH JOB MARKET IS AS HOT AS THE HOUSING MARKET The biotech job market is a bit like the suburban housing market—red hot. It’s a buyer’s market, don’t waive your inspection rights! By Pamela L. Esposito, CBO of Replimune as part of the From The Trenches feature of LifeSciVC.. It is possibly the tightest biotechlabor

REIMAGINING THE WORKPLACE POST PANDEMIC In a recent Harvard Business Review report (Figure 2) virtually all respondents felt that workplace wellbeing had declined since the pandemic. This is no surprise, but interestingly, 56% noted that increased job demands were to blame in large part due to a loss of work-life separation. Only 24% of respondents noted feeling of lostconnection

BIOTECH FUNDING TOPS THE CHARTS AGAIN Venture funding for US-based biopharma companies in 1Q 2021 topped the charts above $12B for the first time ever according to Pitchbook; amazingly, we’ve had 4 straight chart-topping quarters in a row. IPOs raised over $5B, making it one of the strongest quarters ever (#2 behind 3Q 2020). And public follow-on financings topped $11B, againone

SELECTIVE ALLOSTERIC TYK2 INHIBITORS Deucravacitinib is the first truly selective TYK2 inhibitor due to the fact that it targets the allosteric site. Due to improvements in the Nimbus chemical series, our TYK2 allosteric inhibitor extends these margins on JAK1, 2, and 3 even further. Until the BMS paper on deucravacitinib’s Phase 2b results in psoriasis ( NEJM, Sept 2018 ),the

NEW BIOTECH CORPORATE STRUCTURES: POSSIBLE ALTERNATIVES Not a biotech conference goes by these days without a discussion about new models for financing or exiting companies, and BioPharm America in Boston this week is no different. I’m on a panel discussing the topic on Wednesday afternoon. New BIOTECH STARTUPS AND THE HARD TRUTH OF INNOVATION Gary Pisano’s recent Harvard Business Review piece, The Hard Truth About Innovative Cultures, beautifully frames up how innovative corporate environments are frequently misunderstood.Innovative startups aren’t just about being cool and nimble, having beer taps in the kitchen, or an endless bounty of swag. Pisano sums up the harder, harsher reality of truly innovative BIOTECH VENTURE DEAL TERMS ARE MORE "STARTUP-FRIENDLY Biotech Venture Deal Terms Are More “Startup-Friendly” Than Ever. Posted September 10th, 2018 in Biotech financing, Fundraising. Biotech is booming, with eye-popping new financings seemingly announced daily. The sector is having an epic year for startup fundraising, breaking records for what will end up as the most active private biotech WHERE DOES ALL THAT BIOTECH VENTURE CAPITAL GO Venture capital investing in biotech has long been hard to disaggregate: how much goes to “early stage” vs “late stage”, how much goes to CNS vs oncology, discovery vs Phase 3, etc Today BIO’s David Thomas and Chad Wessel have RETURN OF THE JEDI: STROMEDIX ACQUIRED BY BIOGEN Return of the Jedi: Stromedix Acquired by Biogen. Biogen just announced its acquisition of Stromedix for up to $562M. Another solid M&A exit in biotech emphasizing how innovation matters. With a very different model than Avila Therapeutics, an exit we announced in January, Stromedix is a biology-focused, asset-centric companydedicated to

BIOTECH FUNDING TOPS THE CHARTS AGAIN Venture funding for US-based biopharma companies in 1Q 2021 topped the charts above $12B for the first time ever according to Pitchbook; amazingly, we’ve had 4 straight chart-topping quarters in a row. IPOs raised over $5B, making it one of the strongest quarters ever (#2 behind 3Q 2020). And public follow-on financings topped $11B, againone

SELECTIVE ALLOSTERIC TYK2 INHIBITORS Deucravacitinib is the first truly selective TYK2 inhibitor due to the fact that it targets the allosteric site. Due to improvements in the Nimbus chemical series, our TYK2 allosteric inhibitor extends these margins on JAK1, 2, and 3 even further. Until the BMS paper on deucravacitinib’s Phase 2b results in psoriasis ( NEJM, Sept 2018 ),the

THE RECORD-BREAKING BIOTECH FUNDING TSUNAMI OF 1H2020 According to data from BMO Capital Markets, in aggregate, we’ve seen over $17.6B in equity funding in 2Q2020 into biopharma across both IPOs and follow-on’s (excluding offerings from Regeneron and Royalty Pharma). The biotech IPO fundraising level, in terms of capital raised, is the largest ever witnessed in a quarter, and the follow-on THE BIOTECH PARADOX OF 2020: A YEAR IN REVIEW According to preliminary data from Pitchbook, over $26B of venture funding went into US-based biotech firms in 2020, with several quarters topping the charts for record-breaking funding ( the “tsunami” in the first half continued into the second half of the year). 2018 was the prior high, and only hit $19B. This impliesUS-based private

BIOTECH SCIENTIFIC ADVISORY BOARDS: WHAT WORKS, WHAT DOESN Cons – The real costs of a poorly used SAB. SABs don’t come for free . Good ones are a lot of work. And they are also costly for a startup in terms of dollars and equity. A typical SAB member may charge $2.5-5K per day and receive 0.1-0.3% equity. Hollywood-star advisors can be much, much more expensive than that on the equityfront.

LITTLE BY LITTLE: REAL LIFE LESSONS IN BUSINESS Little by Little: Real Life Lessons In Business Development. Posted April 16th, 2018 by Tariq Kassum, in Business Development, From The Trenches. This blog was written by Tariq Kassum, COO and Head of Corporate Development at Obsidian Therapeutics, as part of the From The Trenches feature of LifeSciVC. Experience can be a tough teacher. OUR EXPERIENCE WITH FIRST-TIME BIOTECH CEOS: FIVE Of the 34 biotech companies, a whopping 82% had first-time CEOs. Further, only 26% of our CEOs had worked for prior Atlas companies; the vast majority were, by that definition, “new” relationships in the Atlas portfolio. Many of these were new introductions to our firm, often through referrals or via executive search processes. SEVEN HABITS OF CELGENE’S HIGHLY SUCCESSFUL STRATEGY Over the past seven years, Celgene has emerged as one of the most active and creative deal-makers in the biopharma industry. The Boston Consulting Group’s Biopharma Partnering Survey and Benchmarking analysis examines BD activity and perceptions across the industry, and their 2014 analysis was very telling. Celgene scored as the best partner on 78% of the partnering and culture metrics (7/9 HIGH-PERFORMING BOARDS IN EARLY STAGE BIOTECH High-Performing Boards in Early Stage Biotech. Posted March 3rd, 2012 in Biotech startup advice, General Venture Capital. Having a highly functional and productive Board of Directors is a key ingredient for success for most companies, but its of particular importance for early stage startups. The web is full of advice around what are the BIOTECH CEO PAY: INFLATION HELD AT BAY Biotech CEO Pay: Inflation Held At Bay. The private biotech sector is awash in capital today: funding over the last few quarters has been record-breaking, up over 250% since 2013, as biotech CEOs have worked hard to strengthen their companies’ balance sheets. But in the process of filling up their corporate coffers, have they also filledup

LIFESCIVC | BRUCE BOOTH, PARTNER AT ATLAS VENTURE, BLOGSBIOTECH FINANCINGVC-BACKED BIOTECH RETURNSBUSINESS DEVELOPMENTTALENT Despite saving the world from COVID, pharma and biotech are still in the crosshairs of many politicians. With many anti-Pharma politicians and regulators emboldened in the current environment, and with more aggressive tax and spending policy in the works, there a number of risks to biotech over the next 1-2 years out of Washington. ABOUT ME | LIFESCIVCLIFESCIVC About Bruce Booth. I’m an early stage venture capitalist. Like my partners at Atlas Venture, I enjoy working with great scientists and entrepreneurs to start new biotech companies. In short, we focus on seed-led venture creation around the discovery and development of novel therapeutics. Since joining Atlas in 2005, I’ve been involvedin

THE BIOTECH JOB MARKET IS AS HOT AS THE HOUSING MARKET The biotech job market is a bit like the suburban housing market—red hot. It’s a buyer’s market, don’t waive your inspection rights! By Pamela L. Esposito, CBO of Replimune as part of the From The Trenches feature of LifeSciVC.. It is possibly the tightest biotechlabor

REIMAGINING THE WORKPLACE POST PANDEMIC In a recent Harvard Business Review report (Figure 2) virtually all respondents felt that workplace wellbeing had declined since the pandemic. This is no surprise, but interestingly, 56% noted that increased job demands were to blame in large part due to a loss of work-life separation. Only 24% of respondents noted feeling of lostconnection

BIOTECH FUNDING TOPS THE CHARTS AGAIN Venture funding for US-based biopharma companies in 1Q 2021 topped the charts above $12B for the first time ever according to Pitchbook; amazingly, we’ve had 4 straight chart-topping quarters in a row. IPOs raised over $5B, making it one of the strongest quarters ever (#2 behind 3Q 2020). And public follow-on financings topped $11B, againone

THE ELEPHANT IN THE ROOM By Philip Astley-Sparke, CEO of Replimune, as part of the From The Trenches feature of LifeSciVC. One of the biggest elephants in the room regarding starting and scaling young companies is the tension, often healthy but sometimes detrimental, that exist between CEOs and venture capital firms. SELECTIVE ALLOSTERIC TYK2 INHIBITORS Deucravacitinib is the first truly selective TYK2 inhibitor due to the fact that it targets the allosteric site. Due to improvements in the Nimbus chemical series, our TYK2 allosteric inhibitor extends these margins on JAK1, 2, and 3 even further. Until the BMS paper on deucravacitinib’s Phase 2b results in psoriasis ( NEJM, Sept 2018 ),the

PERSONAL REFLECTION: EMPATHY IN THE WORKPLACE Personal Reflection: Empathy In The Workplace. Just before I chaired a Board meeting last year, I spent a frustratingly painful hour going through many of the uncomfortable details of my divorce process and a set of emotional custody issues with my lawyers. Immediately after hanging up, with only minutes of transition, I put on my best poker NEW BIOTECH CORPORATE STRUCTURES: POSSIBLE ALTERNATIVES Not a biotech conference goes by these days without a discussion about new models for financing or exiting companies, and BioPharm America in Boston this week is no different. I’m on a panel discussing the topic on Wednesday afternoon. New BIOTECH STARTUPS AND THE HARD TRUTH OF INNOVATION Gary Pisano’s recent Harvard Business Review piece, The Hard Truth About Innovative Cultures, beautifully frames up how innovative corporate environments are frequently misunderstood.Innovative startups aren’t just about being cool and nimble, having beer taps in the kitchen, or an endless bounty of swag. Pisano sums up the harder, harsher reality of truly innovative LIFESCIVC | BRUCE BOOTH, PARTNER AT ATLAS VENTURE, BLOGSBIOTECH FINANCINGVC-BACKED BIOTECH RETURNSBUSINESS DEVELOPMENTTALENT Despite saving the world from COVID, pharma and biotech are still in the crosshairs of many politicians. With many anti-Pharma politicians and regulators emboldened in the current environment, and with more aggressive tax and spending policy in the works, there a number of risks to biotech over the next 1-2 years out of Washington. ABOUT ME | LIFESCIVCLIFESCIVC About Bruce Booth. I’m an early stage venture capitalist. Like my partners at Atlas Venture, I enjoy working with great scientists and entrepreneurs to start new biotech companies. In short, we focus on seed-led venture creation around the discovery and development of novel therapeutics. Since joining Atlas in 2005, I’ve been involvedin

THE BIOTECH JOB MARKET IS AS HOT AS THE HOUSING MARKET The biotech job market is a bit like the suburban housing market—red hot. It’s a buyer’s market, don’t waive your inspection rights! By Pamela L. Esposito, CBO of Replimune as part of the From The Trenches feature of LifeSciVC.. It is possibly the tightest biotechlabor

REIMAGINING THE WORKPLACE POST PANDEMIC In a recent Harvard Business Review report (Figure 2) virtually all respondents felt that workplace wellbeing had declined since the pandemic. This is no surprise, but interestingly, 56% noted that increased job demands were to blame in large part due to a loss of work-life separation. Only 24% of respondents noted feeling of lostconnection

BIOTECH FUNDING TOPS THE CHARTS AGAIN Venture funding for US-based biopharma companies in 1Q 2021 topped the charts above $12B for the first time ever according to Pitchbook; amazingly, we’ve had 4 straight chart-topping quarters in a row. IPOs raised over $5B, making it one of the strongest quarters ever (#2 behind 3Q 2020). And public follow-on financings topped $11B, againone

THE ELEPHANT IN THE ROOM By Philip Astley-Sparke, CEO of Replimune, as part of the From The Trenches feature of LifeSciVC. One of the biggest elephants in the room regarding starting and scaling young companies is the tension, often healthy but sometimes detrimental, that exist between CEOs and venture capital firms. SELECTIVE ALLOSTERIC TYK2 INHIBITORS Deucravacitinib is the first truly selective TYK2 inhibitor due to the fact that it targets the allosteric site. Due to improvements in the Nimbus chemical series, our TYK2 allosteric inhibitor extends these margins on JAK1, 2, and 3 even further. Until the BMS paper on deucravacitinib’s Phase 2b results in psoriasis ( NEJM, Sept 2018 ),the

PERSONAL REFLECTION: EMPATHY IN THE WORKPLACE Personal Reflection: Empathy In The Workplace. Just before I chaired a Board meeting last year, I spent a frustratingly painful hour going through many of the uncomfortable details of my divorce process and a set of emotional custody issues with my lawyers. Immediately after hanging up, with only minutes of transition, I put on my best poker NEW BIOTECH CORPORATE STRUCTURES: POSSIBLE ALTERNATIVES Not a biotech conference goes by these days without a discussion about new models for financing or exiting companies, and BioPharm America in Boston this week is no different. I’m on a panel discussing the topic on Wednesday afternoon. New BIOTECH STARTUPS AND THE HARD TRUTH OF INNOVATION Gary Pisano’s recent Harvard Business Review piece, The Hard Truth About Innovative Cultures, beautifully frames up how innovative corporate environments are frequently misunderstood.Innovative startups aren’t just about being cool and nimble, having beer taps in the kitchen, or an endless bounty of swag. Pisano sums up the harder, harsher reality of truly innovative ABOUT ME | LIFESCIVCLIFESCIVC About Bruce Booth. I’m an early stage venture capitalist. Like my partners at Atlas Venture, I enjoy working with great scientists and entrepreneurs to start new biotech companies. In short, we focus on seed-led venture creation around the discovery and development ofnovel therapeutics.

FIVE MACRO RISKS TO BIOTECH COMING OUT OF WASHINGTON Despite saving the world from COVID, pharma and biotech are still in the crosshairs of many politicians. With many anti-Pharma politicians and regulators emboldened in the current environment, and with more aggressive tax and spending policy in the works, there a number of risks to biotech over the next 1-2 years out of Washington. THE RECORD-BREAKING BIOTECH FUNDING TSUNAMI OF 1H2020 According to data from BMO Capital Markets, in aggregate, we’ve seen over $17.6B in equity funding in 2Q2020 into biopharma across both IPOs and follow-on’s (excluding offerings from Regeneron and Royalty Pharma). The biotech IPO fundraising level, in terms of capital raised, is the largest ever witnessed in a quarter, and the follow-on BIOTECH SCIENTIFIC ADVISORY BOARDS: WHAT WORKS, WHAT DOESN Cons – The real costs of a poorly used SAB. SABs don’t come for free . Good ones are a lot of work. And they are also costly for a startup in terms of dollars and equity. A typical SAB member may charge $2.5-5K per day and receive 0.1-0.3% equity. Hollywood-star advisors can be much, much more expensive than that on the equityfront.

LITTLE BY LITTLE: REAL LIFE LESSONS IN BUSINESS Little by Little: Real Life Lessons In Business Development. Posted April 16th, 2018 by Tariq Kassum, in Business Development, From The Trenches. This blog was written by Tariq Kassum, COO and Head of Corporate Development at Obsidian Therapeutics, as part of the From The Trenches feature of LifeSciVC. Experience can be a tough teacher. WHERE DOES ALL THAT BIOTECH VENTURE CAPITAL GO Venture capital investing in biotech has long been hard to disaggregate: how much goes to “early stage” vs “late stage”, how much goes to CNS vs oncology, discovery vs Phase 3, etc Today BIO’s David Thomas and Chad Wessel have SEVEN HABITS OF CELGENE’S HIGHLY SUCCESSFUL STRATEGY Seven Habits of Celgene’s Highly Successful Strategy. Over the past seven years, Celgene has emerged as one of the most active and creative deal-makers in the biopharma industry. The Boston Consulting Group’s Biopharma Partnering Survey and Benchmarking analysis examines BD activity and perceptions across the industry, and their2014

TALENT ACQUISITION: PHARMA IS THE LIFEBLOOD OF BIOTECH Talent Acquisition: Pharma Is The Lifeblood Of Biotech. Startup Biotechs need bigger drug companies for lots of things, including R&D collaborations, investments, non-dilutive funding, and eventual liquidity via M&A. The health of today’s ecosystem depends on biotech and pharma working together. But one of the most important andoften

BIOTECH CEO PAY: INFLATION HELD AT BAY Biotech CEO Pay: Inflation Held At Bay. The private biotech sector is awash in capital today: funding over the last few quarters has been record-breaking, up over 250% since 2013, as biotech CEOs have worked hard to strengthen their companies’ balance sheets. But in the process of filling up their corporate coffers, have they also filledup

RETURN OF THE JEDI: STROMEDIX ACQUIRED BY BIOGEN Return of the Jedi: Stromedix Acquired by Biogen. Biogen just announced its acquisition of Stromedix for up to $562M. Another solid M&A exit in biotech emphasizing how innovation matters. With a very different model than Avila Therapeutics, an exit we announced in January, Stromedix is a biology-focused, asset-centric companydedicated to

LIFESCIVC | BRUCE BOOTH, PARTNER AT ATLAS VENTURE, BLOGSBIOTECH FINANCINGVC-BACKED BIOTECH RETURNSBUSINESS DEVELOPMENTTALENT Despite saving the world from COVID, pharma and biotech are still in the crosshairs of many politicians. With many anti-Pharma politicians and regulators emboldened in the current environment, and with more aggressive tax and spending policy in the works, there a number of risks to biotech over the next 1-2 years out of Washington. THE BIOTECH JOB MARKET IS AS HOT AS THE HOUSING MARKET The biotech job market is a bit like the suburban housing market—red hot. It’s a buyer’s market, don’t waive your inspection rights! By Pamela L. Esposito, CBO of Replimune as part of the From The Trenches feature of LifeSciVC.. It is possibly the tightest biotechlabor

REIMAGINING THE WORKPLACE POST PANDEMIC In a recent Harvard Business Review report (Figure 2) virtually all respondents felt that workplace wellbeing had declined since the pandemic. This is no surprise, but interestingly, 56% noted that increased job demands were to blame in large part due to a loss of work-life separation. Only 24% of respondents noted feeling of lostconnection

SELECTIVE ALLOSTERIC TYK2 INHIBITORS Deucravacitinib is the first truly selective TYK2 inhibitor due to the fact that it targets the allosteric site. Due to improvements in the Nimbus chemical series, our TYK2 allosteric inhibitor extends these margins on JAK1, 2, and 3 even further. Until the BMS paper on deucravacitinib’s Phase 2b results in psoriasis ( NEJM, Sept 2018 ),the

BIOTECH STARTUPS AND THE HARD TRUTH OF INNOVATION Gary Pisano’s recent Harvard Business Review piece, The Hard Truth About Innovative Cultures, beautifully frames up how innovative corporate environments are frequently misunderstood.Innovative startups aren’t just about being cool and nimble, having beer taps in the kitchen, or an endless bounty of swag. Pisano sums up the harder, harsher reality of truly innovative BIOTECH SCIENTIFIC ADVISORY BOARDS: WHAT WORKS, WHAT DOESN Cons – The real costs of a poorly used SAB. SABs don’t come for free . Good ones are a lot of work. And they are also costly for a startup in terms of dollars and equity. A typical SAB member may charge $2.5-5K per day and receive 0.1-0.3% equity. Hollywood-star advisors can be much, much more expensive than that on the equityfront.

WHERE DOES ALL THAT BIOTECH VENTURE CAPITAL GO Venture capital investing in biotech has long been hard to disaggregate: how much goes to “early stage” vs “late stage”, how much goes to CNS vs oncology, discovery vs Phase 3, etc Today BIO’s David Thomas and Chad Wessel have BIOTECH VENTURE DEAL TERMS ARE MORE "STARTUP-FRIENDLY Biotech Venture Deal Terms Are More “Startup-Friendly” Than Ever. Posted September 10th, 2018 in Biotech financing, Fundraising. Biotech is booming, with eye-popping new financings seemingly announced daily. The sector is having an epic year for startup fundraising, breaking records for what will end up as the most active private biotech NEW BIOTECH CORPORATE STRUCTURES: POSSIBLE ALTERNATIVES Not a biotech conference goes by these days without a discussion about new models for financing or exiting companies, and BioPharm America in Boston this week is no different. I’m on a panel discussing the topic on Wednesday afternoon. New SEVEN HABITS OF CELGENE’S HIGHLY SUCCESSFUL STRATEGY Seven Habits of Celgene’s Highly Successful Strategy. Over the past seven years, Celgene has emerged as one of the most active and creative deal-makers in the biopharma industry. The Boston Consulting Group’s Biopharma Partnering Survey and Benchmarking analysis examines BD activity and perceptions across the industry, and their2014

LIFESCIVC | BRUCE BOOTH, PARTNER AT ATLAS VENTURE, BLOGSBIOTECH FINANCINGVC-BACKED BIOTECH RETURNSBUSINESS DEVELOPMENTTALENT Despite saving the world from COVID, pharma and biotech are still in the crosshairs of many politicians. With many anti-Pharma politicians and regulators emboldened in the current environment, and with more aggressive tax and spending policy in the works, there a number of risks to biotech over the next 1-2 years out of Washington. THE BIOTECH JOB MARKET IS AS HOT AS THE HOUSING MARKET The biotech job market is a bit like the suburban housing market—red hot. It’s a buyer’s market, don’t waive your inspection rights! By Pamela L. Esposito, CBO of Replimune as part of the From The Trenches feature of LifeSciVC.. It is possibly the tightest biotechlabor

REIMAGINING THE WORKPLACE POST PANDEMIC In a recent Harvard Business Review report (Figure 2) virtually all respondents felt that workplace wellbeing had declined since the pandemic. This is no surprise, but interestingly, 56% noted that increased job demands were to blame in large part due to a loss of work-life separation. Only 24% of respondents noted feeling of lostconnection

SELECTIVE ALLOSTERIC TYK2 INHIBITORS Deucravacitinib is the first truly selective TYK2 inhibitor due to the fact that it targets the allosteric site. Due to improvements in the Nimbus chemical series, our TYK2 allosteric inhibitor extends these margins on JAK1, 2, and 3 even further. Until the BMS paper on deucravacitinib’s Phase 2b results in psoriasis ( NEJM, Sept 2018 ),the

BIOTECH STARTUPS AND THE HARD TRUTH OF INNOVATION Gary Pisano’s recent Harvard Business Review piece, The Hard Truth About Innovative Cultures, beautifully frames up how innovative corporate environments are frequently misunderstood.Innovative startups aren’t just about being cool and nimble, having beer taps in the kitchen, or an endless bounty of swag. Pisano sums up the harder, harsher reality of truly innovative BIOTECH SCIENTIFIC ADVISORY BOARDS: WHAT WORKS, WHAT DOESN Cons – The real costs of a poorly used SAB. SABs don’t come for free . Good ones are a lot of work. And they are also costly for a startup in terms of dollars and equity. A typical SAB member may charge $2.5-5K per day and receive 0.1-0.3% equity. Hollywood-star advisors can be much, much more expensive than that on the equityfront.

WHERE DOES ALL THAT BIOTECH VENTURE CAPITAL GO Venture capital investing in biotech has long been hard to disaggregate: how much goes to “early stage” vs “late stage”, how much goes to CNS vs oncology, discovery vs Phase 3, etc Today BIO’s David Thomas and Chad Wessel have BIOTECH VENTURE DEAL TERMS ARE MORE "STARTUP-FRIENDLY Biotech Venture Deal Terms Are More “Startup-Friendly” Than Ever. Posted September 10th, 2018 in Biotech financing, Fundraising. Biotech is booming, with eye-popping new financings seemingly announced daily. The sector is having an epic year for startup fundraising, breaking records for what will end up as the most active private biotech NEW BIOTECH CORPORATE STRUCTURES: POSSIBLE ALTERNATIVES Not a biotech conference goes by these days without a discussion about new models for financing or exiting companies, and BioPharm America in Boston this week is no different. I’m on a panel discussing the topic on Wednesday afternoon. New SEVEN HABITS OF CELGENE’S HIGHLY SUCCESSFUL STRATEGY Seven Habits of Celgene’s Highly Successful Strategy. Over the past seven years, Celgene has emerged as one of the most active and creative deal-makers in the biopharma industry. The Boston Consulting Group’s Biopharma Partnering Survey and Benchmarking analysis examines BD activity and perceptions across the industry, and their2014

BIOTECH FUNDING TOPS THE CHARTS AGAIN Venture funding for US-based biopharma companies in 1Q 2021 topped the charts above $12B for the first time ever according to Pitchbook; amazingly, we’ve had 4 straight chart-topping quarters in a row. IPOs raised over $5B, making it one of the strongest quarters ever (#2 behind 3Q 2020). And public follow-on financings topped $11B, againone

THE RECORD-BREAKING BIOTECH FUNDING TSUNAMI OF 1H2020 According to data from BMO Capital Markets, in aggregate, we’ve seen over $17.6B in equity funding in 2Q2020 into biopharma across both IPOs and follow-on’s (excluding offerings from Regeneron and Royalty Pharma). The biotech IPO fundraising level, in terms of capital raised, is the largest ever witnessed in a quarter, and the follow-on THE BIOTECH PARADOX OF 2020: A YEAR IN REVIEW According to preliminary data from Pitchbook, over $26B of venture funding went into US-based biotech firms in 2020, with several quarters topping the charts for record-breaking funding ( the “tsunami” in the first half continued into the second half of the year). 2018 was the prior high, and only hit $19B. This impliesUS-based private

PERSONAL REFLECTION: EMPATHY IN THE WORKPLACE Personal Reflection: Empathy In The Workplace. Just before I chaired a Board meeting last year, I spent a frustratingly painful hour going through many of the uncomfortable details of my divorce process and a set of emotional custody issues with my lawyers. Immediately after hanging up, with only minutes of transition, I put on my best poker SEVEN HABITS OF CELGENE’S HIGHLY SUCCESSFUL STRATEGY Over the past seven years, Celgene has emerged as one of the most active and creative deal-makers in the biopharma industry. The Boston Consulting Group’s Biopharma Partnering Survey and Benchmarking analysis examines BD activity and perceptions across the industry, and their 2014 analysis was very telling. Celgene scored as the best partner on 78% of the partnering and culture metrics (7/9 OUR EXPERIENCE WITH FIRST-TIME BIOTECH CEOS: FIVE Of the 34 biotech companies, a whopping 82% had first-time CEOs. Further, only 26% of our CEOs had worked for prior Atlas companies; the vast majority were, by that definition, “new” relationships in the Atlas portfolio. Many of these were new introductions to our firm, often through referrals or via executive search processes. BIO COMES TO PHILADELPHIA, BIRTHPLACE OF U.S. INNOVATION BIO Comes To Philadelphia, Birthplace Of U.S. Innovation. This blog was written by Jeff Hatfield, CEO of Pennsylvania-based Vitae Pharmaceuticals, as part of the “From the Trenches” feature of LifeSciVC. Next week, BIO returns to Philadelphia for its massive annual convention, bringing together from around the world more than15,000 attendees.

SHOULD I STAY OR SHOULD I GO? BIG PHARMA EXECS TAKING THE You may have noticed that more and more seasoned pharma executives are making the move from big pharma or big biotech to lead small biotech companies. Jeff Jonas at Sage Therapeutics and Don Nicholson at Nimbus Discovery are great examples. The topic was covered a few months ago by LifeSciVC ( here) in relation to the importance of the big HIGH-PERFORMING BOARDS IN EARLY STAGE BIOTECH High-Performing Boards in Early Stage Biotech. Posted March 3rd, 2012 in Biotech startup advice, General Venture Capital. Having a highly functional and productive Board of Directors is a key ingredient for success for most companies, but its of particular importance for early stage startups. The web is full of advice around what are the RETURN OF THE JEDI: STROMEDIX ACQUIRED BY BIOGEN Return of the Jedi: Stromedix Acquired by Biogen. Biogen just announced its acquisition of Stromedix for up to $562M. Another solid M&A exit in biotech emphasizing how innovation matters. With a very different model than Avila Therapeutics, an exit we announced in January, Stromedix is a biology-focused, asset-centric companydedicated to

LIFESCIVC | BRUCE BOOTH, PARTNER AT ATLAS VENTURE, BLOGSBIOTECH FINANCINGVC-BACKED BIOTECH RETURNSBUSINESS DEVELOPMENTTALENT Despite saving the world from COVID, pharma and biotech are still in the crosshairs of many politicians. With many anti-Pharma politicians and regulators emboldened in the current environment, and with more aggressive tax and spending policy in the works, there a number of risks to biotech over the next 1-2 years out of Washington. THE BIOTECH JOB MARKET IS AS HOT AS THE HOUSING MARKET The biotech job market is a bit like the suburban housing market—red hot. It’s a buyer’s market, don’t waive your inspection rights! By Pamela L. Esposito, CBO of Replimune as part of the From The Trenches feature of LifeSciVC.. It is possibly the tightest biotechlabor

THE RECORD-BREAKING BIOTECH FUNDING TSUNAMI OF 1H2020 According to data from BMO Capital Markets, in aggregate, we’ve seen over $17.6B in equity funding in 2Q2020 into biopharma across both IPOs and follow-on’s (excluding offerings from Regeneron and Royalty Pharma). The biotech IPO fundraising level, in terms of capital raised, is the largest ever witnessed in a quarter, and the follow-on THE ELEPHANT IN THE ROOM The Elephant in the Room. By Philip Astley-Sparke, CEO of Replimune, as part of the From The Trenches feature of LifeSciVC. One of the biggest elephants in the room regarding starting and scaling young companies is the tension, often healthy but sometimes detrimental, that exist between CEOs and venture capital firms. NEW BIOTECH CORPORATE STRUCTURES: POSSIBLE ALTERNATIVES Not a biotech conference goes by these days without a discussion about new models for financing or exiting companies, and BioPharm America in Boston this week is no different. I’m on a panel discussing the topic on Wednesday afternoon. New BIOTECH SCIENTIFIC ADVISORY BOARDS: WHAT WORKS, WHAT DOESN Cons – The real costs of a poorly used SAB. SABs don’t come for free . Good ones are a lot of work. And they are also costly for a startup in terms of dollars and equity. A typical SAB member may charge $2.5-5K per day and receive 0.1-0.3% equity. Hollywood-star advisors can be much, much more expensive than that on the equityfront.

BIO COMES TO PHILADELPHIA, BIRTHPLACE OF U.S. INNOVATION BIO Comes To Philadelphia, Birthplace Of U.S. Innovation. This blog was written by Jeff Hatfield, CEO of Pennsylvania-based Vitae Pharmaceuticals, as part of the “From the Trenches” feature of LifeSciVC. Next week, BIO returns to Philadelphia for its massive annual convention, bringing together from around the world more than15,000 attendees.

SHOULD I STAY OR SHOULD I GO? BIG PHARMA EXECS TAKING THE You may have noticed that more and more seasoned pharma executives are making the move from big pharma or big biotech to lead small biotech companies. Jeff Jonas at Sage Therapeutics and Don Nicholson at Nimbus Discovery are great examples. The topic was covered a few months ago by LifeSciVC ( here) in relation to the importance of the big BIOTECH CEO PAY: INFLATION HELD AT BAY Biotech CEO Pay: Inflation Held At Bay. The private biotech sector is awash in capital today: funding over the last few quarters has been record-breaking, up over 250% since 2013, as biotech CEOs have worked hard to strengthen their companies’ balance sheets. But in the process of filling up their corporate coffers, have they also filledup

RETURN OF THE JEDI: STROMEDIX ACQUIRED BY BIOGEN Return of the Jedi: Stromedix Acquired by Biogen. Biogen just announced its acquisition of Stromedix for up to $562M. Another solid M&A exit in biotech emphasizing how innovation matters. With a very different model than Avila Therapeutics, an exit we announced in January, Stromedix is a biology-focused, asset-centric companydedicated to

LIFESCIVC | BRUCE BOOTH, PARTNER AT ATLAS VENTURE, BLOGSBIOTECH FINANCINGVC-BACKED BIOTECH RETURNSBUSINESS DEVELOPMENTTALENT Despite saving the world from COVID, pharma and biotech are still in the crosshairs of many politicians. With many anti-Pharma politicians and regulators emboldened in the current environment, and with more aggressive tax and spending policy in the works, there a number of risks to biotech over the next 1-2 years out of Washington. THE BIOTECH JOB MARKET IS AS HOT AS THE HOUSING MARKET The biotech job market is a bit like the suburban housing market—red hot. It’s a buyer’s market, don’t waive your inspection rights! By Pamela L. Esposito, CBO of Replimune as part of the From The Trenches feature of LifeSciVC.. It is possibly the tightest biotechlabor

THE RECORD-BREAKING BIOTECH FUNDING TSUNAMI OF 1H2020 According to data from BMO Capital Markets, in aggregate, we’ve seen over $17.6B in equity funding in 2Q2020 into biopharma across both IPOs and follow-on’s (excluding offerings from Regeneron and Royalty Pharma). The biotech IPO fundraising level, in terms of capital raised, is the largest ever witnessed in a quarter, and the follow-on THE ELEPHANT IN THE ROOM The Elephant in the Room. By Philip Astley-Sparke, CEO of Replimune, as part of the From The Trenches feature of LifeSciVC. One of the biggest elephants in the room regarding starting and scaling young companies is the tension, often healthy but sometimes detrimental, that exist between CEOs and venture capital firms. NEW BIOTECH CORPORATE STRUCTURES: POSSIBLE ALTERNATIVES Not a biotech conference goes by these days without a discussion about new models for financing or exiting companies, and BioPharm America in Boston this week is no different. I’m on a panel discussing the topic on Wednesday afternoon. New BIOTECH SCIENTIFIC ADVISORY BOARDS: WHAT WORKS, WHAT DOESN Cons – The real costs of a poorly used SAB. SABs don’t come for free . Good ones are a lot of work. And they are also costly for a startup in terms of dollars and equity. A typical SAB member may charge $2.5-5K per day and receive 0.1-0.3% equity. Hollywood-star advisors can be much, much more expensive than that on the equityfront.

BIO COMES TO PHILADELPHIA, BIRTHPLACE OF U.S. INNOVATION BIO Comes To Philadelphia, Birthplace Of U.S. Innovation. This blog was written by Jeff Hatfield, CEO of Pennsylvania-based Vitae Pharmaceuticals, as part of the “From the Trenches” feature of LifeSciVC. Next week, BIO returns to Philadelphia for its massive annual convention, bringing together from around the world more than15,000 attendees.

SHOULD I STAY OR SHOULD I GO? BIG PHARMA EXECS TAKING THE You may have noticed that more and more seasoned pharma executives are making the move from big pharma or big biotech to lead small biotech companies. Jeff Jonas at Sage Therapeutics and Don Nicholson at Nimbus Discovery are great examples. The topic was covered a few months ago by LifeSciVC ( here) in relation to the importance of the big BIOTECH CEO PAY: INFLATION HELD AT BAY Biotech CEO Pay: Inflation Held At Bay. The private biotech sector is awash in capital today: funding over the last few quarters has been record-breaking, up over 250% since 2013, as biotech CEOs have worked hard to strengthen their companies’ balance sheets. But in the process of filling up their corporate coffers, have they also filledup

RETURN OF THE JEDI: STROMEDIX ACQUIRED BY BIOGEN Return of the Jedi: Stromedix Acquired by Biogen. Biogen just announced its acquisition of Stromedix for up to $562M. Another solid M&A exit in biotech emphasizing how innovation matters. With a very different model than Avila Therapeutics, an exit we announced in January, Stromedix is a biology-focused, asset-centric companydedicated to

SELECTIVE ALLOSTERIC TYK2 INHIBITORS Deucravacitinib is the first truly selective TYK2 inhibitor due to the fact that it targets the allosteric site. Due to improvements in the Nimbus chemical series, our TYK2 allosteric inhibitor extends these margins on JAK1, 2, and 3 even further. Until the BMS paper on deucravacitinib’s Phase 2b results in psoriasis ( NEJM, Sept 2018 ),the

REIMAGINING THE WORKPLACE POST PANDEMIC In a recent Harvard Business Review report (Figure 2) virtually all respondents felt that workplace wellbeing had declined since the pandemic. This is no surprise, but interestingly, 56% noted that increased job demands were to blame in large part due to a loss of work-life separation. Only 24% of respondents noted feeling of lostconnection

THE ELEPHANT IN THE ROOM The Elephant in the Room. By Philip Astley-Sparke, CEO of Replimune, as part of the From The Trenches feature of LifeSciVC. One of the biggest elephants in the room regarding starting and scaling young companies is the tension, often healthy but sometimes detrimental, that exist between CEOs and venture capital firms. BIOTECH SCIENTIFIC ADVISORY BOARDS: WHAT WORKS, WHAT DOESN Cons – The real costs of a poorly used SAB. SABs don’t come for free . Good ones are a lot of work. And they are also costly for a startup in terms of dollars and equity. A typical SAB member may charge $2.5-5K per day and receive 0.1-0.3% equity. Hollywood-star advisors can be much, much more expensive than that on the equityfront.

BUILDING A BIOTECH: MAGENTA STARTS CHAPTER 2 WITH A TRIPLE Building A Biotech: Magenta Starts Chapter 2 With A Triple Play. This blog was written by Jason Gardner, CEO of Magenta Therapeutics and former EIR at Atlas Venture, as part of the From The Trenches feature of LifeSciVC. We are excited to open the first page of Chapter 2 at Magenta today. Since our public launch in November 2016, we have been BIOTECH STARTUPS AND THE HARD TRUTH OF INNOVATION Gary Pisano’s recent Harvard Business Review piece, The Hard Truth About Innovative Cultures, beautifully frames up how innovative corporate environments are frequently misunderstood.Innovative startups aren’t just about being cool and nimble, having beer taps in the kitchen, or an endless bounty of swag. Pisano sums up the harder, harsher reality of truly innovative TALENT ACQUISITION: PHARMA IS THE LIFEBLOOD OF BIOTECH Talent Acquisition: Pharma Is The Lifeblood Of Biotech. Startup Biotechs need bigger drug companies for lots of things, including R&D collaborations, investments, non-dilutive funding, and eventual liquidity via M&A. The health of today’s ecosystem depends on biotech and pharma working together. But one of the most important andoften

WHERE DOES ALL THAT BIOTECH VENTURE CAPITAL GO Venture capital investing in biotech has long been hard to disaggregate: how much goes to “early stage” vs “late stage”, how much goes to CNS vs oncology, discovery vs Phase 3, etc Today BIO’s David Thomas and Chad Wessel have OUR EXPERIENCE WITH FIRST-TIME BIOTECH CEOS: FIVE Of the 34 biotech companies, a whopping 82% had first-time CEOs. Further, only 26% of our CEOs had worked for prior Atlas companies; the vast majority were, by that definition, “new” relationships in the Atlas portfolio. Many of these were new introductions to our firm, often through referrals or via executive search processes. HIGH-PERFORMING BOARDS IN EARLY STAGE BIOTECH High-Performing Boards in Early Stage Biotech. Posted March 3rd, 2012 in Biotech startup advice, General Venture Capital. Having a highly functional and productive Board of Directors is a key ingredient for success for most companies, but its of particular importance for early stage startups. The web is full of advice around what are the LIFESCIVC | BRUCE BOOTH, PARTNER AT ATLAS VENTURE, BLOGSBIOTECH FINANCINGVC-BACKED BIOTECH RETURNSBUSINESS DEVELOPMENTTALENT Despite saving the world from COVID, pharma and biotech are still in the crosshairs of many politicians. With many anti-Pharma politicians and regulators emboldened in the current environment, and with more aggressive tax and spending policy in the works, there a number of risks to biotech over the next 1-2 years out of Washington. THE BIOTECH JOB MARKET IS AS HOT AS THE HOUSING MARKET The biotech job market is a bit like the suburban housing market—red hot. It’s a buyer’s market, don’t waive your inspection rights! By Pamela L. Esposito, CBO of Replimune as part of the From The Trenches feature of LifeSciVC.. It is possibly the tightest biotechlabor

THE RECORD-BREAKING BIOTECH FUNDING TSUNAMI OF 1H20202020 BIOTECHBEST SMALL BIOTECH IN 2020BIOTECH INVESTMENT 2020EMERGING BIOTECH COMPANIES 2020NEW BIOTECH COMPANIES 2020SMALL BIOTECH 2020 According to data from BMO Capital Markets, in aggregate, we’ve seen over $17.6B in equity funding in 2Q2020 into biopharma across both IPOs and follow-on’s (excluding offerings from Regeneron and Royalty Pharma). The biotech IPO fundraising level, in terms of capital raised, is the largest ever witnessed in a quarter, and the follow-on THE ELEPHANT IN THE ROOM The Elephant in the Room. By Philip Astley-Sparke, CEO of Replimune, as part of the From The Trenches feature of LifeSciVC. One of the biggest elephants in the room regarding starting and scaling young companies is the tension, often healthy but sometimes detrimental, that exist between CEOs and venture capital firms. NEW BIOTECH CORPORATE STRUCTURES: POSSIBLE ALTERNATIVES Not a biotech conference goes by these days without a discussion about new models for financing or exiting companies, and BioPharm America in Boston this week is no different. I’m on a panel discussing the topic on Wednesday afternoon. New BIOTECH SCIENTIFIC ADVISORY BOARDS: WHAT WORKS, WHAT DOESN Cons – The real costs of a poorly used SAB. SABs don’t come for free . Good ones are a lot of work. And they are also costly for a startup in terms of dollars and equity. A typical SAB member may charge $2.5-5K per day and receive 0.1-0.3% equity. Hollywood-star advisors can be much, much more expensive than that on the equityfront.

BIO COMES TO PHILADELPHIA, BIRTHPLACE OF U.S. INNOVATION BIO Comes To Philadelphia, Birthplace Of U.S. Innovation. This blog was written by Jeff Hatfield, CEO of Pennsylvania-based Vitae Pharmaceuticals, as part of the “From the Trenches” feature of LifeSciVC. Next week, BIO returns to Philadelphia for its massive annual convention, bringing together from around the world more than15,000 attendees.

SHOULD I STAY OR SHOULD I GO? BIG PHARMA EXECS TAKING THE You may have noticed that more and more seasoned pharma executives are making the move from big pharma or big biotech to lead small biotech companies. Jeff Jonas at Sage Therapeutics and Don Nicholson at Nimbus Discovery are great examples. The topic was covered a few months ago by LifeSciVC ( here) in relation to the importance of the big BIOTECH CEO PAY: INFLATION HELD AT BAY Biotech CEO Pay: Inflation Held At Bay. The private biotech sector is awash in capital today: funding over the last few quarters has been record-breaking, up over 250% since 2013, as biotech CEOs have worked hard to strengthen their companies’ balance sheets. But in the process of filling up their corporate coffers, have they also filledup

RETURN OF THE JEDI: STROMEDIX ACQUIRED BY BIOGEN Return of the Jedi: Stromedix Acquired by Biogen. Biogen just announced its acquisition of Stromedix for up to $562M. Another solid M&A exit in biotech emphasizing how innovation matters. With a very different model than Avila Therapeutics, an exit we announced in January, Stromedix is a biology-focused, asset-centric companydedicated to

LIFESCIVC | BRUCE BOOTH, PARTNER AT ATLAS VENTURE, BLOGSBIOTECH FINANCINGVC-BACKED BIOTECH RETURNSBUSINESS DEVELOPMENTTALENT Despite saving the world from COVID, pharma and biotech are still in the crosshairs of many politicians. With many anti-Pharma politicians and regulators emboldened in the current environment, and with more aggressive tax and spending policy in the works, there a number of risks to biotech over the next 1-2 years out of Washington. THE BIOTECH JOB MARKET IS AS HOT AS THE HOUSING MARKET The biotech job market is a bit like the suburban housing market—red hot. It’s a buyer’s market, don’t waive your inspection rights! By Pamela L. Esposito, CBO of Replimune as part of the From The Trenches feature of LifeSciVC.. It is possibly the tightest biotechlabor

THE RECORD-BREAKING BIOTECH FUNDING TSUNAMI OF 1H20202020 BIOTECHBEST SMALL BIOTECH IN 2020BIOTECH INVESTMENT 2020EMERGING BIOTECH COMPANIES 2020NEW BIOTECH COMPANIES 2020SMALL BIOTECH 2020 According to data from BMO Capital Markets, in aggregate, we’ve seen over $17.6B in equity funding in 2Q2020 into biopharma across both IPOs and follow-on’s (excluding offerings from Regeneron and Royalty Pharma). The biotech IPO fundraising level, in terms of capital raised, is the largest ever witnessed in a quarter, and the follow-on THE ELEPHANT IN THE ROOM The Elephant in the Room. By Philip Astley-Sparke, CEO of Replimune, as part of the From The Trenches feature of LifeSciVC. One of the biggest elephants in the room regarding starting and scaling young companies is the tension, often healthy but sometimes detrimental, that exist between CEOs and venture capital firms. NEW BIOTECH CORPORATE STRUCTURES: POSSIBLE ALTERNATIVES Not a biotech conference goes by these days without a discussion about new models for financing or exiting companies, and BioPharm America in Boston this week is no different. I’m on a panel discussing the topic on Wednesday afternoon. New BIOTECH SCIENTIFIC ADVISORY BOARDS: WHAT WORKS, WHAT DOESN Cons – The real costs of a poorly used SAB. SABs don’t come for free . Good ones are a lot of work. And they are also costly for a startup in terms of dollars and equity. A typical SAB member may charge $2.5-5K per day and receive 0.1-0.3% equity. Hollywood-star advisors can be much, much more expensive than that on the equityfront.

BIO COMES TO PHILADELPHIA, BIRTHPLACE OF U.S. INNOVATION BIO Comes To Philadelphia, Birthplace Of U.S. Innovation. This blog was written by Jeff Hatfield, CEO of Pennsylvania-based Vitae Pharmaceuticals, as part of the “From the Trenches” feature of LifeSciVC. Next week, BIO returns to Philadelphia for its massive annual convention, bringing together from around the world more than15,000 attendees.

SHOULD I STAY OR SHOULD I GO? BIG PHARMA EXECS TAKING THE You may have noticed that more and more seasoned pharma executives are making the move from big pharma or big biotech to lead small biotech companies. Jeff Jonas at Sage Therapeutics and Don Nicholson at Nimbus Discovery are great examples. The topic was covered a few months ago by LifeSciVC ( here) in relation to the importance of the big BIOTECH CEO PAY: INFLATION HELD AT BAY Biotech CEO Pay: Inflation Held At Bay. The private biotech sector is awash in capital today: funding over the last few quarters has been record-breaking, up over 250% since 2013, as biotech CEOs have worked hard to strengthen their companies’ balance sheets. But in the process of filling up their corporate coffers, have they also filledup

RETURN OF THE JEDI: STROMEDIX ACQUIRED BY BIOGEN Return of the Jedi: Stromedix Acquired by Biogen. Biogen just announced its acquisition of Stromedix for up to $562M. Another solid M&A exit in biotech emphasizing how innovation matters. With a very different model than Avila Therapeutics, an exit we announced in January, Stromedix is a biology-focused, asset-centric companydedicated to

SELECTIVE ALLOSTERIC TYK2 INHIBITORS Deucravacitinib is the first truly selective TYK2 inhibitor due to the fact that it targets the allosteric site. Due to improvements in the Nimbus chemical series, our TYK2 allosteric inhibitor extends these margins on JAK1, 2, and 3 even further. Until the BMS paper on deucravacitinib’s Phase 2b results in psoriasis ( NEJM, Sept 2018 ),the

REIMAGINING THE WORKPLACE POST PANDEMIC In a recent Harvard Business Review report (Figure 2) virtually all respondents felt that workplace wellbeing had declined since the pandemic. This is no surprise, but interestingly, 56% noted that increased job demands were to blame in large part due to a loss of work-life separation. Only 24% of respondents noted feeling of lostconnection

THE ELEPHANT IN THE ROOM The Elephant in the Room. By Philip Astley-Sparke, CEO of Replimune, as part of the From The Trenches feature of LifeSciVC. One of the biggest elephants in the room regarding starting and scaling young companies is the tension, often healthy but sometimes detrimental, that exist between CEOs and venture capital firms. BIOTECH SCIENTIFIC ADVISORY BOARDS: WHAT WORKS, WHAT DOESN Cons – The real costs of a poorly used SAB. SABs don’t come for free . Good ones are a lot of work. And they are also costly for a startup in terms of dollars and equity. A typical SAB member may charge $2.5-5K per day and receive 0.1-0.3% equity. Hollywood-star advisors can be much, much more expensive than that on the equityfront.

BUILDING A BIOTECH: MAGENTA STARTS CHAPTER 2 WITH A TRIPLE Building A Biotech: Magenta Starts Chapter 2 With A Triple Play. This blog was written by Jason Gardner, CEO of Magenta Therapeutics and former EIR at Atlas Venture, as part of the From The Trenches feature of LifeSciVC. We are excited to open the first page of Chapter 2 at Magenta today. Since our public launch in November 2016, we have been BIOTECH STARTUPS AND THE HARD TRUTH OF INNOVATION Gary Pisano’s recent Harvard Business Review piece, The Hard Truth About Innovative Cultures, beautifully frames up how innovative corporate environments are frequently misunderstood.Innovative startups aren’t just about being cool and nimble, having beer taps in the kitchen, or an endless bounty of swag. Pisano sums up the harder, harsher reality of truly innovative TALENT ACQUISITION: PHARMA IS THE LIFEBLOOD OF BIOTECH Talent Acquisition: Pharma Is The Lifeblood Of Biotech. Startup Biotechs need bigger drug companies for lots of things, including R&D collaborations, investments, non-dilutive funding, and eventual liquidity via M&A. The health of today’s ecosystem depends on biotech and pharma working together. But one of the most important andoften

WHERE DOES ALL THAT BIOTECH VENTURE CAPITAL GO Venture capital investing in biotech has long been hard to disaggregate: how much goes to “early stage” vs “late stage”, how much goes to CNS vs oncology, discovery vs Phase 3, etc Today BIO’s David Thomas and Chad Wessel have OUR EXPERIENCE WITH FIRST-TIME BIOTECH CEOS: FIVE Of the 34 biotech companies, a whopping 82% had first-time CEOs. Further, only 26% of our CEOs had worked for prior Atlas companies; the vast majority were, by that definition, “new” relationships in the Atlas portfolio. Many of these were new introductions to our firm, often through referrals or via executive search processes. HIGH-PERFORMING BOARDS IN EARLY STAGE BIOTECH High-Performing Boards in Early Stage Biotech. Posted March 3rd, 2012 in Biotech startup advice, General Venture Capital. Having a highly functional and productive Board of Directors is a key ingredient for success for most companies, but its of particular importance for early stage startups. The web is full of advice around what are the Blog About Me From The Trenches Recovering scientist turned early stage VC A biotech optimist fightinggravity

*

*

*

*

BIOTECH’S RELEVANCY CHALLENGE IN AN EXPANDING UNIVERSE Posted June 1st, 2021 in Biotech financing, Capital markets

| 0 Comments

Twitter Facebook LinkedIn Redditplayers.

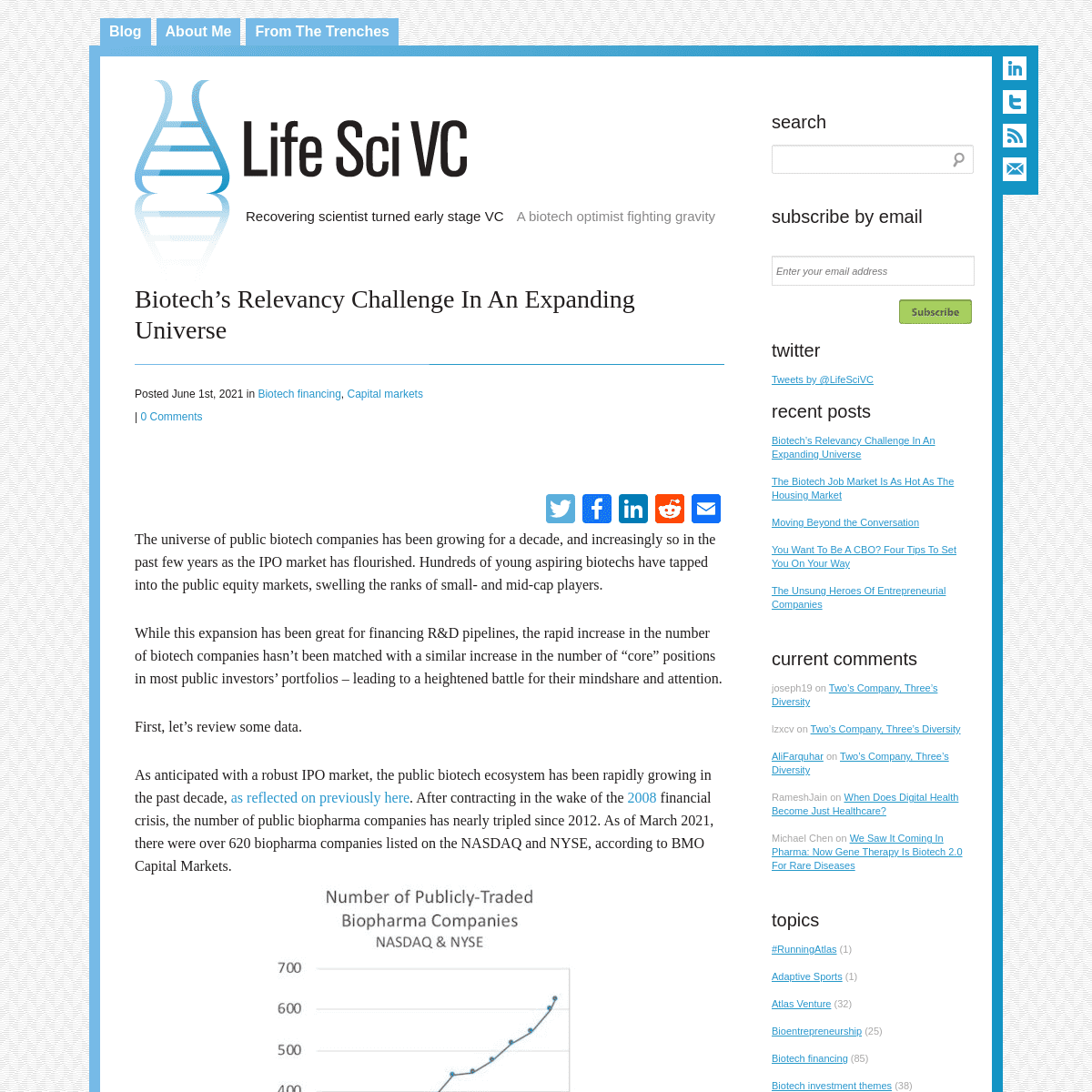

While this expansion has been great for financing R&D pipelines, the rapid increase in the number of biotech companies hasn’t been matched with a similar increase in the number of “core” positions in most public investors’ portfolios – leading to a heightened battle for their mindshare and attention. First, let’s review some data. As anticipated with a robust IPO market, the public biotech ecosystem has been rapidly growing in the past decade, as reflected onpreviously here

.

After contracting in the wake of the 2008 financial crisis, the number of public biopharma companies has nearly tripled since 2012. As of March 2021, there were over 620 biopharma companies listed on the NASDAQ and NYSE, according to BMO CapitalMarkets.

However, the number of biotech-savvy buyside investors hasn’t kept pace with the number of newly public biotech stocks. While anecdotally there’ve been a reasonable number of new funds formed, these haven’t launched at the same pace as new IPOs or the growth of the biotech markets as a whole in recent years. In fact, as explained below, data suggest that many of the bigger and more established public biotech funds have actually grown faster than the overallmarket.

Though metrics of public equity fund formation and activity in biotech are hard to track, there are a few proxy data points that shed some light. Investor positions for any fund with at least $100M in AUM can be tracked by what the SEC calls 13F filings. As background, the number of 13F filings scales with the valuation of companies in a linear way; a newly minted IPO may have 60-120 investors that are required to file 13Fs, which typically grows into 500-800 filers if the company is fortunate enough to get into the $10B market cap range, and Big Pharma’s often have more than 2000 filers. If the pace of fund formation for new investment managers was growing faster than the number of investment opportunities, you’d expect to see the growth rate of the AUM of a stable pool of existing blue chip biotech specialists to trail the growth of the overall biotech market (implying their “market share” was going down as new managers appeared). This hasn’t been the case. Examining the 13F filings of a sample of ten of the most active crossover/biotech specialists (including Baker Brothers, OrbiMed, Perceptive, Red Mile, RA, RTW, Deerfield, Rock Springs, BVF, and EcoR1) across the 7 quarters, from 1Q 2019 and 4Q 2020, reveals an aggregate value increase from $40B to $83B, or a 108% increase. Some of this is by accretive performance of their portfolio positions, some by net inflows into their funds.By

comparison, total biotech financing activity (in dollar terms) for IPOs and public follow-on’s grew 86% over that period (1Q19 vs 4Q20), and the $XBI biotech stock market index increased 76% over that period (3/31/19 to 12/31/20). This delta (108% vs 70-86%) implies that despite the arrival of new managers, many of the bigger and more established managers are increasing, not decreasing, in their aggregate share of the biotech investing/funding market. One of the many limitations of this analysis is it doesn’t capture differences in “where” investors play in the continuum of biotech companies, i.e., buying an IPO is different than buying Alnylam today, and some investors do more of the latter than the former. If anyone has better data on fund formation and activity, please share. That said, I think the analysis is directionally correct around the principle takeaway: THE PACE OF NEW NAMES TO INVEST IN (SUPPLY OF OPPORTUNITIES) HAS INCREASED FASTER THAN THE NUMBER OF POTENTIAL “BIG” HOLDERS OF THOSE NAMES (DEMAND FOR CORE POSITIONS). Fund managers are frequently constrained by the number of true “core” positions they have, due to both mindshare of their team and the need for meaningfully-sized portfolio allocations. Setting aside the huge long-only mutual funds (like Fidelity) that own large swaths of the biotech market, many of the best buyside investors in the biotech investing world only have 20-30 “core” positions, along with a tail of smaller “toe-hold” positions, irrespective of their fund’s assets under management (AUM). Given the illiquidity of many biotech names, these big core positions only typically accrue by participating in marketed or structured biotech financings (e.g., crossover private rounds, IPOs, and Follow-On offerings). Buying these big “core” positions only in the open market would put significant upward pressure on the stock prices for most SMid-cap companies. For an aspiring young biotech to build a successful and supportive investor base for the long-term almost requires becoming a core position with at least a few of the “blue chip” buyside investors. These funds often step-up in every financing with significant anchor orders, and they support the stock on the inevitable volatility dips. As an example, Baker Brothers did this with Synagevaand Seagen

over the past decade, buying into their equity financings as supportive insiders with strong conviction. But the number of core positions “available” in the industry only scales with the number of skilled and size-able investors, since most funds generally don’t have big positions beyond their core 20-30 names. Despite increasing in size (as shown in the data above), most of the top funds haven’t scaled by adding a proportional number of new “core” names. In short, their core portfolios have increased in valuation, rather than in the number of underlying stocks. This is part of what has driven the feed-forward flywheel of crossover and IPO sizes and valuations: larger raises mean larger allocations that are more meaningful for funds, driving up demand for participation in those raises, which increases the valuation and enables ever-larger raises – and so the positive cycle feeds itself. There are two ways for a fund to make room for new “core” positions. They can sell out of a position, believing their capital is better deployed elsewhere (due to either valuation levels or a loss of conviction on the biotech’s prospects). This trading obviously happens, and many observers track the 13F filing changes of the top funds (like this one, tracking EcoR1).

Or, a fund’s core position could be cashed out because of M&A. An acquisition recycles cash back into the fund for redeployment into new names. Over the past year, though, M&A has been rather quiet relative to past bull periods in this 10+ year super-cycle, reducing the relative role of recycling in fund-level portfolio reallocations oflate.

So all these trends highlight the “RELEVANCY CHALLENGE” IN THE BIOTECH EQUITY CAPITAL MARKETS TODAY: in an ever-expanding world of names, where the “supply” of possible core positions is outstripping “demand” for additional core positions, how does a biotech become or maintain relevance to the best long-term investors? The obvious answer is to have an unusually compelling story to tell with great data revealing huge potential for transformative impact on patients. Much easier to say then to truly demonstrate, and “compelling” for an early stage story is often in the eye of thebeholder.

But beyond the obvious, there are a number of things that can beimportant.