2

More Annotations

5

5

Favourite Annotations

4

5

Text

FREE COMMERCIAL LOAN BROKER TRAINING I have trained over 10,000 practicing commercial mortgage brokers, and I have earned close to $1 million in training fees. But you don't have to pay me one red cent to spy on my training lessons to my sons. You'll learn about the new Debt Yield Ratio, and why life companies

and conduits are

FINANCING OF LAND LEASES What is a land lease? A land lease happens when a land owner refuses to part with title to a piece of ground, but he is willing to lease out the use of the land for a very long period of time. Typically the land is unimproved, and the land lessee - the guy leasing the property - proceeds to construct a new building on the property.. Land leases can have any term, but two common lease terms are DEBT RATIO AND COMMERCIAL LOANS The Top Debt Ratio: The Top Debt Ratio is used to make sure that the borrower is not trying to make payments on a personal residence that is too much house for him. It is defined as follows: Top Debt Ratio = First and Second Mortgage Payments / Gross Income. Experience has repeatedly shown that whenever a borrower spends more than 25% to 28%of

HOW TO PREPARE A PRO FORMA OPERATING STATEMENT FOR AN The number you should use for Property Management is 5% of Effective Gross Income; i.e., that number in your pro forma left over after you take off 5% Reserve for Vacancy and Collection Loss. If you try to use 4% of Effective Gross Income, the lender will likely punish you anduse 6% to 8%.

EB-5 COMMERCIAL LOANS AND THE EB-5 PROGRAM The entire process of EB-5 funding is a program developed by the United States Citizenship Immigration Service (USCIS) known as EB-5 Pilot program. USCIS is a division of Homeland Security. The EB-5 process can offer foreign immigrants a fast track path to obtaining US Visas for their "entire family". Simply said, by investing $545,000into an

NEW CONSTRUCTION IS DOOMED AS BANKS STOP MAKING 2,500 For Just $79.95. The reason why is because the banks have stopped making new commercial construction loans. Banks are terrified right now, and the first thing that banks do when they get scared is to stop all commercial real estate lending. This lending freeze is especially true of commercial construction loans. WHAT IS A HVCRE LOAN? In plain English, this means that a loan made by a bank to finance the purchase of commercial land - including the future site of a multifamily project or a residential subdivision - is considered a HVCRE loan. An A&D loan is another example of a HVCRE loan. An acquisition and development (A&D) loan is a loan used to buy a pieceof raw land

COMMERCIAL LOANS AND THE MEANING OF "LAST DOLLAR" The term is used most often when mezzanine loans or preferred equity investments are stacked on top of very large permanent loans. The permanent lender's last dollar is 60% LTV, the mezzanine lender's last dollar is 75% LTV, and the preferred equity provider's last LICENSING FOR COMMERCIAL LOAN BROKERS Licensing for Commercial Loan Brokers. Most states in America do not require a commercial mortgage broker to obtain a mortgage broker's license or a real estate broker's license in order to negotiate commercial mortgage loans in their state. This fact, however, is oftennot obvious.

COMMERCIAL LOANS AND BURN-OFF'S This commercial loan is now a non-recourse loan. My thanks go out to David Repka of Bison Financial Group for this clear explanation. David is looking for commercial construction loans of over $10 million and can be reached at 727-537-0330. Commercial loan FREE COMMERCIAL LOAN BROKER TRAINING I have trained over 10,000 practicing commercial mortgage brokers, and I have earned close to $1 million in training fees. But you don't have to pay me one red cent to spy on my training lessons to my sons. You'll learn about the new Debt Yield Ratio, and why life companiesand conduits are

FINANCING OF LAND LEASES What is a land lease? A land lease happens when a land owner refuses to part with title to a piece of ground, but he is willing to lease out the use of the land for a very long period of time. Typically the land is unimproved, and the land lessee - the guy leasing the property - proceeds to construct a new building on the property.. Land leases can have any term, but two common lease terms are DEBT RATIO AND COMMERCIAL LOANS The Top Debt Ratio: The Top Debt Ratio is used to make sure that the borrower is not trying to make payments on a personal residence that is too much house for him. It is defined as follows: Top Debt Ratio = First and Second Mortgage Payments / Gross Income. Experience has repeatedly shown that whenever a borrower spends more than 25% to 28%of

HOW TO PREPARE A PRO FORMA OPERATING STATEMENT FOR AN The number you should use for Property Management is 5% of Effective Gross Income; i.e., that number in your pro forma left over after you take off 5% Reserve for Vacancy and Collection Loss. If you try to use 4% of Effective Gross Income, the lender will likely punish you anduse 6% to 8%.

EB-5 COMMERCIAL LOANS AND THE EB-5 PROGRAM The entire process of EB-5 funding is a program developed by the United States Citizenship Immigration Service (USCIS) known as EB-5 Pilot program. USCIS is a division of Homeland Security. The EB-5 process can offer foreign immigrants a fast track path to obtaining US Visas for their "entire family". Simply said, by investing $545,000into an

NEW CONSTRUCTION IS DOOMED AS BANKS STOP MAKING 2,500 For Just $79.95. The reason why is because the banks have stopped making new commercial construction loans. Banks are terrified right now, and the first thing that banks do when they get scared is to stop all commercial real estate lending. This lending freeze is especially true of commercial construction loans. WHAT IS A HVCRE LOAN? In plain English, this means that a loan made by a bank to finance the purchase of commercial land - including the future site of a multifamily project or a residential subdivision - is considered a HVCRE loan. An A&D loan is another example of a HVCRE loan. An acquisition and development (A&D) loan is a loan used to buy a pieceof raw land

COMMERCIAL LOANS AND THE MEANING OF "LAST DOLLAR" The term is used most often when mezzanine loans or preferred equity investments are stacked on top of very large permanent loans. The permanent lender's last dollar is 60% LTV, the mezzanine lender's last dollar is 75% LTV, and the preferred equity provider's last LICENSING FOR COMMERCIAL LOAN BROKERS Licensing for Commercial Loan Brokers. Most states in America do not require a commercial mortgage broker to obtain a mortgage broker's license or a real estate broker's license in order to negotiate commercial mortgage loans in their state. This fact, however, is oftennot obvious.

COMMERCIAL LOANS AND BURN-OFF'S This commercial loan is now a non-recourse loan. My thanks go out to David Repka of Bison Financial Group for this clear explanation. David is looking for commercial construction loans of over $10 million and can be reached at 727-537-0330. Commercial loan ACQUISITION AND DEVELOPMENT LOANS Acquisition and Development Loans. A land development loan is an advance of funds, secured by a mortgage, to finance the making, installing, or constructing of the improvements necessary to convert raw land into construction-ready building sites. In other words, a land development loan takes an unimproved parcel and breaks it up into a number of smaller, improved parcels upon which homes or FINANCING OF LAND LEASES What is a land lease? A land lease happens when a land owner refuses to part with title to a piece of ground, but he is willing to lease out the use of the land for a very long period of time. Typically the land is unimproved, and the land lessee - the guy leasing the property - proceeds to construct a new building on the property.. Land leases can have any term, but two common lease terms are COMMERCIAL LOAN APPLICATION C-LOANS LITE AN EASIER COMMERCIAL LOAN APPLICATION Just Complete This One Page Form. C-Loans, Inc. will then electronically submit your commercial loan application to several dozen commercial lenders, each carefully selected from our list of 750 participating banks.BRIDGE LOANS

Bridge Loans. A bridge loan is defined as a short-term real estate loan that gives the property owner time to complete some task - such as improving the property, finding a new tenant and/or selling the property. The typical commercial property bridge loan has a term of one to two years, although many commercial bridge loan lenders will grant the owner the option to extend his loan for sixDEBT YIELD RATIO

Debt Yield Ratio. The Debt Yield Ratio is defined as the Net Operating Income (NOI) divided by the first mortgage debt (loan) amount, times 100%. For example, let's say that a commercial property has a NOI of $437,000 per year, and some conduit lender has been asked to make a new first mortgage loan in the amount of $6,000,000. HOW TO PREPARE A PRO FORMA OPERATING STATEMENT FOR AN This is the most important line in any apartment pro forma because so many deal-killing mistakes are made here. You need to make sure that this top-line number as large as possible because a great many apartment lenders will determine the maximum size of your loan by seizing this number, taking off 5% for vacancy and 35% or 40% for expenses, and then plugging this resultant net operating WHAT IS A HVCRE LOAN? In plain English, this means that a loan made by a bank to finance the purchase of commercial land - including the future site of a multifamily project or a residential subdivision - is considered a HVCRE loan. An A&D loan is another example of a HVCRE loan. An acquisition and development (A&D) loan is a loan used to buy a pieceof raw land

COMMERCIAL CONSTRUCTION LOANS AND SOFT COSTS Construction Loans > Commercial Construction Loans and Soft Costs. Commercial Construction Loans and Soft Costs. Soft Costs Are the Non-Brick and Mortar Expenses . When underwriting a commercial construction loan, ther are four major categories of costs: the land cost, the hard costs, the soft costs, and the contingency reservereserve.

COMMERCIAL LOANS AND TIC ROLL-UPS A tenancy-in-common investment ("TIC" or "TIC Investment") is an investment by a taxpayer in real estate which is co-owned with other investors. Since the taxpayer holds title to the real estate as a tenant-in-common, TIC investments qualify under the like-kind rules of �1031. In other words, if the 67-year-old owner of a big apartment DEBT YIELDS ON CMBS APARTMENT LOANS You will recall that the Debt Yield Ratio is different from the Debt Service Coverage Ratio.They are two completely different ratios. The Debt Yield Ratio is defined as the Net Operating Income (NOI) divided by the first mortgage debt (loan) amount, times 100%.. For example, let's say that a commercial property has a NOI of $437,000 per year, and some conduit lender has been asked toCOMMERCIAL LOANS

The rate is tied to prime, with a margin of 1.5% to 2.75%. Almost all SBA loans are closed at 2.75% over prime. Your deal would have to be pretty awesome to qualify for a margin of only 1.5%. Commercial construction loans are typically priced at prime + 1% to 1.5% FINANCING OF LAND LEASES What is a land lease? A land lease happens when a land owner refuses to part with title to a piece of ground, but he is willing to lease out the use of the land for a very long period of time. Typically the land is unimproved, and the land lessee - the guy leasing the property - proceeds to construct a new building on the property.. Land leases can have any term, but two common lease terms are HOW TO UNDERWRITE COMMERCIAL LOANS C-Loans.com® is sponsored by C-Loans®, Inc.. For help with the operation of the software ONLY, please contact Tom Blackburne, Software Technical Advisor.Mobile phone: (574) 210-6686. 555 University Avenue, Suite 150, Sacramento, CA 95825 telephone: (916) 338-3232 * Fax: (916) 338-2328 FREE COMMERCIAL LOAN BROKER TRAINING I have trained over 10,000 practicing commercial mortgage brokers, and I have earned close to $1 million in training fees. But you don't have to pay me one red cent to spy on my training lessons to my sons. You'll learn about the new Debt Yield Ratio, and why life companiesand conduits are

DEBT RATIO AND COMMERCIAL LOANS The Top Debt Ratio: The Top Debt Ratio is used to make sure that the borrower is not trying to make payments on a personal residence that is too much house for him. It is defined as follows: Top Debt Ratio = First and Second Mortgage Payments / Gross Income. Experience has repeatedly shown that whenever a borrower spends more than 25% to 28%of

HOW TO PREPARE A PRO FORMA OPERATING STATEMENT FOR AN The number you should use for Property Management is 5% of Effective Gross Income; i.e., that number in your pro forma left over after you take off 5% Reserve for Vacancy and Collection Loss. If you try to use 4% of Effective Gross Income, the lender will likely punish you anduse 6% to 8%.

NEW CONSTRUCTION IS DOOMED AS BANKS STOP MAKING 2,500 For Just $79.95. The reason why is because the banks have stopped making new commercial construction loans. Banks are terrified right now, and the first thing that banks do when they get scared is to stop all commercial real estate lending. This lending freeze is especially true of commercial construction loans. DEBT YIELDS ON CMBS APARTMENT LOANS You will recall that the Debt Yield Ratio is different from the Debt Service Coverage Ratio.They are two completely different ratios. The Debt Yield Ratio is defined as the Net Operating Income (NOI) divided by the first mortgage debt (loan) amount, times 100%.. For example, let's say that a commercial property has a NOI of $437,000 per year, and some conduit lender has been asked to COMMERCIAL LOANS AND THE MEANING OF "LAST DOLLAR" The term is used most often when mezzanine loans or preferred equity investments are stacked on top of very large permanent loans. The permanent lender's last dollar is 60% LTV, the mezzanine lender's last dollar is 75% LTV, and the preferred equity provider's last COMMERCIAL LOANS AND BURN-OFF'S This commercial loan is now a non-recourse loan. My thanks go out to David Repka of Bison Financial Group for this clear explanation. David is looking for commercial construction loans of over $10 million and can be reached at 727-537-0330. Commercial loanCOMMERCIAL LOANS

The rate is tied to prime, with a margin of 1.5% to 2.75%. Almost all SBA loans are closed at 2.75% over prime. Your deal would have to be pretty awesome to qualify for a margin of only 1.5%. Commercial construction loans are typically priced at prime + 1% to 1.5% FINANCING OF LAND LEASES What is a land lease? A land lease happens when a land owner refuses to part with title to a piece of ground, but he is willing to lease out the use of the land for a very long period of time. Typically the land is unimproved, and the land lessee - the guy leasing the property - proceeds to construct a new building on the property.. Land leases can have any term, but two common lease terms are HOW TO UNDERWRITE COMMERCIAL LOANS C-Loans.com® is sponsored by C-Loans®, Inc.. For help with the operation of the software ONLY, please contact Tom Blackburne, Software Technical Advisor.Mobile phone: (574) 210-6686. 555 University Avenue, Suite 150, Sacramento, CA 95825 telephone: (916) 338-3232 * Fax: (916) 338-2328 FREE COMMERCIAL LOAN BROKER TRAINING I have trained over 10,000 practicing commercial mortgage brokers, and I have earned close to $1 million in training fees. But you don't have to pay me one red cent to spy on my training lessons to my sons. You'll learn about the new Debt Yield Ratio, and why life companiesand conduits are

DEBT RATIO AND COMMERCIAL LOANS The Top Debt Ratio: The Top Debt Ratio is used to make sure that the borrower is not trying to make payments on a personal residence that is too much house for him. It is defined as follows: Top Debt Ratio = First and Second Mortgage Payments / Gross Income. Experience has repeatedly shown that whenever a borrower spends more than 25% to 28%of

HOW TO PREPARE A PRO FORMA OPERATING STATEMENT FOR AN The number you should use for Property Management is 5% of Effective Gross Income; i.e., that number in your pro forma left over after you take off 5% Reserve for Vacancy and Collection Loss. If you try to use 4% of Effective Gross Income, the lender will likely punish you anduse 6% to 8%.

NEW CONSTRUCTION IS DOOMED AS BANKS STOP MAKING 2,500 For Just $79.95. The reason why is because the banks have stopped making new commercial construction loans. Banks are terrified right now, and the first thing that banks do when they get scared is to stop all commercial real estate lending. This lending freeze is especially true of commercial construction loans. DEBT YIELDS ON CMBS APARTMENT LOANS You will recall that the Debt Yield Ratio is different from the Debt Service Coverage Ratio.They are two completely different ratios. The Debt Yield Ratio is defined as the Net Operating Income (NOI) divided by the first mortgage debt (loan) amount, times 100%.. For example, let's say that a commercial property has a NOI of $437,000 per year, and some conduit lender has been asked to COMMERCIAL LOANS AND THE MEANING OF "LAST DOLLAR" The term is used most often when mezzanine loans or preferred equity investments are stacked on top of very large permanent loans. The permanent lender's last dollar is 60% LTV, the mezzanine lender's last dollar is 75% LTV, and the preferred equity provider's last COMMERCIAL LOANS AND BURN-OFF'S This commercial loan is now a non-recourse loan. My thanks go out to David Repka of Bison Financial Group for this clear explanation. David is looking for commercial construction loans of over $10 million and can be reached at 727-537-0330. Commercial loanCOMMERCIAL LOANS

The rate is tied to prime, with a margin of 1.5% to 2.75%. Almost all SBA loans are closed at 2.75% over prime. Your deal would have to be pretty awesome to qualify for a margin of only 1.5%. Commercial construction loans are typically priced at prime + 1% to 1.5%INTERNATIONAL LOANS

A hard money lender on C-Loans.com at the time made a $3 million loan on a $20 million free-and-clear golf course and residential subdivision in Mexico. The loan was guaranteed by three pro atheletes, with a combined net worth in the range of $100 million. The hard money lender charged 15% and 15 points for an 18 month interest-only loan. ACQUISITION AND DEVELOPMENT LOANS Acquisition and Development Loans. A land development loan is an advance of funds, secured by a mortgage, to finance the making, installing, or constructing of the improvements necessary to convert raw land into construction-ready building sites. In other words, a land development loan takes an unimproved parcel and breaks it up into a number of smaller, improved parcels upon which homes or DEBT SERVICE COVERAGE RATIO Debt Service Coverage Ratio. The most important ratio in all of commercial mortgage underwriting is the debt service coverage ratio. The debt service coverage ratio is defined as the Net Operating Income (NOI) divided by Annual Debt Service on the proposed loan.Debt service is just a fancy word that means the loan payments. When you are computing a debt service coverage ratio, you should notDEBT YIELD RATIO

Debt Yield Ratio. The Debt Yield Ratio is defined as the Net Operating Income (NOI) divided by the first mortgage debt (loan) amount, times 100%. For example, let's say that a commercial property has a NOI of $437,000 per year, and some conduit lender has been asked to make a new first mortgage loan in the amount of $6,000,000. DOWN PAYMENTS ON COMMERCIAL LOANS C-Loans.com® is sponsored by C-Loans®, Inc.. For help with the operation of the software ONLY, please contact Tom Blackburne, Software Technical Advisor.Mobile phone: (574) 210-6686. 555 University Avenue, Suite 150, Sacramento, CA 95825 telephone: (916) 338-3232 * Fax: (916) 338-2328 REPRICING OF COMMERCIAL LOANS Repricing is defined as an increase in the interest rate of a commercial real estate loan after a term sheet has been agreed upon and after the third party reports have been completed. Conduits are the commercial lenders most likely to reprice a commercial loan. Some commercial mortgage lenders insist on fixed rate loans. DEBT YIELDS ON CMBS APARTMENT LOANS You will recall that the Debt Yield Ratio is different from the Debt Service Coverage Ratio.They are two completely different ratios. The Debt Yield Ratio is defined as the Net Operating Income (NOI) divided by the first mortgage debt (loan) amount, times 100%.. For example, let's say that a commercial property has a NOI of $437,000 per year, and some conduit lender has been asked to LICENSING FOR COMMERCIAL LOAN BROKERS Licensing for Commercial Loan Brokers. Most states in America do not require a commercial mortgage broker to obtain a mortgage broker's license or a real estate broker's license in order to negotiate commercial mortgage loans in their state. This fact, however, is oftennot obvious.

EB-5 COMMERCIAL LOANS AND THE EB-5 PROGRAM The entire process of EB-5 funding is a program developed by the United States Citizenship Immigration Service (USCIS) known as EB-5 Pilot program. USCIS is a division of Homeland Security. The EB-5 process can offer foreign immigrants a fast track path to obtaining US Visas for their "entire family". Simply said, by investing $545,000into an

FREE COMMERCIAL LOAN BROKER TRAINING I have trained over 10,000 practicing commercial mortgage brokers, and I have earned close to $1 million in training fees. But you don't have to pay me one red cent to spy on my training lessons to my sons. You'll learn about the new Debt Yield Ratio, and why life companiesand conduits are

HOW TO UNDERWRITE COMMERCIAL LOANS C-Loans.com® is sponsored by C-Loans®, Inc.. For help with the operation of the software ONLY, please contact Tom Blackburne, Software Technical Advisor.Mobile phone: (574) 210-6686. 555 University Avenue, Suite 150, Sacramento, CA 95825 telephone: (916) 338-3232 * Fax: (916) 338-2328 FINANCING OF LAND LEASES What is a land lease? A land lease happens when a land owner refuses to part with title to a piece of ground, but he is willing to lease out the use of the land for a very long period of time. Typically the land is unimproved, and the land lessee - the guy leasing the property - proceeds to construct a new building on the property.. Land leases can have any term, but two common lease terms are DEBT RATIO AND COMMERCIAL LOANS The Top Debt Ratio: The Top Debt Ratio is used to make sure that the borrower is not trying to make payments on a personal residence that is too much house for him. It is defined as follows: Top Debt Ratio = First and Second Mortgage Payments / Gross Income. Experience has repeatedly shown that whenever a borrower spends more than 25% to 28%of

FREE COMMERCIAL LOAN BROKER TRAINING I have trained over 10,000 practicing commercial mortgage brokers, and I have earned close to $1 million in training fees. But you don't have to pay me one red cent to spy on my training lessons to my sons. You'll learn about the new Debt Yield Ratio, and why life companiesand conduits are

HOW TO UNDERWRITE COMMERCIAL LOANS C-Loans.com® is sponsored by C-Loans®, Inc.. For help with the operation of the software ONLY, please contact Tom Blackburne, Software Technical Advisor.Mobile phone: (574) 210-6686. 555 University Avenue, Suite 150, Sacramento, CA 95825 telephone: (916) 338-3232 * Fax: (916) 338-2328 FINANCING OF LAND LEASES What is a land lease? A land lease happens when a land owner refuses to part with title to a piece of ground, but he is willing to lease out the use of the land for a very long period of time. Typically the land is unimproved, and the land lessee - the guy leasing the property - proceeds to construct a new building on the property.. Land leases can have any term, but two common lease terms are DEBT RATIO AND COMMERCIAL LOANS The Top Debt Ratio: The Top Debt Ratio is used to make sure that the borrower is not trying to make payments on a personal residence that is too much house for him. It is defined as follows: Top Debt Ratio = First and Second Mortgage Payments / Gross Income. Experience has repeatedly shown that whenever a borrower spends more than 25% to 28%of

COMMERCIAL CONSTRUCTION LOANS AND SOFT COSTS Construction Loans > Commercial Construction Loans and Soft Costs. Commercial Construction Loans and Soft Costs. Soft Costs Are the Non-Brick and Mortar Expenses . When underwriting a commercial construction loan, ther are four major categories of costs: the land cost, the hard costs, the soft costs, and the contingency reservereserve.

LEAD PURCHASE AGREEMENT Date: _____ LEAD PURCHASE AGREEMENT. Recitals. WHEREAS, C-Loans, Inc. (herein "C-Loans") operates a series of commercial mortgage portals, including C-Loans.com, where borrowers, real estate brokers, mortgage brokers, developers and others can apply on-line for a commercial mortgage loan to over 750 different commercial mortgage lenders using one simple application form; and COMMERCIAL LOANS AND TIC ROLL-UPS A tenancy-in-common investment ("TIC" or "TIC Investment") is an investment by a taxpayer in real estate which is co-owned with other investors. Since the taxpayer holds title to the real estate as a tenant-in-common, TIC investments qualify under the like-kind rules of �1031. In other words, if the 67-year-old owner of a big apartment EB-5 COMMERCIAL LOANS AND THE EB-5 PROGRAM The entire process of EB-5 funding is a program developed by the United States Citizenship Immigration Service (USCIS) known as EB-5 Pilot program. USCIS is a division of Homeland Security. The EB-5 process can offer foreign immigrants a fast track path to obtaining US Visas for their "entire family". Simply said, by investing $545,000into an

COMMERCIAL LOANS AND BURN-OFF'S This commercial loan is now a non-recourse loan. My thanks go out to David Repka of Bison Financial Group for this clear explanation. David is looking for commercial construction loans of over $10 million and can be reached at 727-537-0330. Commercial loan NEW CONSTRUCTION IS DOOMED AS BANKS STOP MAKING COMMERCIAL 2,500 For Just $79.95. The reason why is because the banks have stopped making new commercial construction loans. Banks are terrified right now, and the first thing that banks do when they get scared is to stop all commercial real estate lending. This lending freeze is especially true of commercial construction loans.INTERNATIONAL LOANS

A hard money lender on C-Loans.com at the time made a $3 million loan on a $20 million free-and-clear golf course and residential subdivision in Mexico. The loan was guaranteed by three pro atheletes, with a combined net worth in the range of $100 million. The hard money lender charged 15% and 15 points for an 18 month interest-only loan. COMMERCIAL MORTGAGE BROKER TRAINING Commercial Mortgage Broker Training. Brand New Commercial Mortgage Marketing Course - $199.This is old man Blackburne writing to you, and I have never been more proud of any product or service we have ever offered than this training course for commercial mortgage brokers, SBA lenders, and bankers. HOW TO UNDERWRITE COMMERCIAL LOANS C-Loans.com® is sponsored by C-Loans®, Inc.. For help with the operation of the software ONLY, please contact Tom Blackburne, Software Technical Advisor.Mobile phone: (574) 210-6686. 555 University Avenue, Suite 150, Sacramento, CA 95825 telephone: (916) 338-3232 * Fax: (916) 338-2328 FINANCING OF LAND LEASES What is a land lease? A land lease happens when a land owner refuses to part with title to a piece of ground, but he is willing to lease out the use of the land for a very long period of time. Typically the land is unimproved, and the land lessee - the guy leasing the property - proceeds to construct a new building on the property.. Land leases can have any term, but two common lease terms are DOWN PAYMENTS ON COMMERCIAL LOANS Conventional commercial real estate lenders typically require a minimum down payment of 25% to 30% of the purchase price. Unfortunately, you are no longer allowed to ask the seller to carry back a second mortgage behind the bank's new first mortgage. Your down payment must be cash.FEE AGREEMENTS

Fee Agreements. An important and painful lesson learned by just about every new commercial mortgage broker is to always require a signed fee agreement from the borrower. You’re going to learn this painful lesson eventually. The only real question is whether you learn this lesson after losing just five big commissions ($10,000+) or whetheryou

REPRICING OF COMMERCIAL LOANS Repricing is defined as an increase in the interest rate of a commercial real estate loan after a term sheet has been agreed upon and after the third party reports have been completed. Conduits are the commercial lenders most likely to reprice a commercial loan. Some commercial mortgage lenders insist on fixed rate loans. COMMERCIAL LOANS, CAP RATES, AND COMMERCIAL LOAN CONSTANTS Cap rates can vary from 3.5% to 13%, but an average commercial property in an average area these days sells at a cap rate of between 8% and 9.75%. Free List of 3,159 Commercial Lenders. Sort By Your Own Criteria. For example, let's suppose you win the lottery, but its only a small one. You net $1 million after taxes. COMMERCIAL LOANS AND THE MEANING OF "LAST DOLLAR" The term is used most often when mezzanine loans or preferred equity investments are stacked on top of very large permanent loans. The permanent lender's last dollar is 60% LTV, the mezzanine lender's last dollar is 75% LTV, and the preferred equity provider's last dollar DIFFERENCE BETWEEN A COMMERCIAL MORTGAGE LOAN AND A DEED A commercial loan, if secured by deed of trust, can be foreclosed much faster and much more cheaply than a commercial loan secured by a mortgage. California, like most of the states in the West, is a deed of trust state. This is why the trust deed investment business (hard money mortgage business) is so large in California. FREE COMMERCIAL LOAN BROKER TRAINING I have trained over 10,000 practicing commercial mortgage brokers, and I have earned close to $1 million in training fees. But you don't have to pay me one red cent to spy on my training lessons to my sons. You'll learn about the new Debt Yield Ratio, and why life companiesand conduits are

HOW TO UNDERWRITE COMMERCIAL LOANS C-Loans.com® is sponsored by C-Loans®, Inc.. For help with the operation of the software ONLY, please contact Tom Blackburne, Software Technical Advisor.Mobile phone: (574) 210-6686. 555 University Avenue, Suite 150, Sacramento, CA 95825 telephone: (916) 338-3232 * Fax: (916) 338-2328 FINANCING OF LAND LEASES What is a land lease? A land lease happens when a land owner refuses to part with title to a piece of ground, but he is willing to lease out the use of the land for a very long period of time. Typically the land is unimproved, and the land lessee - the guy leasing the property - proceeds to construct a new building on the property.. Land leases can have any term, but two common lease terms are DEBT RATIO AND COMMERCIAL LOANS The Top Debt Ratio: The Top Debt Ratio is used to make sure that the borrower is not trying to make payments on a personal residence that is too much house for him. It is defined as follows: Top Debt Ratio = First and Second Mortgage Payments / Gross Income. Experience has repeatedly shown that whenever a borrower spends more than 25% to 28%of

COMMERCIAL CONSTRUCTION LOANS AND SOFT COSTS Construction Loans > Commercial Construction Loans and Soft Costs. Commercial Construction Loans and Soft Costs. Soft Costs Are the Non-Brick and Mortar Expenses . When underwriting a commercial construction loan, ther are four major categories of costs: the land cost, the hard costs, the soft costs, and the contingency reservereserve.

LEAD PURCHASE AGREEMENT Date: _____ LEAD PURCHASE AGREEMENT. Recitals. WHEREAS, C-Loans, Inc. (herein "C-Loans") operates a series of commercial mortgage portals, including C-Loans.com, where borrowers, real estate brokers, mortgage brokers, developers and others can apply on-line for a commercial mortgage loan to over 750 different commercial mortgage lenders using one simple application form; and COMMERCIAL LOANS AND TIC ROLL-UPS A tenancy-in-common investment ("TIC" or "TIC Investment") is an investment by a taxpayer in real estate which is co-owned with other investors. Since the taxpayer holds title to the real estate as a tenant-in-common, TIC investments qualify under the like-kind rules of �1031. In other words, if the 67-year-old owner of a big apartment EB-5 COMMERCIAL LOANS AND THE EB-5 PROGRAM The entire process of EB-5 funding is a program developed by the United States Citizenship Immigration Service (USCIS) known as EB-5 Pilot program. USCIS is a division of Homeland Security. The EB-5 process can offer foreign immigrants a fast track path to obtaining US Visas for their "entire family". Simply said, by investing $545,000into an

COMMERCIAL LOANS AND BURN-OFF'S This commercial loan is now a non-recourse loan. My thanks go out to David Repka of Bison Financial Group for this clear explanation. David is looking for commercial construction loans of over $10 million and can be reached at 727-537-0330. Commercial loan FREE COMMERCIAL LOAN BROKER TRAINING I have trained over 10,000 practicing commercial mortgage brokers, and I have earned close to $1 million in training fees. But you don't have to pay me one red cent to spy on my training lessons to my sons. You'll learn about the new Debt Yield Ratio, and why life companiesand conduits are

HOW TO UNDERWRITE COMMERCIAL LOANS C-Loans.com® is sponsored by C-Loans®, Inc.. For help with the operation of the software ONLY, please contact Tom Blackburne, Software Technical Advisor.Mobile phone: (574) 210-6686. 555 University Avenue, Suite 150, Sacramento, CA 95825 telephone: (916) 338-3232 * Fax: (916) 338-2328 FINANCING OF LAND LEASES What is a land lease? A land lease happens when a land owner refuses to part with title to a piece of ground, but he is willing to lease out the use of the land for a very long period of time. Typically the land is unimproved, and the land lessee - the guy leasing the property - proceeds to construct a new building on the property.. Land leases can have any term, but two common lease terms are DEBT RATIO AND COMMERCIAL LOANS The Top Debt Ratio: The Top Debt Ratio is used to make sure that the borrower is not trying to make payments on a personal residence that is too much house for him. It is defined as follows: Top Debt Ratio = First and Second Mortgage Payments / Gross Income. Experience has repeatedly shown that whenever a borrower spends more than 25% to 28%of

COMMERCIAL CONSTRUCTION LOANS AND SOFT COSTS Construction Loans > Commercial Construction Loans and Soft Costs. Commercial Construction Loans and Soft Costs. Soft Costs Are the Non-Brick and Mortar Expenses . When underwriting a commercial construction loan, ther are four major categories of costs: the land cost, the hard costs, the soft costs, and the contingency reservereserve.

LEAD PURCHASE AGREEMENT Date: _____ LEAD PURCHASE AGREEMENT. Recitals. WHEREAS, C-Loans, Inc. (herein "C-Loans") operates a series of commercial mortgage portals, including C-Loans.com, where borrowers, real estate brokers, mortgage brokers, developers and others can apply on-line for a commercial mortgage loan to over 750 different commercial mortgage lenders using one simple application form; and COMMERCIAL LOANS AND TIC ROLL-UPS A tenancy-in-common investment ("TIC" or "TIC Investment") is an investment by a taxpayer in real estate which is co-owned with other investors. Since the taxpayer holds title to the real estate as a tenant-in-common, TIC investments qualify under the like-kind rules of �1031. In other words, if the 67-year-old owner of a big apartment EB-5 COMMERCIAL LOANS AND THE EB-5 PROGRAM The entire process of EB-5 funding is a program developed by the United States Citizenship Immigration Service (USCIS) known as EB-5 Pilot program. USCIS is a division of Homeland Security. The EB-5 process can offer foreign immigrants a fast track path to obtaining US Visas for their "entire family". Simply said, by investing $545,000into an

COMMERCIAL LOANS AND BURN-OFF'S This commercial loan is now a non-recourse loan. My thanks go out to David Repka of Bison Financial Group for this clear explanation. David is looking for commercial construction loans of over $10 million and can be reached at 727-537-0330. Commercial loan NEW CONSTRUCTION IS DOOMED AS BANKS STOP MAKING COMMERCIAL 2,500 For Just $79.95. The reason why is because the banks have stopped making new commercial construction loans. Banks are terrified right now, and the first thing that banks do when they get scared is to stop all commercial real estate lending. This lending freeze is especially true of commercial construction loans.INTERNATIONAL LOANS

A hard money lender on C-Loans.com at the time made a $3 million loan on a $20 million free-and-clear golf course and residential subdivision in Mexico. The loan was guaranteed by three pro atheletes, with a combined net worth in the range of $100 million. The hard money lender charged 15% and 15 points for an 18 month interest-only loan. COMMERCIAL MORTGAGE BROKER TRAINING Commercial Mortgage Broker Training. Brand New Commercial Mortgage Marketing Course - $199.This is old man Blackburne writing to you, and I have never been more proud of any product or service we have ever offered than this training course for commercial mortgage brokers, SBA lenders, and bankers. HOW TO UNDERWRITE COMMERCIAL LOANS C-Loans.com® is sponsored by C-Loans®, Inc.. For help with the operation of the software ONLY, please contact Tom Blackburne, Software Technical Advisor.Mobile phone: (574) 210-6686. 555 University Avenue, Suite 150, Sacramento, CA 95825 telephone: (916) 338-3232 * Fax: (916) 338-2328 FINANCING OF LAND LEASES What is a land lease? A land lease happens when a land owner refuses to part with title to a piece of ground, but he is willing to lease out the use of the land for a very long period of time. Typically the land is unimproved, and the land lessee - the guy leasing the property - proceeds to construct a new building on the property.. Land leases can have any term, but two common lease terms are DOWN PAYMENTS ON COMMERCIAL LOANS Conventional commercial real estate lenders typically require a minimum down payment of 25% to 30% of the purchase price. Unfortunately, you are no longer allowed to ask the seller to carry back a second mortgage behind the bank's new first mortgage. Your down payment must be cash.FEE AGREEMENTS

Fee Agreements. An important and painful lesson learned by just about every new commercial mortgage broker is to always require a signed fee agreement from the borrower. You’re going to learn this painful lesson eventually. The only real question is whether you learn this lesson after losing just five big commissions ($10,000+) or whetheryou

REPRICING OF COMMERCIAL LOANS Repricing is defined as an increase in the interest rate of a commercial real estate loan after a term sheet has been agreed upon and after the third party reports have been completed. Conduits are the commercial lenders most likely to reprice a commercial loan. Some commercial mortgage lenders insist on fixed rate loans. COMMERCIAL LOANS, CAP RATES, AND COMMERCIAL LOAN CONSTANTS Cap rates can vary from 3.5% to 13%, but an average commercial property in an average area these days sells at a cap rate of between 8% and 9.75%. Free List of 3,159 Commercial Lenders. Sort By Your Own Criteria. For example, let's suppose you win the lottery, but its only a small one. You net $1 million after taxes. COMMERCIAL LOANS AND THE MEANING OF "LAST DOLLAR" The term is used most often when mezzanine loans or preferred equity investments are stacked on top of very large permanent loans. The permanent lender's last dollar is 60% LTV, the mezzanine lender's last dollar is 75% LTV, and the preferred equity provider's last dollar DIFFERENCE BETWEEN A COMMERCIAL MORTGAGE LOAN AND A DEED A commercial loan, if secured by deed of trust, can be foreclosed much faster and much more cheaply than a commercial loan secured by a mortgage. California, like most of the states in the West, is a deed of trust state. This is why the trust deed investment business (hard money mortgage business) is so large in California.* Sign In

* Apply NOW

__Search

* Lender Vault

* Resource Center

* Terms of Use

__

* Sign In

* Apply NOW

*

Home

*

Lender Vault

*

Mortgage Brokers

*

Overview - Mortgage Brokers*

Cool Stuff For Mortgage Brokers*

Free Commercial Loan Placement Kit*

Need Commercial Mortgage Leads?*

Free List of 200 Commercial Lenders*

How To Market for Commercial Loans*

Get Paid to Enter Commercial Loans Into C-Loans*

Advice for Commercial Mortgage Brokers*

Focus on Permanent Loans*

Large Commercial Loans Seldom Close*

Don’t Chase Construction Loans*

International Loans Seldom Close*

Read the C-Loans Blog*

Market To Referral Sources for Deals*

Tips on How To Write a Newsletter*

Learn How To Create PDF’s*

Buying Commercial Leads*

Fee Agreements

*

Time Management

*

Pipeline Management

*

Choosing the Right Bank Loan Officer*

Importance of Wining and Dining*

Educate Yourself in Commercial Mortgage Finance*

Earn $5,000 Referral Fees in Your Sleep*

Earn Big Referral Fees Using Links in Your Emails*

Easy Referral Input Page*

Earn Fees for Referring Lenders*

Referral Fees

*

Consult With George Blackburne for $375 Per Hour*

Expert Witness in Commercial Mortgage Matters*

Earn $2,000 Every Time You Blast Out Your E-Mail Newsletter*

Earn a $2,000 Referral Fee For One Quick Phone Call or E-Mail*

Refer Commercial Loans by Telephone*

Mortgage Broker Success Stories*

Past Mortgage Broker Newsletters*

Commercial Loans NOT Secured By Real Estate*

Commercial Mortgage Marketing Course*

Commercial Loan Calculator*

Fix and Flip Loans

*

Franchise Loans and Franchising Financing*

Buy Leads If Your Credit Is Only So-So*

Free Commercial Loan Software*

Free List of 750 Commercial Lenders*

Secrets to Referral Fees*

Training

*

Learn To Broker Commercial Loans*

Find Your Own Private Investors. Service Your Own Deals.*

Commercial Mortgage Marketing Manual Only $199*

Mortgage Broker Fee Agreement By an Attorney Only $199*

Learn to Underwrite Commercial Mortgage Loans - Only $199*

Get All 3 Commercial Financing Tools For Just $249*

Intermediate Commercial Mortgage Training*

The Practice of Commercial Mortgage Brokerage*

Loan Servicing Software*

Free Commercial Loan Broker Training*

Commercial Mortgage Broker Training*

Buy Both Training Programs*

How to Underwrite Commercial Loans*

Borrowers

*

Overview – Borrowers*

Free Commercial Loan Placement Kit*

Free List of 200 Commercial Lenders*

Cool Stuff Just for Direct Commercial Mortgage Borrowers*

What is a Commercial Loan?*

Difference Between a Commercial Loan and a Home Loan*

Commercial Loan Rates Compared to Home Loan Rates*

Will I Qualify for a Commercial Loan?*

How Large of a Commercial Loan Can I Get?*

Commercial Loan Calculator*

Commercial Mortgage Calculator*

How To Get a Commercial Loan*

Where Can I Find a Good Commercial Loan?*

How To Find a Commercial Lender*

Need More Lenders?

*

Who is Making Commercial Loans Today?*

What Types Of Commercial Lenders Offer The Lowest Rates*

Before You Apply for a Commercial Mortgage Loan*

Commercial Loan Tips*

Commercial Loan Processing Time*

Commercial Lenders Are Unpredictable*

Commercial Appraisals*

Toxic Reports

*

Application Fees

*

Terms Sheets

*

Local Lenders

*

Use Your Deposit Relationship*

Size of Your Commercial Lender*

Seven Investment Property Loan Tips*

Balloon Payment Too Big?*

Referral Fees

*

Easy Referral Input Page*

Borrower Success Stories*

Past Private Client Newsletters*

Commercial Real Estate Loans*

Fix and Flip Loans

*

Fix and Flip Loan Center*

Trust Deed Investing*

Investment Property Loans*

Finding Construction Lenders*

Equity For Commercial Construction Deals*

Down Payments on Commercial Loans*

How Do Commercial Loans Work?*

Commercial Loans Resource Center*

Commercial Real Estate Loan Rates*

Commercial Loan Interest Rates*

Real Estate Brokers

*

Overview - Commercial Real Estate Brokers*

Free Commercial Loan Placement Kit*

Free List of 200 Commercial Lenders*

Cool Stuff For Commercial Real Estate Brokers*

Open a Commercial Mortgage Company on the Side*

Open Your Own Hard Money Lending Company*

Put a Link on Your Website and Earn $5,000*

Put a Link in Your Emails and Earn $10,0000*

Referral Fees

*

Easy Referral Input Page*

Past Commercial Real Estate Broker Newsletters*

Fix and Flip Loans

*

How To Get Listed For Free on Our Find a Commercial Broker Directory*

Secrets to Referral Fees*

Lenders

*

Overview – Commercial Mortgage Lenders*

Free SBA Loan Leads

*

Join C-Loans As a Lender*

Commercial Lending Preferences*

Interesting Stuff for Direct Commercial Lenders*

What Does C-Loans Cost a Lender?*

Can't Get Your Good Customer Enough Loan Proceeds?*

Commercial Mortgage Marketing Course*

Commercial Loan App’s Delivered To Your Email Box*

Easiest Way To Earn Large Referral Fees*

Referral Fees

*

Easy Referral Input Page*

Need an Expert Witness?*

Banker Success Stories*

Past Banker Newsletters*

Get Our Marketing Course For Free*

Free Commercial Loan Software*

About Us

*

Overview – C-Loans, Inc.*

Apply Now

*

Contact Us

*

Recent C-Loans Closings*

Awards and Affiliations*

George’s Book at Amazon*

Client Success Stories*

C-Loans Graphics and Banners Center*

C-Loans Blog – Free Training* Home

* Mortgage Brokers

MORTGAGE BROKERS

*

Column 1

* Free Commercial Loan Placement Kit * Free Commercial Loan Software * Cool Stuff For Mortgage Brokers * Need Commercial Mortgage Leads? * Commercial Loan Calculator * Free List of 200 Commercial Lenders * Free List of 750 Commercial Lenders * Secrets to Referral Fees*

Column 3

* Earn $5,000 Referral Fees in Your Sleep * Earn Big Referral Fees Using Links in Your Emails * Easy Referral Input Page * Earn Fees for Referring Lenders* Referral Fees

*

Column 4

* Earn $2,000 Every Time You Blast Out Your E-Mail Newsletter * Earn a $2,000 Referral Fee For One Quick Phone Call or E-Mail * Refer Commercial Loans by Telephone * Mortgage Broker Success Stories * Past Mortgage Broker Newsletters* Training

TRAINING

*

Column 1

* Learn To Broker Commercial Loans * Find Your Own Private Investors. Service Your Own Deals. * Buy Both Training Courses - How to Broker Commercial Loans and How to Find Private Investors - For Just $849 * The Practice of Commercial Mortgage Brokerage * Commercial Mortgage Marketing Manual Only $199 * Mortgage Broker Fee Agreement By an Attorney Only $199*

Column 2

* Learn to Underwrite Commercial Mortgage Loans - Only $199 * Get All 3 Commercial Financing Tools For Just $249 * Intermediate Commercial Mortgage Training * Loan Servicing Software * Free Commercial Loan Broker Training * Commercial Mortgage Broker Training * Free Training Articles About Commercial Loans* Borrowers

BORROWERS

*

Column 1

* Overview – Borrowers * Earn 8% to 12% Interest * Free Commercial Loan Placement Kit * Free List of 200 Commercial Lenders * Cool Stuff Just for Direct Commercial Mortgage Borrowers * What is a Commercial Loan? * Difference Between a Commercial Loan and a Home Loan * How Do Commercial Loans Work?*

Column 2

* Fix and Flip Loan Center * Fix and Flip Loans * Fix and Flip Funding * Fix and Flip Loans - Leverage * Financing For Flipping Homes * Commercial Loans Resource Center * Commercial Loan Rates Compared to Home Loan Rates * How to Underwrite Commercial Loans*

Column 3

* Need More Lenders? * Who is Making Commercial Loans Today? * What Types Of Commercial Lenders Offer The Lowest Rates * Before You Apply for a Commercial Mortgage Loan * How Large of a Commercial Loan Can I Get? * Investment Property Loans*

Column 4

* Referral Fees

* Easy Referral Input Page * Borrower Success Stories * Past Private Client Newsletters * Commercial Real Estate Loan Rates * Find a Commercial Broker * Commercial Loan Interest Rates * Real Estate BrokersREAL ESTATE BROKERS

*

Columnn 1

* Fix and Flip Loans * Overview - Commercial Real Estate Brokers * Free Commercial Loan Placement Kit * Free List of 200 Commercial Lenders * Cool Stuff For Commercial Real Estate Brokers * Secrets to Referral Fees*

Column 2

* Fix and Flip Loan Center * Fix and Flip Loans * Fix and Flip Funding * Fix and Flip Loans - Leverage * Investment Property Loans * Find a Commercial Broker*

Column 3

* Put a Link on Your Website and Earn $5,000 * Put a Link in Your Emails and Earn $10,000* Referral Fees

* Easy Referral Input Page * Past Commercial Real Estate Broker Newsletters * Commercial Loan Rates Compared to Home Loan Rates * How To Get Listed For Free on Our Find a Commercial BrokerDirectory

* Lenders

LENDERS

*

Columnn 1

* Overview – Commercial Mortgage Lenders * Commercial Lending Preferences * Commercial Loan App’s Delivered To Your Email Box * Free SBA Loan Leads * Join C-Loans As a Lender*

Column 2

* Fix and Flip Loan Center * Fix and Flip Loans * Fix and Flip Funding * Fix and Flip Loans - Leverage*

Column 3

* Get Our Marketing Course For Free * Easiest Way To Earn Large Referral Fees * Easy Referral Input Page * Need an Expert Witness? * Banker Success Stories * Past Banker Newsletters* About Us

ABOUT US

*

Columnn 1

* Overview – C-Loans, Inc.* Apply Now

* Contact Us

* Recent C-Loans Closings * Awards and Affiliations * George’s Book at Amazon * Client Success Stories * C-Loans Graphics and Banners Center * C-Loans Blog – Free Training* Blog

Search

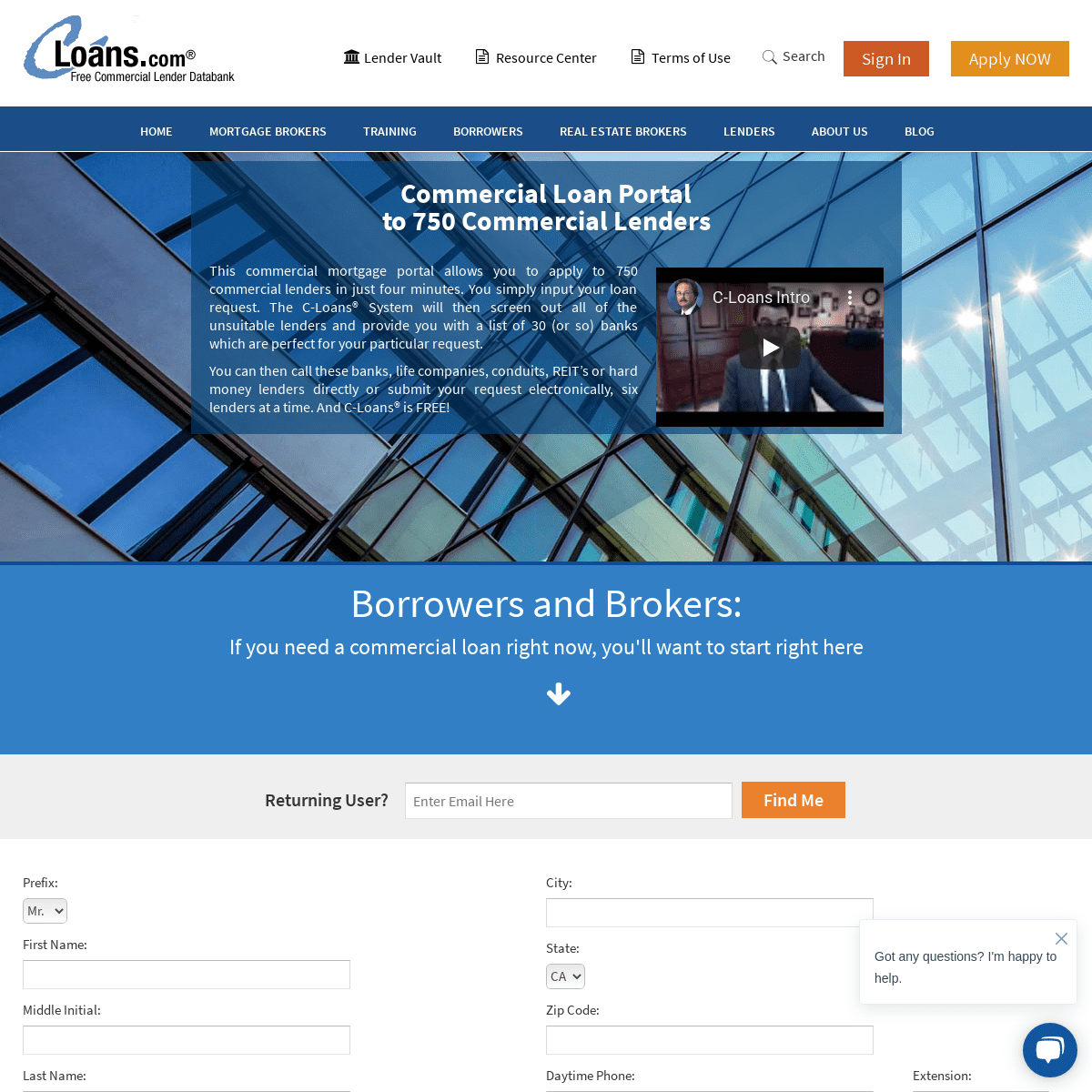

COMMERCIAL LOAN PORTAL TO 750 COMMERCIAL LENDERS This commercial mortgage portal allows you to apply to 750 commercial lenders in just four minutes. You simply input your loan request. The C-Loans® System will then screen out all of the unsuitable lenders and provide you with a list of 30 (or so) banks which are perfect for your particular request. You can then call these banks, life companies, conduits, REIT’s or hard money lenders directly or submit your request electronically, six lenders at a time. And C-Loans® is FREE!* «

* »

* Play

* 01

BORROWERS AND BROKERS: If you need a commercial loan right now, you'll want to start righthere

Returning User?

Prefix:

Mr.Mrs.Dr.MissMs.

First Name:

Middle Initial:

Last Name:

Suffix:

IIIIIIVJr.Esq.M.D.

I am

the Borrower for this loana Mortgage Brokerthe Real Estate Brokeran Employee of the brokerthe Financial Advisor for this loanSomeone else who is not listed herethe Developer for this projectCompany Name:

Mailing Address:

Additional Line 2:

City:

State:

AKALARAZCACOCTDCDEFLGAHIIAIDILINKSKYLAMAMDMEMIMNMOMSMTNCNDNENHNJNMNVNYOHOKORPARISCSDTNTXUTVAVIVTWAWIWVWYZip Code:

Daytime Phone:

Extension:

Fax:

Evening Phone:

Cellphone:

E-mail address:

E-mail address (confirm):FREE SBA LOAN LEADS

Must Be a Salaried Loan Officer at a Commercial Bank BANKS AND DIRECT LENDERS* If You Need More Commercial Loans, Please Press Here *Servicing $20 Million+ in Commercial Loans COMMERCIAL MORTGAGE BROKER TRAINING Learn how to market for commercial mortgage loans, how to underwrite them, how to package them, where to place them, and how to collectyour fee.

COOL STUFF FOR BROKERS & BORROWERSFree Commercial

Loan Software

FREE

Commercial Loan Calculator Accredited Investors Earn 11% to 13% InterestLearn Commercial

Mortgage Finance

Free Daily Lessons in CommercialMortgage Brokerage

(Sign Up Here)

Free Loan

Placement Kit

Become a Hard Money

Lender Yourself

Submit Your Commercial Loan to 750 Lenders for Free!Marketing Course

This Brand New Program is Fantastic!Commercial

Mortgage.com

Free List of 200

Lenders

Mortgage Brokers:

Buy Cheap Leads

You’re Running Your CommercialLoan Shop All Wrong

Fee Collection CourseCommercial Mortgage

Training

Commercial Loan

Resource Center

Find a

Commercial Broker

Commercial Broker Directory -Get Listed

PRIMER ON COMMERCIAL REAL ESTATE FINANCE _EVEN YOU OLD PRO’S WILL LEARN A TON_ COMMERCIAL LOAN QUICK START Please forgive me if this first section sounds like a sales pitch; but I have an important concept to convey. Even if you are an old pro at commercial real estate finance, you will find our _FREE_ commercial mortgage portal, C-Loans.com , to be a great way to quickly present your commercial loan request to _hundreds_ ofdifferent banks.

Here’s that important concept: Why present your loan to so many banks? There is a bank out there right now that is too flush with cash. The bank president is yelling at his senior vice president, “We need to make some commercial loans _right now!_” IT IS THIS TOO-LIQUID BANK WHICH WILL GIVE YOU THE LARGEST NEW LOAN AT THE LOWEST INTEREST RATE. The C-Loans System (we spent $2.2MM writing this code) helps you to pinpoint that too-liquidbank.

Are you looking for an SBA loan to buy a building for your business? Grasp this concept: Every SBA lender is different. Your application for an $600,000 SBA loan to buy a campground could get turned down by 19 banks, only to have the 20th bank approve your deal because the president of that particular bank happens to own a $300,000 RV and loves to camp. There are over 250 different SBA lenders on C-Loans, and in just four minutes you can submit your deal to all of them, six lenders at a time. Are you looking for a loan to buy an investment property, like an apartment building, office building, and or retail center? Once again – The hungriest bank will give you the most leverage and require _THE SMALLEST DOWN PAYMENT_. Who is the hungriest bank? Among our 750 different banks, this changes daily, depending on which bank just got some loan payoff’s or some huge new deposits. Submitting your commercial loan using C-Loans helps you to instantly identify which SVP of Real Estate Loans is getting chewed out by his boss. _Haha!_ Does your deal have some black hairs? Maybe your company is losing money. Maybe you went through a divorce and went bankrupt two years ago? There are over 300 commercial lenders - subprime lenders and hard money lenders - on our portal who specialize in making less-than-perfect commercial loans. As you fill out your mini-app, you’ll see a section named, “Special Issues”. Just identify your concern. For example, “One of my two retail spaces is vacant; but unfortunately I have a balloon payment coming due, so I have to borrow right now.” Boom. The lenders will screen themselves, and the forgiving ones will reach out to you with offers. WHAT IS A COMMERCIAL LOAN? (PREPARE TO LEARN SOMETHING.) The word “commercial” is just a fancy word for “business”, so a commercial loan is just another way of saying business loan. To really understand what constitutes a commercial real estate loan, it is easier to understand what it is not. A loan secured by a single-family residence, a condo, a townhouse, a duplex, a triplex, or a 4-plex is considered to be a residential loan. In the parlance of the industry, such properties are known as one-to-four family dwellings, and loans secured by 1-4 family dwellings are considered to be residential loans. Residential loans are special because they can be sold overnight to Fannie Mae or Freddie Mac in a pinch. Because they are _LIQUID INVESTMENTS_, loans secured by one-to-four family dwellings enjoy MUCH lower interest rates - as much as 1.25% lower. Definition of a Commercial Loan: A commercial real estate loan is therefore a real estate loan that is NOT secured by a one-to-four family dwelling. A land loan is an example of a commercial real estateloan. Surprised?

Example:

You own a four-plex, and all of the units are rented out to tenants. You are holding the property as an investment to provide income for your retirement. You want to refinance your four-plex to pull out some equity in order to buy a five-plex. The loan against your non-owner-occupied four-plex is a commercial loan because it is an investment property, and the purpose of the loan is not for personal, family, or household purposes. True or false? _False!_ A loan on your existing four-plex is still a residential loan, even though the property is non-owner-occupied. As a residential loan, it will enjoy an interest rate that is at least three-quarters of a percent lower than the commercial loan that you will eventually get on your new five-plex. Remember, the cutoff is four units. If the multifamily property has more than four units, you need to apply to a commercial lender. To get a residential loan on your non-owner-occupied 4-plex, you should apply to a residential lender, like Quicken Loans. To get a commercial loan on your new 5-plex, you should apply using C-Loans. WHAT ARE THE DIFFERENT TYPES OF COMMERCIAL LOANS? There are more than a dozen different types of commercial loans, although most real estate investors will only use one of the firstfive types:

PERMANENT LOANS - This is the most common type of commercial real estate loan. A permanent loan is a garden-variety first mortgage on a commercial property. To qualify as a permanent loan, the loan must have a term of at least five years and some amortization. In other words, a permanent loan cannot just have interest-only payments. In contrast with residential loans, which often enjoy a 30-year amortization, most commercial permanent loans have a 25-year amortization. If the property is older than 35-years-old, the lender might even a 20-year amortization. The one exception to this rule is multifamily properties (apartment buildings). Most multifamily permanent loans have a 30-year amortization. Most commercial permanent loans are made by banks, and, with the exception of multifamily properties, have a maximum term of ten years. SBA LOANS - If your business partially-occupies a commercial property, this is the loan for you. SBA loans are NOT made by the Small Business Administration (“SBA”). The SBA merely guarantees certain commercial loans made by banks and specialty finance companies. If you have been in business for at least three years, you can get an SBA loan of 90% loan-to-value to buy a building for your business to occupy; otherwise, you’ll have to put 30% down. The SBA only guarantees a portion of an SBA loan, so the bank making the loan has some of its own dough at risk. This is why 19 SBA lenders could turn your deal down, only to have the 20th SBA lender approve your deal. There are over 250 different SBA lenders on C-Loans. CONSTRUCTION LOANS - These loans are used to pay for the construction of commercial buildings, residential subdivisions (tracts of houses), and residential condominium developments. Construction loans usually have a term of just one year, although a six-month extension can sometimes be negotiated for an extra point. The bank doesn’t just give the borrower $3 million and hopes he builds the apartment building, as opposed to skipping to Mexico. Instead, the bank only advances funds as work is completed. For example, when the grading is done, the grading contractor is paid. The interesting thing about construction loans is that while they have interest-only monthly payments, a reserve, funded by the bank, is created at the beginning of the loan to make these monthly interest payments. The borrower only has to pay interest on the amount of the construction loan that has been drawn down to date. In other words, the interest payment in month one is usually very small because the developer has used very little of the loan proceeds. CONSTRUCTION LOANS ARE MADE BY LOCAL LENDERS, rather than by some big bank in faraway New York City, because someone from the bank has to go out to the property regularly to inspect the progress of construction before it approves any disbursements to the subcontractors. These visits are called PROGRESS INSPECTIONS, and there is small fee to the borrower for each one. BRIDGE LOANS - A bridge loan is a short-term loan, and most bridge lenders can fund these loans very quickly (30 days versus the normal 75 days). Bridge loans have a term of between one year and five years, and they have interest-only monthly payments. Bridge loans are usually much more expensive than permanent loans or construction loans. Bridge loans are often used on _VALUED-ADDED PROJECTS_, where the finished value of the project is projected to be much higher than the cost to acquire the property and to renovate it. They can also be used to give the owner time to find a tenant. Large bridge loans ($3 million+) are usually floating rate loans, tied to LIBOR. (Did you know that LIBOR will stop being computed on January 1, 2022 because of all of the corruption associated with its computation?) Another type of bridge loan is a short-term loan made by a hard money lender. Hard money bridge loans can be for any purpose, not just to renovate the property. Hard money bridge loans usually have a fixed rate. There are 300+ bridge lenders on C-Loans. USDA BUSINESS &INDUSTRY LOANS - You may have never heard of the USDA Business and Industry (“B&I”) loan program, but it is very similar to the SBA loan program. Some of the poorest Americans live in rural areas, where there are few job opportunities. The purpose of B&I loans is to bring jobs to rural areas, defined as cities of less than 50,000 in population. Unlike SBA loans, B&I loans do NOT require that the property be owner-used, as long as the loan is projected to bring jobs to the rural area. USDA B&I loans can be as large as $25 million, compared to just $10 million for an SBA loan. They can have fixed rates and have a 30-year amortization. That portion of the loan secured by equipment can have a term as long as fifteen years, compared to just ten years on SBA loans. There are 125+ USDA commercial lenders on C-Loans. There are a whole bunch of other types of commercial loans, but most of them don’t apply to the typical commercial real estate investor. We will discuss them much further below in the section, “Other Types of Commercial Mortgages”. WHAT ARE COMMERCIAL MORTGAGE RATES TODAY? Let’s talk first about the interest rate on commercial permanent loans (garden-variety first mortgages). Earlier we mentioned that commercial mortgage rates are typically 75 to 125 basis points higher than residential mortgage rates. A _BASIS POINT_ is 1/100th of one percent, so 125 basis points is 1.25%. Therefore, if the 30-year conforming mortgage rate is 4.0% today, then commercial mortgage rates would be around 4.75% to 5.25%. Here is something that will surprise you. Banks from Maine to Florida, to California, and to Hawaii generally have almost the exact same conventional commercial mortgage rates, terms, and programs. There is almost no price competition in banking. Banks move together like a giant herd. _Moooo_. The typical commercial permanent loan from a bank has a fixed rate for the first five years. Then there is one rate-readjustment to market. The interest rate is then fixed for five more years. The loan is amortized over 25 years, and it has a term of ten years. There is generally some sort of declining prepayment penalty, like 3-2-1 or 5-4-3-2-1. There will be a six-month window at the end of five years, and then the prepayment penalty will apply again to the second five years. And remember, most banks have this exact same program. So what is the interest rate? You can predict it with some precision. Just look up five-year Treasuries on the internet and then add between 275 to 350 basis points (2.75% to 3.5%). Therefore, if five-year Treasuries are 2.0% today, your rate will be between 4.75% to 5.5%. Obviously, only the very best deals get the lowest rate. What about SBA loans? Most SBA loans are made using the 7a Program, which is a 25-year, fully-amortized, floating-rate loan. The rate is tied to prime, with a margin of 1.5% to 2.75%. Almost all SBA loans are closed at 2.75% over prime. Your deal would have to be pretty awesome to qualify for a margin of only 1.5%. Commercial construction loans are typically priced at prime + 1% to 1.5% floating, 1 to 1.5 points, one year, interest-only. Bridge loans vary greatly in price, depending on the quality of the deal and the borrower. High-net-worth borrowers, on large, good-quality properties can get floating-rate bridge loans tied to LIBOR, with a margin as low as 4.5% to 5.5%. (LIBOR is really-really low.) Average deals to clean borrowers might be priced at 6% to 8% floating over LIBOR. The points would be 1.5 to 2.5. Hard money bridge loans are typically fixed rate loans with rates as low as 8% (in California), 9% to 10% nationwide, and sometimes as high as 12% to 13% on riskier deals. The points are typically 2 to 3. Few people know about the USDA commercial loan program, but the program is terrific. If the deal is really good, you can negotiate a fixed rate and a 30-year amortization; otherwise, the rates and terms on a USDA Business and Industry loan are similar to those of SBAloans.

HOW DO COMMERCIAL LOANS WORK? Commercial loans almost always need to be secured. UNSECURED LINES OF CREDIT are difficult to obtain, unless the loan amount is fairly small (less than $100,000), your net worth is very high, you keep tons of cash in the bank, and your credit is perfect. The collateral available to serve as the security for your commercial loan determines the type of commercial loan you can get and the kind of lender to whom you should apply. If the collateral is a multifamily property (apartment building), then you would apply for a MULTIFAMILY LOAN to either a life company, a conduit, a bank, or an agency lender specializing in multifamily loans. Agency lenders include Fannie Mae, Freddie Mac, and Ginnie Mae. We will discuss agency lenders in more detail below. If the collateral is an investment property, like an office building, retail property, strip center, shopping center, industrial building, warehouse, mobile home park, or self-storage facility, you will likely apply for a PERMANENT LOAN to either a life company, a conduit, a bank, or a credit union. Life companies seldom lend on anything other than office, retail, and industrial properties. If the property is owner-occupied by your business, you would most likely apply for an SBA LOAN to a bank or a specialized SBA lender. If the property is located in a small town or rural area, you may want to apply for a USDA LOAN to a bank or a specialized USDA lender. If no real estate is available, and you are trying to buy or borrow against some equipment, you would apply for an EQUIPMENT LOAN to either a bank or an equipment finance company. You could also apply to a leasing company to just lease the equipment. If your proposed collateral is your ACCOUNTS RECEIVABLE, you would apply for an accounts receivable loan to either a bank or a specialty finance company. If you were really-really desperate, you could actually sell your accounts receivable to a factor at a huge discount. Ouch! This method of financing your business is called FACTORING. If your proposed collateral is your inventory of, say, 100 completed surfboards, you would apply for an INVENTORY LOAN to either a bank or a specialty finance company. Most commercial real estate loans have balloon payments. There are three major exceptions - multifamily loans, SBA 5a loans, and USDA Business and Industry loans. These last three loan types usually enjoy long-term, fully-amortized loans. Unfortunately, C-Loans does not place business loans not secured byreal estate.

WHO MAKES COMMERCIAL LOANS? Below is a list of the major types of lenders who make commercial real estate loans. They are listed in order, which the cheapest, most desirable lenders at the top. LIFE COMPANIES - A life company is just short for a life insurance company, and they have, by far, the cheapest commercial mortgage rates. Their interest rates are probably 35 to 45 basis points cheaper than conduits, the second cheapest type of commercial lender. There are two key things to understand about life companies: (1) They only make fixed rate loans; and (2) they never want to get paid off early. The reason why is because life companies work off of actuarial tables to pay their death benefits, so they need to know _exactly_ how much they will make (fixed rate) and exactly when they will get paid off (no early prepayments). Because they are the prettiest girl at the dance, they get to go home with the quarterback. Their typical minimum loan is a whopping $5 million. They will only finance very standard property types - multifamily, office, retail and industrial properties (the Four Major Food Groups) - in the nicest areas of Football Team cities. And if that was not picky enough, life companies will rarely exceed 60% loan-to-value. In forty years, I (George Blackburne III, the old attorney) have never successfully closed a loan with a lifecompany.

CONDUITS - Conduit is short for Real Estate Mortgage Investment Conduit (“REMIC”). Conduits are specialized commercial mortgage companies that originate very large ($5 million and up) commercial real estate loans on the Four Major Food Groups. These are deals with a slightly higher LTV’s than a life company would tolerate and/or properties that are not quite pretty enough or well-located enough for a life company. These conduit loans are very cookie-cutter and plain vanilla. The loans are thrown into a huge pool. When the conduit has amassed at least $1.5 billion of these cookie-cutter commercial loans, the pool is rated by Moody’s or Standard & Poor’s, and then the pool is securitized. Securitization means that bonds (IOU’s) are issued, secured by the loans in the pool. If you were to buy one of these bonds, you might own 1/300,000th of this pool of loans. COMMERCIAL BANKS - A commercial bank is just a garden-variety bank that accepts deposits and makes loans, in contrast with an _INVESTMENT BANK_ (which sell stocks or takes companies public) or a _MERCHANT BANK_ (they invest equity in companies rather than make loans). Banks will make commercial real estate loans as small as $100,000 to as large as $300 million. Banks will finance almost all commercial property types, including construction loans on residential subdivisions and permanent loans on restaurants, as long as the borrower is making money and has plenty of cash in the bank. The only exception is politically-incorrect properties, like casinos, gentlemen’s clubs, and pot dispensaries. A good rule of thumb is to never apply to a bank for a loan if you need money. Huh? Sell something and put some cash in your bank account first. Then apply to the bank for a loan. If you know you will need cash in March, apply for the loan in August of the prior year, when your busy season has just ended and you are flush with cash. Here is another good rule for dealing with banks. Banks greatly prefer to make short-term loans to _HIGH-NET-WORTH INDIVIDUALS_ (memorize this banking term of art), who maintain large cash balances in their bank. A good way to get a borderline deal approved is to approach a small bank and promise to move all of the borrower’s accounts to this small bank. CREDIT UNIONS - Credit unions have come out of nowhere in recent years to seize 6% of the commercial real estate loan market. They offer the same interest rate and terms as commercial banks, without the weirdness of only lending to liquid borrowers. If you have good credit and your commercial loan cash flows, they will make you the loan in a heartbeat, even if you have very little cash in the bank. It used to be that you had to work for a particular company in order to qualify for a loan from a credit union; but those days are long gone. Today, all you have to do is live in the same state as the credit union OR own a property in that same state in order to qualify. The credit union, by law, will require that you open a token account with thecredit union.

REIT’S - A REIT is a real estate investment trust. It’s basically a corporation that invests exclusively in real estate and/or mortgages. For tax reasons, a REIT must distribute 90% of its taxable income as dividends. There are very few surviving mortgage REIT’s, and those few that still exist today make mainly expensive bridge loans; but they are still cheaper than hard money lenders. HARD MONEY LENDERS - With the rise of crowd-funding, there are now almost 1,000 commercial hard money lenders across America scratching and clawing for deals. The good news is that this has driven down hard money mortgage rates down below 10%, and, in California, to as low as 8%. God bless capitalism. Quick joke: Why do communists only write using lower-case letters? Answer: They hate capitalism. _Haha!_ OTHER TYPES OF COMMERCIAL OR PERSONAL-PROPERTY-SECURED BUSINESS LOANS AGENCY LOAN - An agency loan is typically a multifamily loan or senior housing loan that is guaranteed by some government-sponsored enterprise (“GSE”), such as Fannie Mae, Freddie Mac, or Ginnie Mae. Agency loans have 30-year terms and a terrific, low, fixed rate. The minimum agency loan is $1 million, and the process is a littleslow.

SBA 7(A) LOAN - The SBA 7(a) program is a 25-year, fully-amortized, first mortgage loan program with a floating rate, tied to the Prime Rate. It is the most common type of SBA loan. The maximum loan amountis $5 million.

SBA 504 LOAN - The SBA 504 loan program starts with a conventional, fixed-rate, first mortgage, which is typically made by a bank. The first mortgage usually has a term of ten years. Behind this conventional first mortgage, a local community development corporation will make a 20-year fully-amortized, SBA-guaranteed, second mortgage. It is the most common way to get a fixed rate SBA loan. The maximum SBA 504 loan is $10 million combined. TAKEOUT LOAN - A takeout loan is simply a garden-variety permanent loan that pays off a construction loan.CONNECT WITH US

*

*

*

*

C-Loans.com® is sponsored by C-Loans®, Inc. For help with the operation of the software ONLY, please contact Tom Blackburne, Software Technical Advisor. Mobile phone: (574) 210-6686. 555 University Avenue, Suite 150, Sacramento, CA 95825 telephone: (916) 338-3232 * Fax: (916) 338-2328 Real Estate Broker — California Dept. of Real Estate License:00829677

Arizona Dept. of Financial Institutions License: MB-0909472 Florida Mortgage Brokers License: MLD1726 / MLD519NMLS ID: 103430

Read our many client Success Stories » * Return to C-Loans® Home Page * Return to BlackburneandSons.com Home Page � 2021 C-Loans®, Inc. All rights reserved. Sacramento Web Design* Terms of Use

* Disclaimer

* Awards & Affiliations* Privacy Policy

* Site Map

LOG IN

×

INTRODUCING C-LOANS LITE! JUST COMPLETE ONE SIMPLE FORM. WITHIN MINUTES, HUNGRY BANKS AND OTHER COMMERCIAL LENDERS WILL BE CONTACTING YOU WITH OFFERS.LEARN MORE

Details

6