6

More Annotations

4

5

Favourite Annotations

2

4

Text

JOHN CHARCOL

John Charcol is the original independent mortgage broker. We have over 40 years’ experience in finding the best mortgage rates for every type of buyer. Whether you’re investing in property or looking to buy your first home, we can help. Our expert, independent mortgage advice will make buying your home or property investment easy. CAPITAL GAINS TAX CALCULATOR UK 2020 Our Capital Gains Tax calculator gives you an estimate of how much you could have to pay in Capital Gains Tax (CGT) when you sell your property in the UK. Simply enter your total earnings, the sale and purchase price of the property and your tax-deductible expenses and click the Calculate button. CGT tax deductible expenses include: StampDuty

GUIDE TO LIMITED COMPANY BUY-TO-LET as now transitional rates new 2016/17 2017/18 2018/19 2019/20 2020 onwards rental income £15,000 £15,000 £15,000 £15,000 £15,000 mortgage interest £10,800 £10,800 £10,800 £10,800 £10,800 reduction in mortgagae interest allowance MORTGAGE LOAN-TO-VALUE CALCULATOR 2020 How to Calculate LTV for Mortgage. You want to buy a house for �400,000. You have £80,000 in savings that you want to put down as a deposit. You take out a mortgage/loan to cover the remaining amount: �400,000 - £80,000 = £320,000. Your LTV is 80%: (£320,000 – 400,000) x 100 = 80. CAPITAL GAINS TAX ON SECOND HOMES Your new income is above £50,000 and so falls into the higher rate tax band: You pay 18% CGT on the taxable gains above £45,000 and up to £50,000: (£50,000 - £45,000) = £5,000. 18% of £5,000 (£5,000 x 0.18) = £900 in CGT. You pay 28% CGT on the taxable gains on the amount above £50,000: (£133,000 - £50,000) = £83,000. HOW CAN I BUY A HOUSE WHEN I HAVEN'T SOLD MY CURRENT Again you will need to make sure that the new mortgage gives you the flexibility to reduce the amount outstanding once you have sold your current home without being penalised. I believe we can help you and that you would benefit from speaking to one of our independent mortgage advisers. Please call 03304 332 927 and one of our adviserswill

WHAT IS THE MINIMUM SIZE FOR A FLAT TO GET A The usual minimum for a studio flat to be acceptable for a mortgage is 30 sq metres. There are a couple of lenders who do not state a minimum size for studio flats because their suitability as security depends not only on their size and location, but how easy they will be to sell if the lender has to take possession. CAN I SELL HALF OF MY HOUSE TO MY DAUGHTER OR SON? The other option would be to "sell" the property to your son, and retain a legal interest in the property. This would be a 'concessionary sale' and not every lender will look at this type of scenario, however as John Charcol is an independent, whole of market broker, we have excellent relationships with those lenders who shouldbe able to help.

CAN I GET A MORTGAGE FOR A PROPERTY WITHOUT A WATER SUPPLY A private water supply is one which is not provided by a water company. For properties that do have a private water supply, Defra has put together a guide on buying a house with a private water supply, which you can read. If you'd like to let us know a bit more and the property and its location on 03304 332 927 then we'll see what can bedone.

MY EX WON'T PAY HIS HALF OF THE MORTGAGE WHAT CAN I DO? Speak to your lender as soon as your ex-partner indicates they won’t be maintaining their share of the mortgage payment. Lenders sometimes show leniency on cases where they’re kept updated. Some lenders may even consider reducing your monthly payments by converting to interest-only or extending the term. Other options if your ex-partnerJOHN CHARCOL

John Charcol is the original independent mortgage broker. We have over 40 years’ experience in finding the best mortgage rates for every type of buyer. Whether you’re investing in property or looking to buy your first home, we can help. Our expert, independent mortgage advice will make buying your home or property investment easy. CAPITAL GAINS TAX CALCULATOR UK 2020 Our Capital Gains Tax calculator gives you an estimate of how much you could have to pay in Capital Gains Tax (CGT) when you sell your property in the UK. Simply enter your total earnings, the sale and purchase price of the property and your tax-deductible expenses and click the Calculate button. CGT tax deductible expenses include: StampDuty

GUIDE TO LIMITED COMPANY BUY-TO-LET as now transitional rates new 2016/17 2017/18 2018/19 2019/20 2020 onwards rental income £15,000 £15,000 £15,000 £15,000 £15,000 mortgage interest £10,800 £10,800 £10,800 £10,800 £10,800 reduction in mortgagae interest allowance MORTGAGE LOAN-TO-VALUE CALCULATOR 2020 How to Calculate LTV for Mortgage. You want to buy a house for �400,000. You have £80,000 in savings that you want to put down as a deposit. You take out a mortgage/loan to cover the remaining amount: �400,000 - £80,000 = £320,000. Your LTV is 80%: (£320,000 – 400,000) x 100 = 80. CAPITAL GAINS TAX ON SECOND HOMES Your new income is above £50,000 and so falls into the higher rate tax band: You pay 18% CGT on the taxable gains above £45,000 and up to £50,000: (£50,000 - £45,000) = £5,000. 18% of £5,000 (£5,000 x 0.18) = £900 in CGT. You pay 28% CGT on the taxable gains on the amount above £50,000: (£133,000 - £50,000) = £83,000. HOW CAN I BUY A HOUSE WHEN I HAVEN'T SOLD MY CURRENT Again you will need to make sure that the new mortgage gives you the flexibility to reduce the amount outstanding once you have sold your current home without being penalised. I believe we can help you and that you would benefit from speaking to one of our independent mortgage advisers. Please call 03304 332 927 and one of our adviserswill

WHAT IS THE MINIMUM SIZE FOR A FLAT TO GET A The usual minimum for a studio flat to be acceptable for a mortgage is 30 sq metres. There are a couple of lenders who do not state a minimum size for studio flats because their suitability as security depends not only on their size and location, but how easy they will be to sell if the lender has to take possession. CAN I SELL HALF OF MY HOUSE TO MY DAUGHTER OR SON? The other option would be to "sell" the property to your son, and retain a legal interest in the property. This would be a 'concessionary sale' and not every lender will look at this type of scenario, however as John Charcol is an independent, whole of market broker, we have excellent relationships with those lenders who shouldbe able to help.

CAN I GET A MORTGAGE FOR A PROPERTY WITHOUT A WATER SUPPLY A private water supply is one which is not provided by a water company. For properties that do have a private water supply, Defra has put together a guide on buying a house with a private water supply, which you can read. If you'd like to let us know a bit more and the property and its location on 03304 332 927 then we'll see what can bedone.

MY EX WON'T PAY HIS HALF OF THE MORTGAGE WHAT CAN I DO? Speak to your lender as soon as your ex-partner indicates they won’t be maintaining their share of the mortgage payment. Lenders sometimes show leniency on cases where they’re kept updated. Some lenders may even consider reducing your monthly payments by converting to interest-only or extending the term. Other options if your ex-partner CAPITAL GAINS TAX UK PROPERTY Capital Gains Tax Allowance on Property. The Capital Gains tax allowance on property for 2021 - 2022 is £12,300. This means you don’t pay any CGT on the first £12,300 you earn from the sale of your property. Example. Following on from the previous OFFSET MORTGAGES: ARE THEY MAKING A POST-COVID COMEBACK Legal . YOUR PROPERTY MAY BE REPOSSESSED IF YOU DO NOT KEEP UP REPAYMENTS ON A MORTGAGE OR ANY DEBT SECURED ON IT. John Charcol is a trading name of John Charcol Limited and its AppointedRepresentatives.

CAPITAL GAINS TAX CALCULATOR UK 2020 Our Capital Gains Tax calculator gives you an estimate of how much you could have to pay in Capital Gains Tax (CGT) when you sell your property in the UK. Simply enter your total earnings, the sale and purchase price of the property and your tax-deductible expenses and click the Calculate button. CGT tax deductible expenses include: StampDuty

CAPITAL GAINS TAX ON SECOND HOMES Your new income is above £50,000 and so falls into the higher rate tax band: You pay 18% CGT on the taxable gains above £45,000 and up to £50,000: (£50,000 - £45,000) = £5,000. 18% of £5,000 (£5,000 x 0.18) = £900 in CGT. You pay 28% CGT on the taxable gains on the amount above £50,000: (£133,000 - £50,000) = £83,000. BUY-TO-LET LIMITED COMPANY: SETTING UP & ADVICE An individual who sells a buy-to-let receives a certain allowance – i.e. an amount they don’t pay CGT on. If a private landlord sold their property within the 2020 - 2021 tax year or the 2021 - 2022 tax year, they would receive an allowance of £12,300. A private STAMP DUTY ON SECOND HOME 2021: SECOND HOUSE TAX You’re purchasing a second home for £700,000. The maximum rate of Stamp Duty you’ll pay is 8% but this is only for the portion of your property value over £500,000 - i.e. £200,000. You pay Additional Stamp Duty at 3% on the first £500,000 and some at 8% on the remaining £200,000. You’ll pay: 3% on the first £500,000 of the�700,000

ENQUIRE NOW

Enquire today to get the latest advice, support and news about mortgages and property from our John Charcol mortgage experts. LANDLORDS AND FINANCE COSTS RESTRICTION: WHAT’S DEDUCTIBLE You can deduct 25% of your finance costs payment from your rental income. 25% of £10,800 = £2,700. £15,000 - £2,700 = £12,300. Your Income Tax rate is applied to your remaining rental income. 40% of �12,300 = £4,920. You receive Allowable Tax Relief at 20% on the remaining 75% of finance costs. 75% of £10,800 = £8,100. CAN I SELL PART OF MY LAND IF I HAVE A MORTGAGE? Legal . YOUR PROPERTY MAY BE REPOSSESSED IF YOU DO NOT KEEP UP REPAYMENTS ON A MORTGAGE OR ANY DEBT SECURED ON IT. John Charcol is a trading name of John Charcol Limited and its AppointedRepresentatives.

CAN MY NAME BE TAKEN OFF A JOINT MORTGAGE WITHOUT MY As you cannot be named on the title deeds without also being on the mortgage, your ex-partner will need to have you removed from the title deeds first or at least at the same time that they have you removed from the mortgage. Some lenders will allow you to stay on a mortgage but not on the title deeds. This may be suitable in certainsituations.

JOHN CHARCOL

John Charcol is the original independent mortgage broker. We have over 40 years’ experience in finding the best mortgage rates for every type of buyer. Whether you’re investing in property or looking to buy your first home, we can help. Our expert, independent mortgage advice will make buying your home or property investment easy. CAPITAL GAINS TAX UK PROPERTY Capital Gains Tax Allowance on Property. The Capital Gains tax allowance on property for 2021 - 2022 is £12,300. This means you don’t pay any CGT on the first £12,300 you earn from the sale of your property. Example. Following on from the previous STAMP DUTY ON SECOND HOME 2021: SECOND HOUSE TAX You’re purchasing a second home for £700,000. The maximum rate of Stamp Duty you’ll pay is 8% but this is only for the portion of your property value over £500,000 - i.e. £200,000. You pay Additional Stamp Duty at 3% on the first £500,000 and some at 8% on the remaining £200,000. You’ll pay: 3% on the first £500,000 of the�700,000

GUIDE TO LIMITED COMPANY BUY-TO-LET as now transitional rates new 2016/17 2017/18 2018/19 2019/20 2020 onwards rental income £15,000 £15,000 £15,000 £15,000 £15,000 mortgage interest £10,800 £10,800 £10,800 £10,800 £10,800 reduction in mortgagae interest allowance HOW CAN I BUY A HOUSE WHEN I HAVEN'T SOLD MY CURRENT Again you will need to make sure that the new mortgage gives you the flexibility to reduce the amount outstanding once you have sold your current home without being penalised. I believe we can help you and that you would benefit from speaking to one of our independent mortgage advisers. Please call 03304 332 927 and one of our adviserswill

GETTING THE SUMS RIGHT For example, let’s assume that school fees for one of my client’s children is £20,000 per year for five years, so £100,000 in total. If that were to be paid monthly over those five years then my client would be paying £1,666 per month (plus all the other background costs, e.g. school trips, uniform, meals, etc). If that same client CAN I REMORTGAGE A RIGHT TO BUY PROPERTY? The Right to Buy is a government scheme in England. The property discount can be up to 70% or £110,500 in London and £82,800 for properties outside London. The discount you could potentially receive depends on: How long you’ve been a tenant with a CAN I GET A MORTGAGE FOR A PROPERTY WITHOUT A WATER SUPPLY A private water supply is one which is not provided by a water company. For properties that do have a private water supply, Defra has put together a guide on buying a house with a private water supply, which you can read. If you'd like to let us know a bit more and the property and its location on 03304 332 927 then we'll see what can bedone.

CAN I SELL HALF OF MY HOUSE TO MY DAUGHTER OR SON? The other option would be to "sell" the property to your son, and retain a legal interest in the property. This would be a 'concessionary sale' and not every lender will look at this type of scenario, however as John Charcol is an independent, whole of market broker, we have excellent relationships with those lenders who shouldbe able to help.

ARE YOU BREACHING YOUR MORTGAGE TERMS RENTING OUT YOUR Lenders may prefer to initially give you a warning. "I suspect that in practice, if a lender discovered an historic breach it would write reminding its customer of the terms of their mortgage and spell out the need to get permission if they want to use Airbnb or a similar site in the future," says Boulger. "If the borrower wanted to do thatJOHN CHARCOL

John Charcol is the original independent mortgage broker. We have over 40 years’ experience in finding the best mortgage rates for every type of buyer. Whether you’re investing in property or looking to buy your first home, we can help. Our expert, independent mortgage advice will make buying your home or property investment easy. CAPITAL GAINS TAX UK PROPERTY Capital Gains Tax Allowance on Property. The Capital Gains tax allowance on property for 2021 - 2022 is £12,300. This means you don’t pay any CGT on the first £12,300 you earn from the sale of your property. Example. Following on from the previous STAMP DUTY ON SECOND HOME 2021: SECOND HOUSE TAX You’re purchasing a second home for £700,000. The maximum rate of Stamp Duty you’ll pay is 8% but this is only for the portion of your property value over £500,000 - i.e. £200,000. You pay Additional Stamp Duty at 3% on the first £500,000 and some at 8% on the remaining £200,000. You’ll pay: 3% on the first £500,000 of the�700,000

GUIDE TO LIMITED COMPANY BUY-TO-LET as now transitional rates new 2016/17 2017/18 2018/19 2019/20 2020 onwards rental income £15,000 £15,000 £15,000 £15,000 £15,000 mortgage interest £10,800 £10,800 £10,800 £10,800 £10,800 reduction in mortgagae interest allowance HOW CAN I BUY A HOUSE WHEN I HAVEN'T SOLD MY CURRENT Again you will need to make sure that the new mortgage gives you the flexibility to reduce the amount outstanding once you have sold your current home without being penalised. I believe we can help you and that you would benefit from speaking to one of our independent mortgage advisers. Please call 03304 332 927 and one of our adviserswill

GETTING THE SUMS RIGHT For example, let’s assume that school fees for one of my client’s children is £20,000 per year for five years, so £100,000 in total. If that were to be paid monthly over those five years then my client would be paying £1,666 per month (plus all the other background costs, e.g. school trips, uniform, meals, etc). If that same client CAN I REMORTGAGE A RIGHT TO BUY PROPERTY? The Right to Buy is a government scheme in England. The property discount can be up to 70% or £110,500 in London and £82,800 for properties outside London. The discount you could potentially receive depends on: How long you’ve been a tenant with a CAN I GET A MORTGAGE FOR A PROPERTY WITHOUT A WATER SUPPLY A private water supply is one which is not provided by a water company. For properties that do have a private water supply, Defra has put together a guide on buying a house with a private water supply, which you can read. If you'd like to let us know a bit more and the property and its location on 03304 332 927 then we'll see what can bedone.

CAN I SELL HALF OF MY HOUSE TO MY DAUGHTER OR SON? The other option would be to "sell" the property to your son, and retain a legal interest in the property. This would be a 'concessionary sale' and not every lender will look at this type of scenario, however as John Charcol is an independent, whole of market broker, we have excellent relationships with those lenders who shouldbe able to help.

ARE YOU BREACHING YOUR MORTGAGE TERMS RENTING OUT YOUR Lenders may prefer to initially give you a warning. "I suspect that in practice, if a lender discovered an historic breach it would write reminding its customer of the terms of their mortgage and spell out the need to get permission if they want to use Airbnb or a similar site in the future," says Boulger. "If the borrower wanted to do that CAPITAL GAINS TAX UK PROPERTY Capital Gains Tax Allowance on Property. The Capital Gains tax allowance on property for 2021 - 2022 is £12,300. This means you don’t pay any CGT on the first £12,300 you earn from the sale of your property. Example. Following on from the previous OFFSET MORTGAGES: ARE THEY MAKING A POST-COVID COMEBACK Legal . YOUR PROPERTY MAY BE REPOSSESSED IF YOU DO NOT KEEP UP REPAYMENTS ON A MORTGAGE OR ANY DEBT SECURED ON IT. John Charcol is a trading name of John Charcol Limited and its AppointedRepresentatives.

CAPITAL GAINS TAX CALCULATOR UK 2020 Our Capital Gains Tax calculator gives you an estimate of how much you could have to pay in Capital Gains Tax (CGT) when you sell your property in the UK. Simply enter your total earnings, the sale and purchase price of the property and your tax-deductible expenses and click the Calculate button. CGT tax deductible expenses include: StampDuty

BUY-TO-LET LIMITED COMPANY: SETTING UP & ADVICE An individual who sells a buy-to-let receives a certain allowance – i.e. an amount they don’t pay CGT on. If a private landlord sold their property within the 2020 - 2021 tax year or the 2021 - 2022 tax year, they would receive an allowance of £12,300. A privateENQUIRE NOW

Enquire today to get the latest advice, support and news about mortgages and property from our John Charcol mortgage experts. MORTGAGE LOAN-TO-VALUE CALCULATOR 2020 How to Calculate LTV for Mortgage. You want to buy a house for �400,000. You have £80,000 in savings that you want to put down as a deposit. You take out a mortgage/loan to cover the remaining amount: �400,000 - £80,000 = £320,000. Your LTV is 80%: (£320,000 – 400,000) x 100 = 80. GUARANTOR MORTGAGES FOR FIRST-TIME BUYERS 2021 Guarantor mortgages are loans which are secured against the property you’re buying. You have to put down a deposit just like you would with any other mortgage. They're usually repayment mortgages as they’re primarily taken out by first-time buyers. With a repayment mortgage, you pay back a bit of your mortgage balance each month, withinterest.

TENANTS IN COMMON MEANING & HOW TO CHANGE Tenants in Common Meaning. To be tenants in common you must be part of a tenancy in common agreement. A tenancy in common agreement is a situation in which 2 or more people hold interest in a property and each owner has the right to leave their share of the property to a GUIDE TO LIMITED COMPANY BUY-TO-LET as now transitional rates new 2016/17 2017/18 2018/19 2019/20 2020 onwards rental income £15,000 £15,000 £15,000 £15,000 £15,000 mortgage interest £10,800 £10,800 £10,800 £10,800 £10,800 reduction in mortgagae interest allowance CAPITAL GAINS TAX ON SECOND HOMES Your new income is above £50,000 and so falls into the higher rate tax band: You pay 18% CGT on the taxable gains above £45,000 and up to £50,000: (£50,000 - £45,000) = £5,000. 18% of £5,000 (£5,000 x 0.18) = £900 in CGT. You pay 28% CGT on the taxable gains on the amount above £50,000: (£133,000 - £50,000) = £83,000.JOHN CHARCOL

John Charcol is the original independent mortgage broker. We have over 40 years’ experience in finding the best mortgage rates for every type of buyer. Whether you’re investing in property or looking to buy your first home, we can help. Our expert, independent mortgage advice will make buying your home or property investment easy. CAPITAL GAINS TAX UK PROPERTY Capital Gains Tax Allowance on Property. The Capital Gains tax allowance on property for 2021 - 2022 is £12,300. This means you don’t pay any CGT on the first £12,300 you earn from the sale of your property. Example. Following on from the previous STAMP DUTY ON SECOND HOME 2021: SECOND HOUSE TAX You’re purchasing a second home for £700,000. The maximum rate of Stamp Duty you’ll pay is 8% but this is only for the portion of your property value over £500,000 - i.e. £200,000. You pay Additional Stamp Duty at 3% on the first £500,000 and some at 8% on the remaining £200,000. You’ll pay: 3% on the first £500,000 of the�700,000

GUIDE TO LIMITED COMPANY BUY-TO-LET as now transitional rates new 2016/17 2017/18 2018/19 2019/20 2020 onwards rental income £15,000 £15,000 £15,000 £15,000 £15,000 mortgage interest £10,800 £10,800 £10,800 £10,800 £10,800 reduction in mortgagae interest allowance HOW CAN I BUY A HOUSE WHEN I HAVEN'T SOLD MY CURRENT Again you will need to make sure that the new mortgage gives you the flexibility to reduce the amount outstanding once you have sold your current home without being penalised. I believe we can help you and that you would benefit from speaking to one of our independent mortgage advisers. Please call 03304 332 927 and one of our adviserswill

GETTING THE SUMS RIGHT For example, let’s assume that school fees for one of my client’s children is £20,000 per year for five years, so £100,000 in total. If that were to be paid monthly over those five years then my client would be paying £1,666 per month (plus all the other background costs, e.g. school trips, uniform, meals, etc). If that same client CAN I REMORTGAGE A RIGHT TO BUY PROPERTY? The Right to Buy is a government scheme in England. The property discount can be up to 70% or £110,500 in London and £82,800 for properties outside London. The discount you could potentially receive depends on: How long you’ve been a tenant with a CAN I GET A MORTGAGE FOR A PROPERTY WITHOUT A WATER SUPPLY A private water supply is one which is not provided by a water company. For properties that do have a private water supply, Defra has put together a guide on buying a house with a private water supply, which you can read. If you'd like to let us know a bit more and the property and its location on 03304 332 927 then we'll see what can bedone.

CAN I SELL HALF OF MY HOUSE TO MY DAUGHTER OR SON? The other option would be to "sell" the property to your son, and retain a legal interest in the property. This would be a 'concessionary sale' and not every lender will look at this type of scenario, however as John Charcol is an independent, whole of market broker, we have excellent relationships with those lenders who shouldbe able to help.

ARE YOU BREACHING YOUR MORTGAGE TERMS RENTING OUT YOUR Lenders may prefer to initially give you a warning. "I suspect that in practice, if a lender discovered an historic breach it would write reminding its customer of the terms of their mortgage and spell out the need to get permission if they want to use Airbnb or a similar site in the future," says Boulger. "If the borrower wanted to do thatJOHN CHARCOL

John Charcol is the original independent mortgage broker. We have over 40 years’ experience in finding the best mortgage rates for every type of buyer. Whether you’re investing in property or looking to buy your first home, we can help. Our expert, independent mortgage advice will make buying your home or property investment easy. CAPITAL GAINS TAX UK PROPERTY Capital Gains Tax Allowance on Property. The Capital Gains tax allowance on property for 2021 - 2022 is £12,300. This means you don’t pay any CGT on the first £12,300 you earn from the sale of your property. Example. Following on from the previous STAMP DUTY ON SECOND HOME 2021: SECOND HOUSE TAX You’re purchasing a second home for £700,000. The maximum rate of Stamp Duty you’ll pay is 8% but this is only for the portion of your property value over £500,000 - i.e. £200,000. You pay Additional Stamp Duty at 3% on the first £500,000 and some at 8% on the remaining £200,000. You’ll pay: 3% on the first £500,000 of the�700,000

GUIDE TO LIMITED COMPANY BUY-TO-LET as now transitional rates new 2016/17 2017/18 2018/19 2019/20 2020 onwards rental income £15,000 £15,000 £15,000 £15,000 £15,000 mortgage interest £10,800 £10,800 £10,800 £10,800 £10,800 reduction in mortgagae interest allowance HOW CAN I BUY A HOUSE WHEN I HAVEN'T SOLD MY CURRENT Again you will need to make sure that the new mortgage gives you the flexibility to reduce the amount outstanding once you have sold your current home without being penalised. I believe we can help you and that you would benefit from speaking to one of our independent mortgage advisers. Please call 03304 332 927 and one of our adviserswill

GETTING THE SUMS RIGHT For example, let’s assume that school fees for one of my client’s children is £20,000 per year for five years, so £100,000 in total. If that were to be paid monthly over those five years then my client would be paying £1,666 per month (plus all the other background costs, e.g. school trips, uniform, meals, etc). If that same client CAN I REMORTGAGE A RIGHT TO BUY PROPERTY? The Right to Buy is a government scheme in England. The property discount can be up to 70% or £110,500 in London and £82,800 for properties outside London. The discount you could potentially receive depends on: How long you’ve been a tenant with a CAN I GET A MORTGAGE FOR A PROPERTY WITHOUT A WATER SUPPLY A private water supply is one which is not provided by a water company. For properties that do have a private water supply, Defra has put together a guide on buying a house with a private water supply, which you can read. If you'd like to let us know a bit more and the property and its location on 03304 332 927 then we'll see what can bedone.

CAN I SELL HALF OF MY HOUSE TO MY DAUGHTER OR SON? The other option would be to "sell" the property to your son, and retain a legal interest in the property. This would be a 'concessionary sale' and not every lender will look at this type of scenario, however as John Charcol is an independent, whole of market broker, we have excellent relationships with those lenders who shouldbe able to help.

ARE YOU BREACHING YOUR MORTGAGE TERMS RENTING OUT YOUR Lenders may prefer to initially give you a warning. "I suspect that in practice, if a lender discovered an historic breach it would write reminding its customer of the terms of their mortgage and spell out the need to get permission if they want to use Airbnb or a similar site in the future," says Boulger. "If the borrower wanted to do that CAPITAL GAINS TAX UK PROPERTY Capital Gains Tax Allowance on Property. The Capital Gains tax allowance on property for 2021 - 2022 is £12,300. This means you don’t pay any CGT on the first £12,300 you earn from the sale of your property. Example. Following on from the previous OFFSET MORTGAGES: ARE THEY MAKING A POST-COVID COMEBACK Legal . YOUR PROPERTY MAY BE REPOSSESSED IF YOU DO NOT KEEP UP REPAYMENTS ON A MORTGAGE OR ANY DEBT SECURED ON IT. John Charcol is a trading name of John Charcol Limited and its AppointedRepresentatives.

CAPITAL GAINS TAX CALCULATOR UK 2020 Our Capital Gains Tax calculator gives you an estimate of how much you could have to pay in Capital Gains Tax (CGT) when you sell your property in the UK. Simply enter your total earnings, the sale and purchase price of the property and your tax-deductible expenses and click the Calculate button. CGT tax deductible expenses include: StampDuty

BUY-TO-LET LIMITED COMPANY: SETTING UP & ADVICE An individual who sells a buy-to-let receives a certain allowance – i.e. an amount they don’t pay CGT on. If a private landlord sold their property within the 2020 - 2021 tax year or the 2021 - 2022 tax year, they would receive an allowance of £12,300. A privateENQUIRE NOW

Enquire today to get the latest advice, support and news about mortgages and property from our John Charcol mortgage experts. MORTGAGE LOAN-TO-VALUE CALCULATOR 2020 How to Calculate LTV for Mortgage. You want to buy a house for �400,000. You have £80,000 in savings that you want to put down as a deposit. You take out a mortgage/loan to cover the remaining amount: �400,000 - £80,000 = £320,000. Your LTV is 80%: (£320,000 – 400,000) x 100 = 80. GUARANTOR MORTGAGES FOR FIRST-TIME BUYERS 2021 Guarantor mortgages are loans which are secured against the property you’re buying. You have to put down a deposit just like you would with any other mortgage. They're usually repayment mortgages as they’re primarily taken out by first-time buyers. With a repayment mortgage, you pay back a bit of your mortgage balance each month, withinterest.

TENANTS IN COMMON MEANING & HOW TO CHANGE Tenants in Common Meaning. To be tenants in common you must be part of a tenancy in common agreement. A tenancy in common agreement is a situation in which 2 or more people hold interest in a property and each owner has the right to leave their share of the property to a GUIDE TO LIMITED COMPANY BUY-TO-LET as now transitional rates new 2016/17 2017/18 2018/19 2019/20 2020 onwards rental income £15,000 £15,000 £15,000 £15,000 £15,000 mortgage interest £10,800 £10,800 £10,800 £10,800 £10,800 reduction in mortgagae interest allowance CAPITAL GAINS TAX ON SECOND HOMES Your new income is above £50,000 and so falls into the higher rate tax band: You pay 18% CGT on the taxable gains above £45,000 and up to £50,000: (£50,000 - £45,000) = £5,000. 18% of £5,000 (£5,000 x 0.18) = £900 in CGT. You pay 28% CGT on the taxable gains on the amount above £50,000: (£133,000 - £50,000) = £83,000.JOHN CHARCOL

John Charcol is the original independent mortgage broker. We have over 40 years’ experience in finding the best mortgage rates for every type of buyer. Whether you’re investing in property or looking to buy your first home, we can help. Our expert, independent mortgage advice will make buying your home or property investment easy. CAPITAL GAINS TAX UK PROPERTY Capital Gains Tax Allowance on Property. The Capital Gains tax allowance on property for 2021 - 2022 is £12,300. This means you don’t pay any CGT on the first £12,300 you earn from the sale of your property. Example. Following on from the previous MORTGAGE LOAN-TO-VALUE CALCULATOR 2020 How to Calculate LTV for Mortgage. You want to buy a house for �400,000. You have £80,000 in savings that you want to put down as a deposit. You take out a mortgage/loan to cover the remaining amount: �400,000 - £80,000 = £320,000. Your LTV is 80%: (£320,000 – 400,000) x 100 = 80. STAMP DUTY ON SECOND HOME 2021: SECOND HOUSE TAX You’re purchasing a second home for £700,000. The maximum rate of Stamp Duty you’ll pay is 8% but this is only for the portion of your property value over £500,000 - i.e. £200,000. You pay Additional Stamp Duty at 3% on the first £500,000 and some at 8% on the remaining £200,000. You’ll pay: 3% on the first £500,000 of the�700,000

TENANTS IN COMMON MEANING & HOW TO CHANGE Tenants in Common Meaning. To be tenants in common you must be part of a tenancy in common agreement. A tenancy in common agreement is a situation in which 2 or more people hold interest in a property and each owner has the right to leave their share of the property to a CAPITAL GAINS TAX ON SECOND HOMES Your new income is above £50,000 and so falls into the higher rate tax band: You pay 18% CGT on the taxable gains above £45,000 and up to £50,000: (£50,000 - £45,000) = £5,000. 18% of £5,000 (£5,000 x 0.18) = £900 in CGT. You pay 28% CGT on the taxable gains on the amount above £50,000: (£133,000 - £50,000) = £83,000. GETTING THE SUMS RIGHT For example, let’s assume that school fees for one of my client’s children is £20,000 per year for five years, so £100,000 in total. If that were to be paid monthly over those five years then my client would be paying £1,666 per month (plus all the other background costs, e.g. school trips, uniform, meals, etc). If that same client CAN I SELL HALF OF MY HOUSE TO MY DAUGHTER OR SON? The other option would be to "sell" the property to your son, and retain a legal interest in the property. This would be a 'concessionary sale' and not every lender will look at this type of scenario, however as John Charcol is an independent, whole of market broker, we have excellent relationships with those lenders who shouldbe able to help.

CAN I GET A MORTGAGE FOR A PROPERTY WITHOUT A WATER SUPPLY A private water supply is one which is not provided by a water company. For properties that do have a private water supply, Defra has put together a guide on buying a house with a private water supply, which you can read. If you'd like to let us know a bit more and the property and its location on 03304 332 927 then we'll see what can bedone.

MY EX WON'T PAY HIS HALF OF THE MORTGAGE WHAT CAN I DO? Speak to your lender as soon as your ex-partner indicates they won’t be maintaining their share of the mortgage payment. Lenders sometimes show leniency on cases where they’re kept updated. Some lenders may even consider reducing your monthly payments by converting to interest-only or extending the term. Other options if your ex-partnerJOHN CHARCOL

John Charcol is the original independent mortgage broker. We have over 40 years’ experience in finding the best mortgage rates for every type of buyer. Whether you’re investing in property or looking to buy your first home, we can help. Our expert, independent mortgage advice will make buying your home or property investment easy. CAPITAL GAINS TAX UK PROPERTY Capital Gains Tax Allowance on Property. The Capital Gains tax allowance on property for 2021 - 2022 is £12,300. This means you don’t pay any CGT on the first £12,300 you earn from the sale of your property. Example. Following on from the previous MORTGAGE LOAN-TO-VALUE CALCULATOR 2020 How to Calculate LTV for Mortgage. You want to buy a house for �400,000. You have £80,000 in savings that you want to put down as a deposit. You take out a mortgage/loan to cover the remaining amount: �400,000 - £80,000 = £320,000. Your LTV is 80%: (£320,000 – 400,000) x 100 = 80. STAMP DUTY ON SECOND HOME 2021: SECOND HOUSE TAX You’re purchasing a second home for £700,000. The maximum rate of Stamp Duty you’ll pay is 8% but this is only for the portion of your property value over £500,000 - i.e. £200,000. You pay Additional Stamp Duty at 3% on the first £500,000 and some at 8% on the remaining £200,000. You’ll pay: 3% on the first £500,000 of the�700,000

TENANTS IN COMMON MEANING & HOW TO CHANGE Tenants in Common Meaning. To be tenants in common you must be part of a tenancy in common agreement. A tenancy in common agreement is a situation in which 2 or more people hold interest in a property and each owner has the right to leave their share of the property to a CAPITAL GAINS TAX ON SECOND HOMES Your new income is above £50,000 and so falls into the higher rate tax band: You pay 18% CGT on the taxable gains above £45,000 and up to £50,000: (£50,000 - £45,000) = £5,000. 18% of £5,000 (£5,000 x 0.18) = £900 in CGT. You pay 28% CGT on the taxable gains on the amount above £50,000: (£133,000 - £50,000) = £83,000. GETTING THE SUMS RIGHT For example, let’s assume that school fees for one of my client’s children is £20,000 per year for five years, so £100,000 in total. If that were to be paid monthly over those five years then my client would be paying £1,666 per month (plus all the other background costs, e.g. school trips, uniform, meals, etc). If that same client CAN I SELL HALF OF MY HOUSE TO MY DAUGHTER OR SON? The other option would be to "sell" the property to your son, and retain a legal interest in the property. This would be a 'concessionary sale' and not every lender will look at this type of scenario, however as John Charcol is an independent, whole of market broker, we have excellent relationships with those lenders who shouldbe able to help.

CAN I GET A MORTGAGE FOR A PROPERTY WITHOUT A WATER SUPPLY A private water supply is one which is not provided by a water company. For properties that do have a private water supply, Defra has put together a guide on buying a house with a private water supply, which you can read. If you'd like to let us know a bit more and the property and its location on 03304 332 927 then we'll see what can bedone.

MY EX WON'T PAY HIS HALF OF THE MORTGAGE WHAT CAN I DO? Speak to your lender as soon as your ex-partner indicates they won’t be maintaining their share of the mortgage payment. Lenders sometimes show leniency on cases where they’re kept updated. Some lenders may even consider reducing your monthly payments by converting to interest-only or extending the term. Other options if your ex-partner OFFSET MORTGAGES: ARE THEY MAKING A POST-COVID COMEBACK Legal . YOUR PROPERTY MAY BE REPOSSESSED IF YOU DO NOT KEEP UP REPAYMENTS ON A MORTGAGE OR ANY DEBT SECURED ON IT. John Charcol is a trading name of John Charcol Limited and its AppointedRepresentatives.

CAPITAL GAINS TAX CALCULATOR UK 2020 Our Capital Gains Tax calculator gives you an estimate of how much you could have to pay in Capital Gains Tax (CGT) when you sell your property in the UK. Simply enter your total earnings, the sale and purchase price of the property and your tax-deductible expenses and click the Calculate button. CGT tax deductible expenses include: StampDuty

GUIDE TO LIMITED COMPANY BUY-TO-LET as now transitional rates new 2016/17 2017/18 2018/19 2019/20 2020 onwards rental income £15,000 £15,000 £15,000 £15,000 £15,000 mortgage interest £10,800 £10,800 £10,800 £10,800 £10,800 reduction in mortgagae interest allowance BUY-TO-LET LIMITED COMPANY: SETTING UP & ADVICE An individual who sells a buy-to-let receives a certain allowance – i.e. an amount they don’t pay CGT on. If a private landlord sold their property within the 2020 - 2021 tax year or the 2021 - 2022 tax year, they would receive an allowance of £12,300. A private CAPITAL GAINS TAX ON SECOND HOMES Your new income is above £50,000 and so falls into the higher rate tax band: You pay 18% CGT on the taxable gains above £45,000 and up to £50,000: (£50,000 - £45,000) = £5,000. 18% of £5,000 (£5,000 x 0.18) = £900 in CGT. You pay 28% CGT on the taxable gains on the amount above £50,000: (£133,000 - £50,000) = £83,000. RENTAL YIELD CALCULATOR: HOW TO WORK OUT RENTAL YIELD Rental yield = (Monthly rental income x 12) ÷ Property value. We’ve broken down how you use this formula to calculate rental yield below: Take the monthly rental income amount or expected rental income and multiply it by 12. Divide it by the property’s purchase price or current market value. Multiply this figure by 100 to get thepercentage.

HOW CAN I BUY A HOUSE WHEN I HAVEN'T SOLD MY CURRENT Again you will need to make sure that the new mortgage gives you the flexibility to reduce the amount outstanding once you have sold your current home without being penalised. I believe we can help you and that you would benefit from speaking to one of our independent mortgage advisers. Please call 03304 332 927 and one of our adviserswill

CAN I REMORTGAGE A RIGHT TO BUY PROPERTY? The Right to Buy is a government scheme in England. The property discount can be up to 70% or £110,500 in London and £82,800 for properties outside London. The discount you could potentially receive depends on: How long you’ve been a tenant with a IS IT DIFFICULT TO SPLIT THE FREEHOLD TITLE? Placing a Split on the Freehold Title. A freehold is the permanent and absolute tenure of land or property. By buying a freehold property, it means you own that property and the land on which it stands outright. Meaning that it is completely owned by you unless you decide to sell it. It's unclear as to why your current broker is having trouble CAN MY NAME BE TAKEN OFF A JOINT MORTGAGE WITHOUT MY As you cannot be named on the title deeds without also being on the mortgage, your ex-partner will need to have you removed from the title deeds first or at least at the same time that they have you removed from the mortgage. Some lenders will allow you to stay on a mortgage but not on the title deeds. This may be suitable in certainsituations.

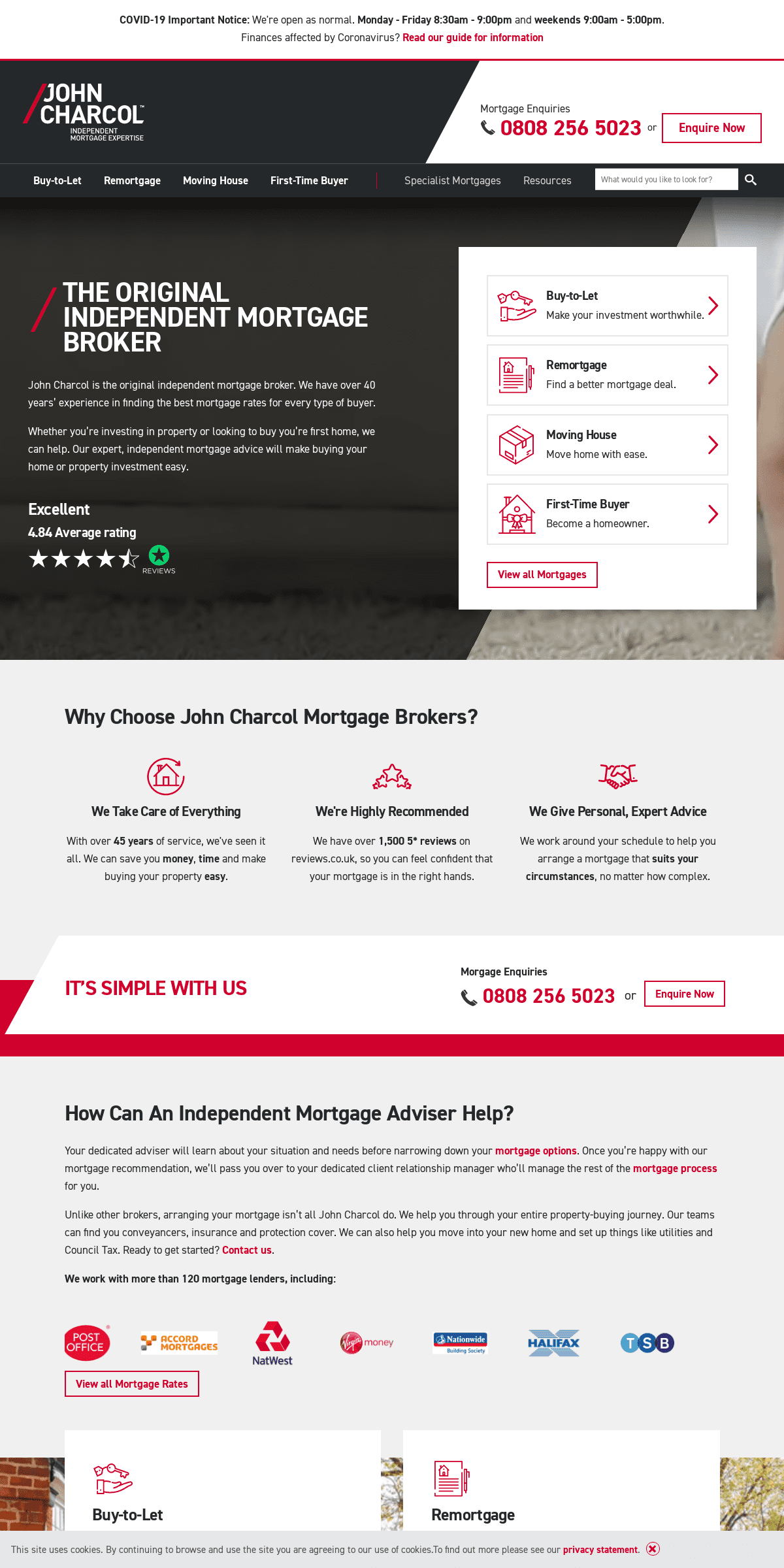

COVID-19 IMPORTANT NOTICE: We're open as normal. MONDAY - FRIDAY 8:30AM - 9:00PM and WEEKENDS 9:00AM - 5:00PM. Finances affected by Coronavirus? Read our guide for information* Enquire Now

* Menu

Mortgage Enquiries0808 256 5023orEnquire Now* Home

HOME

* Buy-to-Let

BUY-TO-LET

Turn your property into a worthwhile investment.*

* Mortgages

* Buy-to-Let Mortgages * LTD Company Buy-to-Let Mortgages * Buy-to-Let Remortgages * Portfolio Landlord Mortgages*

* Guides

* Buy-to-Let Guide

* LTD Company Buy-to-Let Guide * Buy-to-Let Tax Changes * Tax on Rental Income * Capital Gains Tax Guide * Stamp Duty on Second Homes*

* Tools

* Buy-to-Let Mortgage Calculator * Buy-to-Let Rent Calculator * Rental Yield Calculator * Capital Gains Tax Calculator * Buy-to-Let Stamp Duty Calculator* Remortgage

REMORTGAGE

Change your mortgage deal for your current property.*

* Mortgages

* Remortgage Deals

*

* Guides

* Remortgaging Guide * Funding Home Improvements * Guide to Second Property Mortgages*

* Tools

* Mortgage Rate Change Calculator * Mortgage Overpayment Calculator * Home Extension Calculator* Moving House

MOVING HOUSE

Manage your move and arrange your mortgage with ease.*

* Mortgages

* Moving House Mortgages * Fixed Rate Mortgages*

* Guides

* Moving Home Guide

* Buying a House Guide * Divorce and Mortgage Guide * Borrowing into Retirement * Property Finance for Expats* First-Time Buyer

FIRST-TIME BUYER

Take your first steps towards homeownership.*

* Mortgages

* First-Time Buyer Mortgages*

* Guides

* Buying Your First Home * How Much Deposit Do I Need? * Applying for A Mortgage* Help to Buy Guide

* Guarantor Mortgages* Tenants in Common

*

* Tools

* How Much Can I Borrow? * Loan to Value Calculator * Mortgage Repayment Calculator * Right to Buy Calculator* Spacer

* Specialist Mortgages SPECIALIST MORTGAGES Understand all of your options, no matter how complex.*

* Mortgages

* Second-Charge Mortgages * Commercial Mortgages * Freelance and Self-Employed Mortgages * Contractor Mortgages* Bridging Loans

* Expat Mortgages

* Offset Mortgages

* Development Finance * More Specialist Mortgages* Resources

RESOURCES

Find loads of useful information to support you on your property-buying journey.*

* News and Blog

* Mortgage and Property Blog * John Charcol in the News * Ray Boulger’s Blog*

* Support

* Mortgage Guides

* Mortgage Calculators * Ask the Mortgage Experts* Mortgage Glossary

* Mortgage Videos

* Search

SEARCH

Site searchSearch keyword(s): Search Site searchSearch keyword(s): Search THE ORIGINAL INDEPENDENT MORTGAGE BROKER THE ORIGINAL INDEPENDENT MORTGAGE BROKER John Charcol is the original independent mortgage broker. We have over 40 years’ experience in finding the best mortgage rates for everytype of buyer.

Whether you’re investing in property or looking to buy you’re first home, we can help. Our expert, independent mortgage advice will make buying your home or property investment easy.EXCELLENT

4.84 AVERAGE RATINGBUY-TO-LET

Make your investment worthwhile.REMORTGAGE

Find a better mortgage deal.MOVING HOUSE

Move home with ease.FIRST-TIME BUYER

Become a homeowner.

View all Mortgages

WHY CHOOSE JOHN CHARCOL MORTGAGE BROKERS? WE TAKE CARE OF EVERYTHING With over 45 YEARS of service, we've seen it all. We can save you MONEY, TIME and make buying your property EASY. WE'RE HIGHLY RECOMMENDED We have over 1,500 5* REVIEWS on reviews.co.uk, so you can feel confident that your mortgage is in the right hands. WE GIVE PERSONAL, EXPERT ADVICE We work around your schedule to help you arrange a mortgage that SUITS YOUR CIRCUMSTANCES, no matter how complex. IT’S SIMPLE WITH USMORGAGE ENQUIRIES

0808 256 5023 or

Enquire Now

HOW CAN AN INDEPENDENT MORTGAGE ADVISER HELP? Your dedicated adviser will learn about your situation and needs before narrowing down your mortgage options . Once you’re happy with our mortgage recommendation, we’ll pass you over to your dedicated client relationship manager who’ll manage the rest of the mortgage processfor you.

Unlike other brokers, arranging your mortgage isn’t all John Charcol do. We help you through your entire property-buying journey. Our teams can find you conveyancers, insurance and protection cover. We can also help you move into your new home and set up things like utilities and Council Tax. Ready to get started? Contact us . WE WORK WITH MORE THAN 120 MORTGAGE LENDERS, INCLUDING: View all Mortgage RatesBUY-TO-LET

Your mortgage will affect the profit potential of your buy-to-let investment. Use our free and easy best buy tool to compare currentmortgage rates.

Learn More

REMORTGAGE

Nearing the end of your fixed term? Or maybe it’s just time for a better rate? See what mortgages are on the market right now.Learn More

MOVING HOUSE

Let us take care of everything: the mortgage, the application, conveyancing, insurance, protection, removals, utilities. Make yourmove easy.

Learn More

FIRST-TIME BUYER

It doesn’t need to be complicated. We’ll guide you through, right up to the day you move in. Take your first step towards homeownershipnow.

Learn More

COMMERCIAL MORTGAGES Specific requirements? Need your portfolio packaged? We’re specialists in commercial mortgages.More Info

SELF-EMPLOYED MORTGAGES How will being self-employed affect your mortgage? Ask us. We’llexplain everything.

More Info

EXPAT MORTGAGES

It doesn’t matter how complex your case is. We’re experts. See howwe can help.

More Info

The kind of specialist mortgage you need will depend on your unique situation. We’re experts in a range of specialist mortgages: commercial, self-employed, expat, bridging, offset, second charge and more. We understand what you need. Ask us about your options. View all Specialist Mortgages WHAT OUR CUSTOMERS SAY WHAT OUR CUSTOMERS SAYJOHN CHARCOL

0330 057 5173 £

Cutlers Exchange, 123 Houndsditch London EC3A 7BUEXCELLENT

1770 Total reviews

90%

4.85 Average rating

*

5

★ ★ ★ ★ ★

ANONYMOUS

I have been working with John Charcol for many years and I have always had excellent service. Thanks to Sarah Dormer and Michelle Gilbert for their professional yet friendly approach, excellent communication skills and resilient. I am happy to recommend their services to everyone and I will not hesitate to use their service again.less I have been working with John Charcol for many years and I have always had excellent service. Thanks to Sarah Dormer and Michelle Gilbert for their professional yet friendly approach, excellent communication skills and resilient. I am happy to recommend their services to everyone and I will not hesitate to use their …morePosted 2 days ago

*

4

★ ★ ★ ★ ★

ANONYMOUS

I find John Charcol very accommodating and helpful.Posted 4 days ago

*

5

★ ★ ★ ★ ★

C

Such a smooth process. Steven was very responsive, efficient and kept us informed at all times. We're really happy with the mortgage we got.Posted 4 days ago

*

5

★ ★ ★ ★ ★

RICHARD

The staff were professional throughout the process and found a deal that was suitable to my needs.Posted 5 days ago

*

5

★ ★ ★ ★ ★

NICOLAS

I honestly cannot thank Daniel Bowles enough!!! From the bottom of my heart I cannot recommend him enough- the phrase 'going above and beyond' springs to mind. After I initially had a very poor credit rating, financial issues and basically been told by every other broker that I was unable to get a mortgage any time soon, Dan actually took the time in helping me and offering me phenomenal advice/support at the drop of a hat. Without Dan I would never be in the position where I am today (a first-time buyer) and getting on the ladder. After seeing how horrible the property market can be at time (aimed at Estate Agents) Dan & John Charcol were a breath of fresh air in my first property completion as you could actually tell Dan cared about customer service and finding the right product for YOU.less I honestly cannot thank Daniel Bowles enough!!! From the bottom of my heart I cannot recommend him enough- the phrase 'going above and beyond' springs to mind. After I initially had a very poor credit rating, financial issues and basically been told by every other broker that I was unable to get a mortgage any time soon, …morePosted 1 week ago

*

5

★ ★ ★ ★ ★

A

We have been working with John Charcol for the past few years and we have been always very satisfied with great service. Thanks to Sener for his very high level of professionalism and excellent communication skills. We are very happy to recommend John Charcol to anyone requiring mortgage broker services even in complicatedcircumstances.less

We have been working with John Charcol for the past few years and we have been always very satisfied with great service. Thanks to Sener for his very high level of professionalism and excellent communication skills. We are very happy to recommend John Charcol to anyone requiring mortgage broker services even in …morePosted 1 week ago

*

5

★ ★ ★ ★ ★

M

Excellent service from the first phone call to the final completion.Thank you.

Posted 1 week ago

*

5

★ ★ ★ ★ ★

BARRY

I first started dealing with John Charcol around 9 months before our BTL remortgage actually completed. We had to try two or three different routes to get the mortgage we needed (due to a unique rental situation), so got to build a great relationship with the team, brilliantly led by Charlotte A. Charlotte was a great, prompt communicator, and each time we hit a problem, she always had an alternative avenue for us to go down. Thankfully, this persistence paid off, and we got the remortgage, raising the capital we needed for a renovation project. Thanks to Charlotte for all the support. I am very happy to recommend.less I first started dealing with John Charcol around 9 months before our BTL remortgage actually completed. We had to try two or three different routes to get the mortgage we needed (due to a unique rental situation), so got to build a great relationship with the team, brilliantly led by Charlotte A. Charlotte was a great, …morePosted 2 weeks ago

*

5

★ ★ ★ ★ ★

ANONYMOUS

Great service and advice. Many thanks.Posted 2 weeks ago

*

5

★ ★ ★ ★ ★

ALISON

Very happy with Norbert arranging a bespoke mortgage for me. He kept me informed throughout. Reasonable price for a unique product. Highlyrecommended.

Posted 2 weeks ago

Read More Testimonials AWARD-WINNING MORTGAGE EXPERTS John Charcol have been providing mortgage advice for a long time. We stand at the forefront of the mortgage industry and have won many awards for our hard work and contributions. We set the benchmark forexcellent service.

More About John Charcol -------------------------MORTGAGE RESOURCES

MORTGAGE CALCULATORS Ready to crunch some numbers? Get started with our free and easycalculators.

Try Our Mortgage CalculatorsMORTGAGE GUIDES

We’ve got guides on everything - from remortgaging to tax on rental income. Find the information you need right here. Read Our Mortgage Guides COMPARE MORTGAGE RATES Look at mortgage rates on the market right now with our freecomparison tools.

Search all Mortgage Rates* About Us

* Introducer and Affiliate Schemes* Our Fees

* Careers

* Our Offices

* Regulatory Statement* Our Team

* Client Testimonials * Complaints Procedure* Our Awards

* Cookie and Privacy Statement * Refer, Relax and Share £200* Accessibility

* Appointed Representatives* Sitemap

Sign Up to Our Newsletter* Newsletter

LEGAL

YOUR PROPERTY MAY BE REPOSSESSED IF YOU DO NOT KEEP UP REPAYMENTS ON A MORTGAGE OR ANY DEBT SECURED ON IT. John Charcol is a trading name of John Charcol Limited and its Appointed Representatives. John Charcol Limited is authorised and regulated by the Financial Conduct Authority. The Financial Services Register number is 665649. Registered in England No. 9157892. Registered office address for John Charcol Limited is St. Helen's, 1 Undershaft, London, EC3P 3DQ. The FCA does not regulate some investment mortgage contracts. Calls may be recorded for training andmonitoring.

� 2020 John Charcol

Web design agency - Liquid Light You are currently offline. Some pages or content may fail to load. This site uses cookies. By continuing to browse and use the site you are agreeing to our use of cookies.To find out more please see ourprivacy statement .

Details

1